3 Value Stocks For Steady Cash Flow And Dividends

Dollar General Corporation DG | 0.00 |

With the Federal Reserve keeping rates on hold but signaling a tougher line on inflation, markets have been reminded that easy money is no longer a given. Bond yields moved higher, stock prices reacted sharply, and investors are again paying close attention to cash flow, balance sheet strength, and reliable income. This article focuses on value stocks that may appeal to investors who prefer companies with defensive traits when policy uncertainty rises. Below, you will find 3 stocks from our Value Stocks screener that appear directly exposed to the latest Fed news and its potential ripple effects on markets.

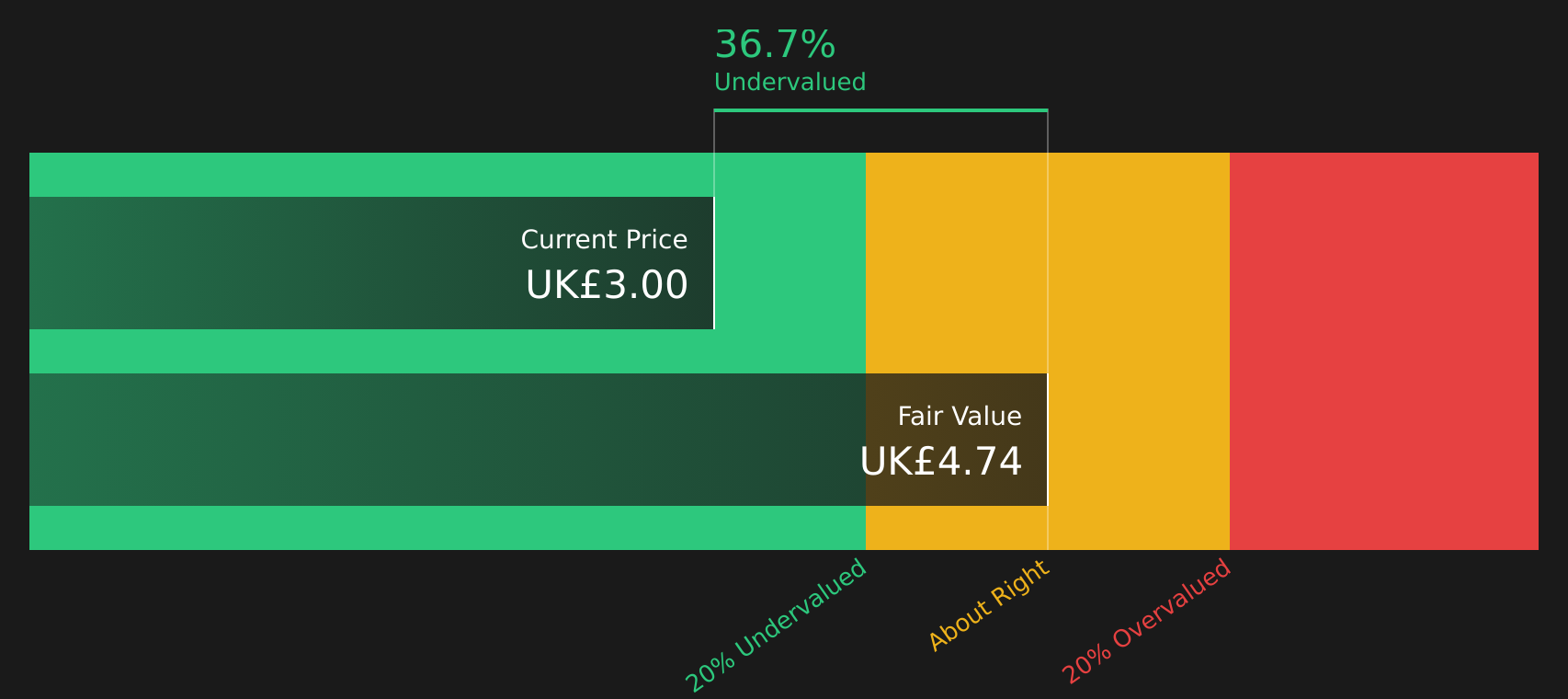

J Sainsbury (LSE:SBRY)

Overview: J Sainsbury is a UK based retailer that runs supermarkets, convenience stores and online channels selling food, general merchandise, clothing and fuel, alongside a smaller banking and insurance operation under brands such as Sainsbury’s, Argos, Habitat, Tu, Nectar and Sainsbury’s Bank.

