3 US Value Stocks With Low P E And Strong Margins

MGIC Investment Corporation MTG | 0.00 |

Rising US bond yields have just taken the heat out of richly priced growth stocks like SpaceX, after its market value dropped by about $400b on a 16.4% share price fall, and that shock is rippling across global markets. When expensive growth names get squeezed, attention often shifts to companies with lower P/E and P/B ratios, steadier balance sheets, and less volatile trading. This article looks at how that shift connects to a Value Stocks screener and examines 3 stocks exposed to the same macro forces as SpaceX that some investors may regard as worth a closer look.

Vipshop Holdings (VIPS)

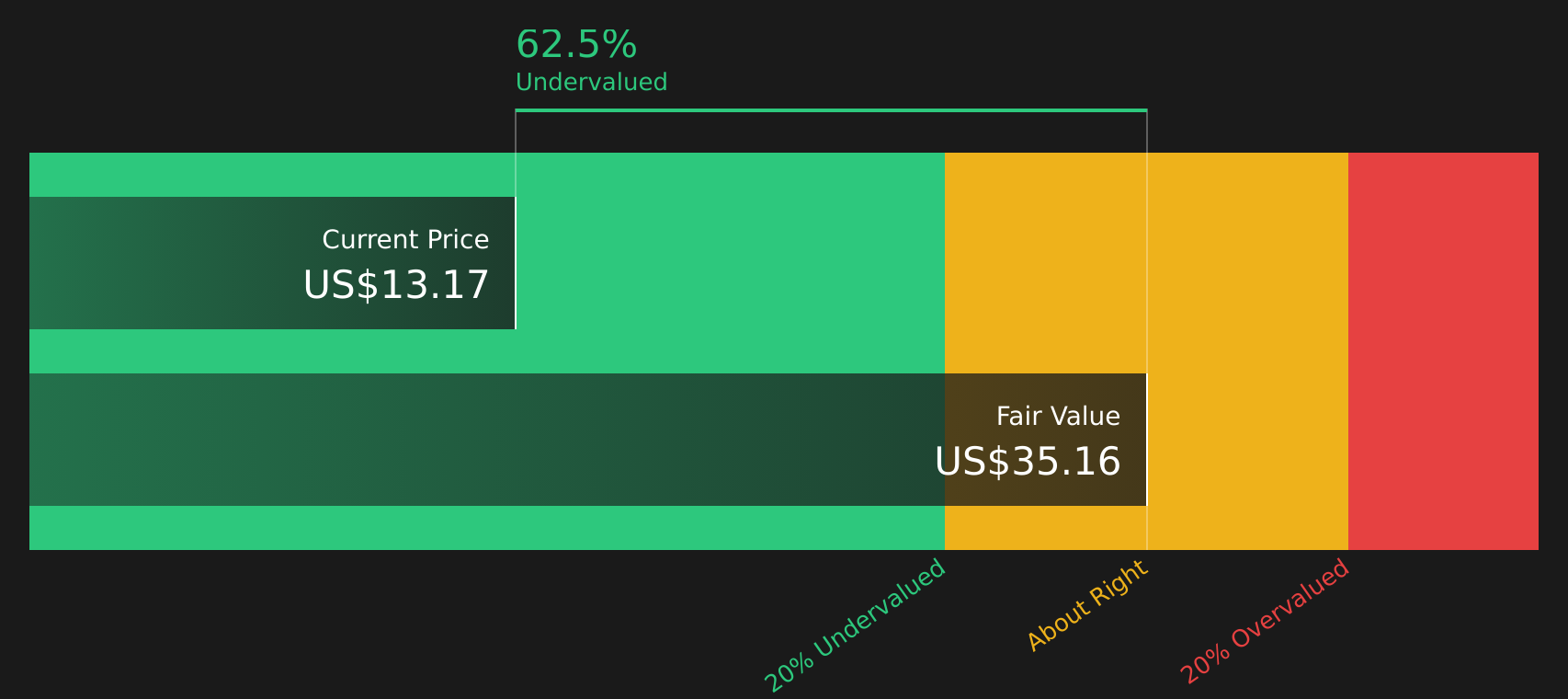

Overview: Vipshop Holdings runs discount focused online platforms and outlet malls in China, offering branded apparel, beauty, and lifestyle products through its vip.com and vipshop.com sites as well as physical stores. It combines merchandising, warehousing, and technology services to sell authenticated brands at value prices to Chinese consumers.

