A Closer Look at Camtek (NasdaqGM:CAMT) Valuation After Completion of $425 Million Convertible Bond Offering

Camtek Ltd CAMT | 157.73 | -0.61% |

Camtek (NasdaqGM:CAMT) just wrapped up a $425 million zero-coupon convertible bond offering, following last week’s initial announcement of the deal. For investors, this is not just another fundraising event; it signals a major shift in how Camtek is choosing to finance future growth, boost its balance sheet, and potentially increase flexibility for new projects or acquisitions in the future. The convertible nature of the notes means current and prospective shareholders will want to pay close attention, as these securities can eventually be swapped for stock, impacting ownership and future returns.

The completion of this convertible offering comes after a year in which Camtek’s stock has steadily gained, up roughly 7% over the past year, and climbing nearly 24% in the past 3 months. Momentum appears to be building, especially when considering the company’s solid multi-year performance and recurring double-digit growth in both revenue and net income. Past moves such as acquisitions have already shaped Camtek’s trajectory, and this bond issue represents one of the most substantial capital moves in its recent history.

With shares continuing to climb and fresh capital available, the real question is whether Camtek’s current market price still represents a bargain, or if investors are already factoring in high growth expectations.

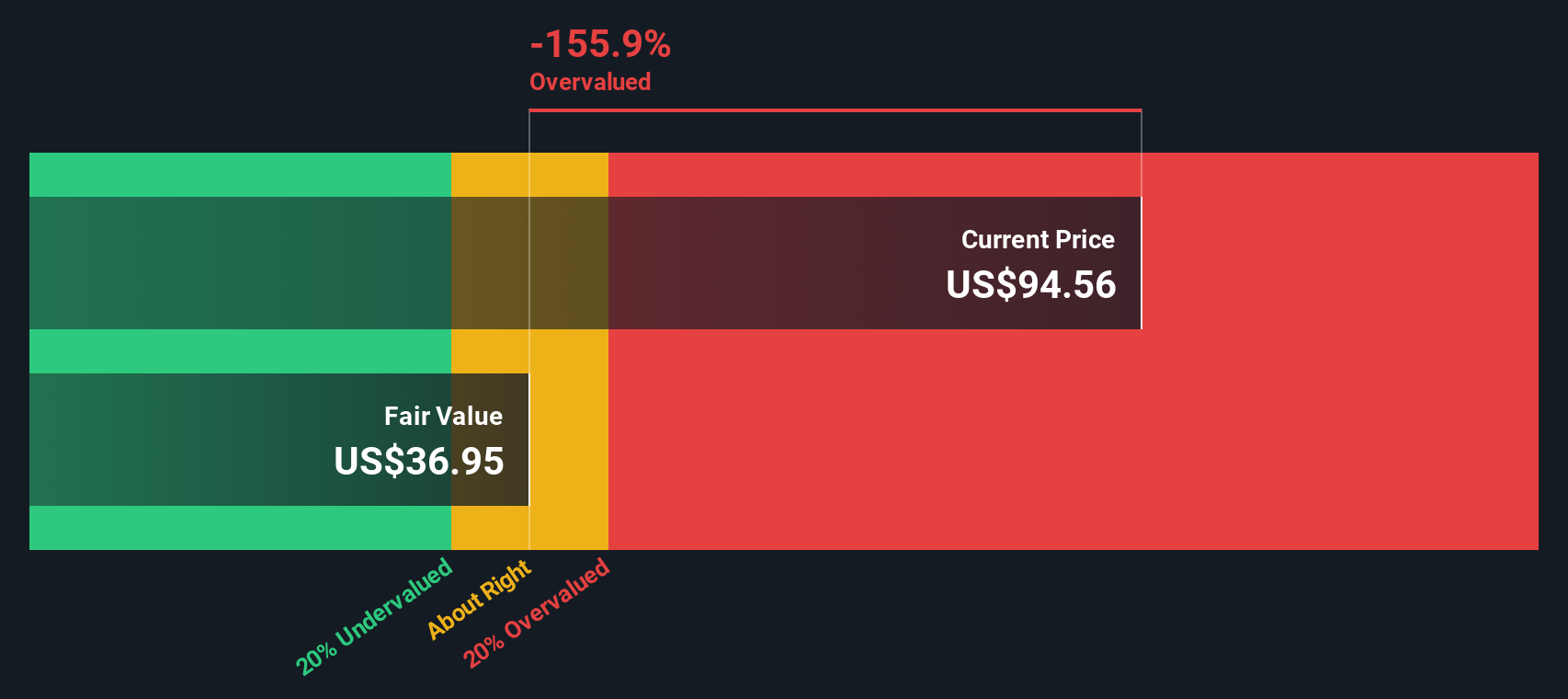

Most Popular Narrative: 12.2% Undervalued

The leading valuation narrative considers Camtek shares to be undervalued, based on robust growth expectations and industry catalysts that could lift the company's fair value above current market levels.

Accelerating demand for high-performance computing (HPC) and AI-driven applications is expanding the need for advanced packaging, micro-bump, and hybrid bonding inspection. This directly grows Camtek's total addressable market and supports multi-year revenue growth. Rapid customer adoption of newly launched Hawk and Eagle G5 platforms, which address evolving requirements such as smaller defect detection and higher throughput, is expected to drive both incremental revenue and gross margin expansion as customers prioritize advanced features and process future-proofing.

Curious how this narrative justifies Camtek’s price target? The full story uncovers a web of growth projections, technology bets, industry shifts, and bold assumptions about market leadership. The critical quantitative details behind the “undervalued” label might surprise you. Want to dig into the exact drivers analysts see fueling Camtek’s future worth? The deeper you look, the more interesting the forecast becomes.

Result: Fair Value of $99.10 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, Camtek’s deep reliance on Asian markets and intensifying competition from larger rivals could quickly challenge these optimistic forecasts if industry dynamics shift.

Find out about the key risks to this Camtek narrative.Another View: Discounted Cash Flow Model

Our SWS DCF model paints a different picture. This approach, which forecasts future cash flows and discounts them to the present, suggests the shares might not be as attractively priced as the first method claims. Which should investors trust?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Camtek Narrative

Of course, if you have a different take or want to dive into the numbers yourself, you can craft your own perspective in just a few minutes. Do it your way.

A great starting point for your Camtek research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Take charge of your portfolio’s potential. Don’t let tomorrow’s best opportunities pass you by. Experience game-changing stocks and new market trends with these handpicked ideas:

- Unlock the upside of underappreciated companies poised for strong future cash flows by searching for undervalued stocks based on cash flows.

- Maximize your income with shares that offer consistent payouts over 3% by checking out dividend stocks with yields > 3%.

- Stay ahead of the curve in healthcare innovation. See which groundbreaking companies are leading the AI-powered transformation within healthcare AI stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.