Operations: J Sainsbury generates virtually all of its £33.6b revenue from Retail activities, with £33.6b from Retail and £96m from Financial Services, all in the United Kingdom.

Market Cap: £6.7b

J Sainsbury offers a defensive profile that some investors may consider when central banks turn more hawkish, with a UK focused grocery business that sells everyday essentials and produces large, relatively stable cash flows. The company is trading below some estimates of fair value and has a dividend yield of 4.54%. However, those payouts are not fully covered by free cash flow and margins remain thin at a 1.2% net profit margin. Management is targeting £1b of cost savings by 2027 and is backing that plan with a £300m buyback. Investors still face clear risks from competition, funding that relies entirely on external borrowing and pressure on general merchandise.

J Sainsbury’s everyday cash flows, 4.54% dividend yield and cost saving targets could be masking a more complex trade off between resilience and risk, so it may be worth reviewing the 3 key rewards and 1 important warning sign

Dollar General (DG)

Overview: Dollar General is a large U.S. discount retailer that focuses on low priced everyday essentials, from groceries and household items to basic apparel and seasonal goods, serving mainly small towns and lower income communities that prioritise value and convenience.

Operations: Dollar General generates about US$43.1b in revenue from its Retail Store Operations segment.

Market Cap: US$24.0b

Dollar General stands out in a hawkish Fed backdrop because a higher rate setting and stretched household budgets often push more shoppers toward discount chains that offer value and proximity. The company’s 3.6% net margin, recent earnings growth of 35.6% and a 2.08% dividend yield sit alongside efforts to lift profitability through private label expansion, store remodels and better control of shrink and freight costs. At the same time, heavy use of external borrowing, wage and freight pressures, and intense competition from Walmart and other discounters mean execution on margins and pricing remains critical. For investors who want to see how that balance of resilience and risk stacks up, the recent earnings beats, guidance tweaks and analyst debate make Dollar General a key stock to watch in the value segment.

Dollar General’s combination of earnings growth, margin pressure and Fed sensitive customers may be telling a more complex story than the headline numbers suggest, so review the analysis report for Dollar General to see what the market could be missing.

