A Closer Look At AeroVironment (AVAV) Valuation After Sharp Share Price Momentum

AeroVironment, Inc. AVAV | 0.00 |

Why AeroVironment is on investors’ radar

AeroVironment (AVAV) shares have moved sharply over the past month, with the stock returning about 61%, putting fresh attention on how its current valuation lines up with recent financial results.

At a share price of $378.57, AeroVironment’s recent 30 day share price return of 61.33% and 1 year total shareholder return of 128.90% point to strong momentum building around the stock, in addition to a 360.60% total shareholder return over three years.

If AeroVironment’s move has you looking beyond a single defense name, this could be a good moment to scan other aerospace and defense stocks that are catching market attention.

With AeroVironment now trading at $378.57 and sitting only about 3% below the average analyst price target, the key question is whether recent gains leave limited upside, or if the market is still catching up to its future growth potential.

Most Popular Narrative: 6.3% Undervalued

Against the last close of $378.57, the most followed narrative points to a fair value of about $404, using a 7.6% discount rate.

The company's strategic focus on developing modular, interoperable, and software-defined platforms, including the newly launched AV Halo open software ecosystem, directly aligns with the accelerating adoption of AI-powered autonomy and network-centric warfare. This positioning may enable future premium pricing, increased service revenues, and gross margin expansion as these high-value platforms are deployed at scale. Successful integration of the BlueHalo acquisition materially expands AeroVironment's addressable markets, diversifies its competitive portfolio, and enables operational leverage as the company increases manufacturing capacity, which may support bottom-line EBITDA and net margin improvement as production volumes ramp.

Curious how projected revenue, margin expansion, and a future earnings multiple all fit together at this price? The core assumptions are bolder than you might think.

Result: Fair Value of $404.00 (UNDERVALUED)

However, keep in mind that heavy reliance on U.S. defense contracts and margin pressure linked to the BlueHalo acquisition could challenge the upbeat narrative around AVAV.

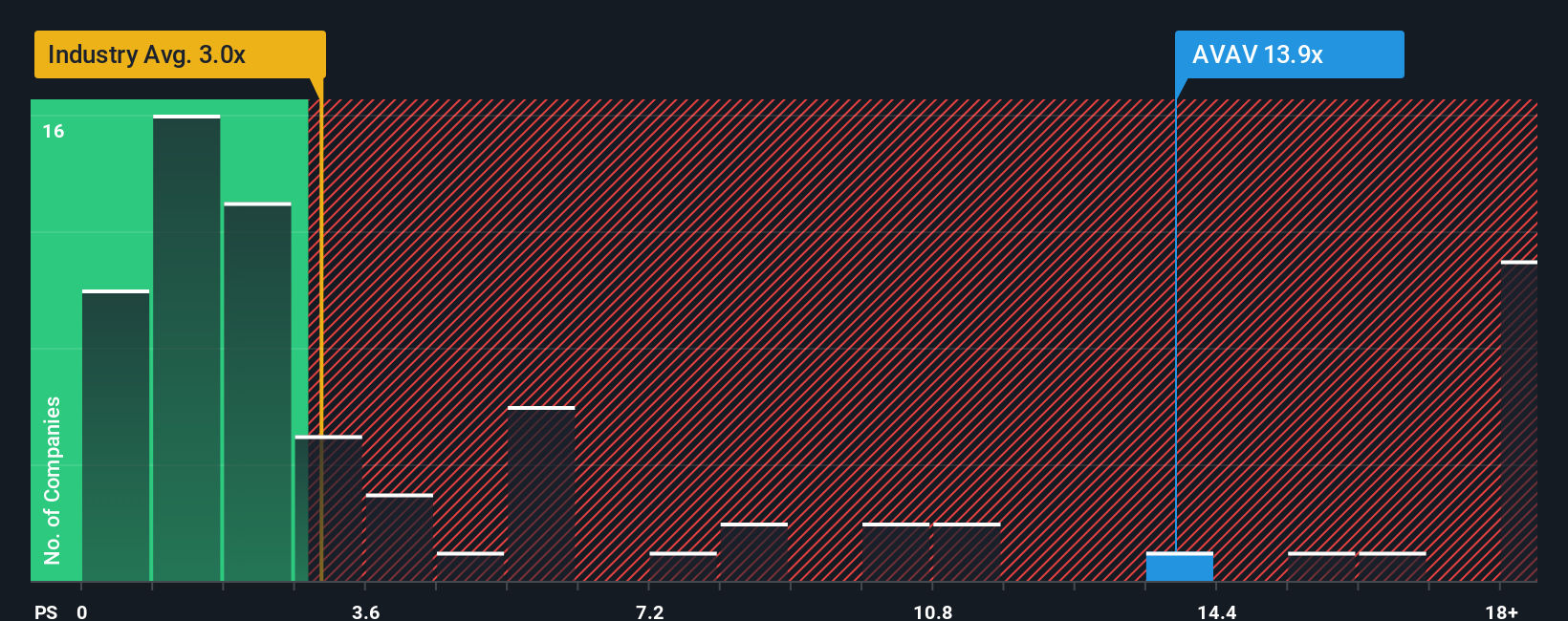

Another View: Rich Sales Multiple Raises Questions

That 6.3% undervaluation narrative sits alongside a very different signal from the P/S ratio. At 13.9x sales, AeroVironment trades at a much richer level than both the US Aerospace & Defense average of 3.8x and peers at 12.7x, while the fair ratio is 4x.

If the market eventually leans closer to that fair ratio, today’s price could leave little room for disappointment. The question for you is whether future growth and margins justify staying this far above where sales multiples for the sector, peers, and the fair ratio currently sit.

Build Your Own AeroVironment Narrative

If you see the numbers differently, or simply prefer to test your own assumptions against the data, you can build a tailored thesis in minutes: Do it your way.

A great starting point for your AeroVironment research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If AeroVironment has caught your eye, do not stop here. Some of the most interesting opportunities often sit just outside your current watchlist.

- Spot underpriced potential early and scan these 874 undervalued stocks based on cash flows that may trade below what their cash flows suggest.

- Ride powerful tech themes by checking out these 24 AI penny stocks positioned around artificial intelligence growth.

- Target dependable income streams and review these 12 dividend stocks with yields > 3% that focus on yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.