Operations: Vipshop generates all of its CN¥106.2b in revenue in the People's Republic of China.

Market Cap: US$6.4b

Vipshop Holdings draws interest because it couples a low P/E, solid cash generation, and a share price that sits well below some fair value estimates with an apparel focused model that still has customer growth, margin, and competition risks. Earnings have grown 7.5% per year over 5 years. Recent guidance points to flat or slightly weaker near term revenue, which keeps expectations in check even as UBS highlights earnings quality, outlet expansion, and buybacks as supports for the story. With higher US yields pressuring expensive growth stocks such as SpaceX, some investors may see Vipshop as a way to stay in consumer exposure while shifting toward value and cash flow discipline.

Vipshop’s low P/E and cash generation story looks incomplete without a closer read of how earnings quality, buybacks, and outlet expansion fit together, and how the 4 key rewards and 1 important major warning sign could shift the risk balance investors are assuming

Essent Group (ESNT)

Overview: Essent Group is a US focused mortgage insurer and reinsurer that helps lenders and borrowers manage credit risk on residential home loans, alongside a growing business in title insurance, settlement services, and related credit risk management solutions.

Operations: Essent Group generates about US$1.28b in revenue, with roughly US$1.05b from Mortgage Insurance excluding reinsurance, US$102m from Reinsurance, and US$124m from Corporate & Other, almost entirely in the United States.

Market Cap: US$5.4b

Essent Group stands out in a market that has recently punished richly priced growth stocks like SpaceX, because it combines a low P/E and a roughly 60% discount to one fair value estimate with high net margins around 53.6% and a growing dividend that currently yields about 2.46%. Analysts expect modest revenue growth but slightly declining earnings ahead. The company relies on higher risk external borrowing and has seen recent insider selling, so this is not a simple “cheap and safe” story. Add in active buybacks, disciplined underwriting, and sensitivity to interest rates and housing affordability, and Essent Group becomes a value stock that may reward closer inspection rather than a quick judgment.

Essent Group’s rich margins and dividend are only half the story. The real question is whether the valuation discount still matches its risk profile, which the 2 key rewards and 2 important warning signs (1 is major!) quietly puts to the test.

MGIC Investment (MTG)

Overview: MGIC Investment provides private mortgage insurance and related credit risk solutions that help lenders protect against losses when homebuyers default on their loans, covering unpaid principal, delinquent interest, and foreclosure related costs across the US and certain territories.

Operations: MGIC Investment generates about US$1.2b in revenue from Mortgage Insurance.

Market Cap: US$5.5b

MGIC Investment is attracting attention because it combines low P/E and P/B ratios with a core business tied directly to US housing demand, at a time when investors are rethinking rich valuations in high growth stocks after the SpaceX sell off and rising bond yields. Earnings and revenue are expected to edge lower and the business relies entirely on external borrowing. However, net margins are close to 60%, capital returns are meaningful through buybacks and dividends, and the stock trades well below some fair value estimates. For investors who think the market is overreacting to near term housing and credit worries, MGIC’s mix of profitability, conservative risk management, and heavy capital return may be more interesting than recent share price weakness suggests.

MGIC’s low P/E and P/B, high margins, and capital returns story appears to be priced for caution rather than confidence, so the real question is what the 2 key rewards and 1 important major warning sign is hinting at

The three value stocks in this article are just a starting point, with the full Value Stocks screener surfacing 46 more companies that share similar valuation traits and potentially compelling narratives. Identify and analyze stocks that fit your preferred mix of low P/E and P/B ratios, balance sheet strength, dividend potential, and lower volatility so you can focus on the highest conviction ideas using the filters and narrative tools inside Simply Wall St.

Take Control of Your Investment Journey

If Essent Group or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Value Stocks

Fresh opportunities can move from quiet accumulation to breakout momentum fast. Once the crowd catches on, ideal entry points can get crowded or start dropping, so consider taking a closer look in advance.

- Spot income workhorses with solid cash flows and generous payouts before yields get compressed by demand by scanning the 7 dividend fortresses while they are still under the radar for now.

- Track early leaders in AI infrastructure gaining momentum as data demand remains elevated, and use the curated 49 AI infrastructure stocks to filter the most resilient operators first.

- Target metal producers ahead of potential sentiment shifts with a focused look at the 33 elite gold producer stocks before renewed interest in hard assets changes their relative value profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.