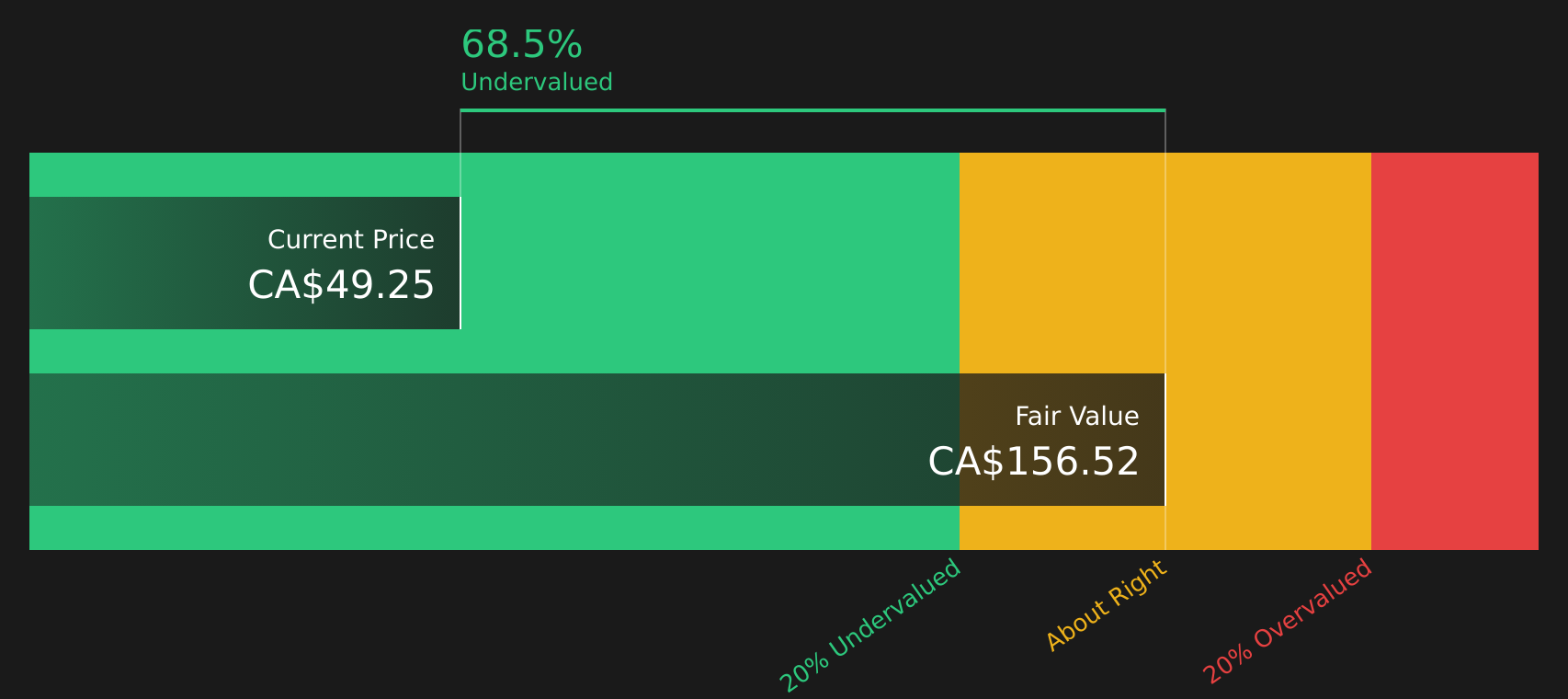

North West (TSX:NWC)

Overview: North West (TSX:NWC) runs grocery, discount and convenience stores, fuel outlets and related services focused on remote and underserved communities in northern Canada, rural Alaska, the South Pacific and the Caribbean. It provides essential food, general merchandise, pharmacy and financial services where competition is limited and demand is driven by everyday needs.

Operations: North West generates CA$1.5b of revenue in Canada and CA$1.1b from international markets.

Market Cap: CA$2.3b

North West provides exposure to the Fed’s more hawkish stance through a retailer built on essential spending in remote regions. This type of spending tends to support steadier cash flow when rates rise and debt feels heavier for consumers. The stock screens as very cheap against an internal cash flow estimate and trades on a P/E below both peers and the wider industry, even though earnings are still positive, margins sit at 5.4% and dividends yield about 3.34%. At the same time, funding relies entirely on external borrowing and longer term earnings trends have been soft, so the key question is whether recent refinancing, cost programs and resilient international same store sales are enough to justify that discount.

North West’s essential spending, 5.4% margins and 3.34% dividend yield could be masking a much bigger gap between perception and reality, so it may be worth reading the 3 key rewards and 1 important major warning sign

The three value stocks in this article are just a starting point, with the full Value Stocks (Defensive, High Cash Flow Companies) screener uncovering 12 more companies that pair defensive cash flows with income and balance sheet strength, and each with its own investment narrative worth a closer look. Use Simply Wall St to identify and analyze the specific catalysts, dividend profiles and risk factors that matter most to you so you can focus on the highest conviction opportunities in this value and defense corner of the market.

Take Control of Your Investment Journey

If J Sainsbury or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Beyond These Value Picks?

Fresh opportunities can move from quiet to breakout quickly, and late entries often get caught chasing momentum instead of value. Scan under the radar ideas now and get in early.

- Spot resilient companies that may hold up when conditions get tougher by scanning the 5 resilient stocks with low risk scores curated for calmer portfolios.

- Capitalize on steady income themes by reviewing the 5 dividend fortresses aimed at stocks where yields and balance sheets work together.

- Track where real profitability meets AI momentum by using the 63 profitable AI stocks that aren't just burning cash so you focus on businesses backed by cash flows, not just hype.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.