A Fresh Look at Medical Properties Trust (MPW) Valuation Following Share Repurchase Announcement

Medical Properties Trust, Inc. MPW | 5.02 | 0.00% |

Medical Properties Trust (MPW) just revealed a new share repurchase program, planning to buy back up to $150 million of its own stock. This move generally reflects management’s confidence in the company’s outlook and future prospects.

Medical Properties Trust’s latest buyback comes after a notable run in its share price, which has surged more than 24% over the past 90 days. This has helped boost its year-to-date share price return to 26%. While long-term total shareholder returns are still deep in negative territory, short-term momentum has clearly picked up, signaling a potential shift in sentiment as management renews its focus on shareholder value.

If this kind of turnaround interests you, now’s a great time to broaden your horizons and discover fast growing stocks with high insider ownership

With shares up sharply and management signaling optimism through buybacks, investors now face a key question: is Medical Properties Trust still undervalued, or has the recent rally fully reflected its future growth prospects?

Most Popular Narrative: Fairly Valued

Medical Properties Trust closed at $5.07, just above the most widely tracked narrative fair value of $5.00 per share. The latest analysis points to a balanced view, but the projection is anchored by a few standout assumptions.

Accelerated ramp-up of rental payments from newly installed operators on previously distressed hospital assets, demonstrated by a jump from $3.4 million to $11 million in cash rental income quarter over quarter and an expected annualized cash rent exceeding $1 billion by 2026, positions the company for significant near-term revenue and FFO improvement.

What’s fueling that confidence? The narrative is betting on a dramatic shift in operating profits and future margins, all hinging on earnings turning positive and a hefty earnings multiple. Want to know what’s behind those figures and which assumptions have analysts divided? The full breakdown reveals the high-stakes thinking setting this fair value.

Result: Fair Value of $5.00 (ABOUT RIGHT)

However, ongoing tenant concentration risk and higher refinancing costs could quickly turn optimism into fresh concerns if these headwinds intensify.

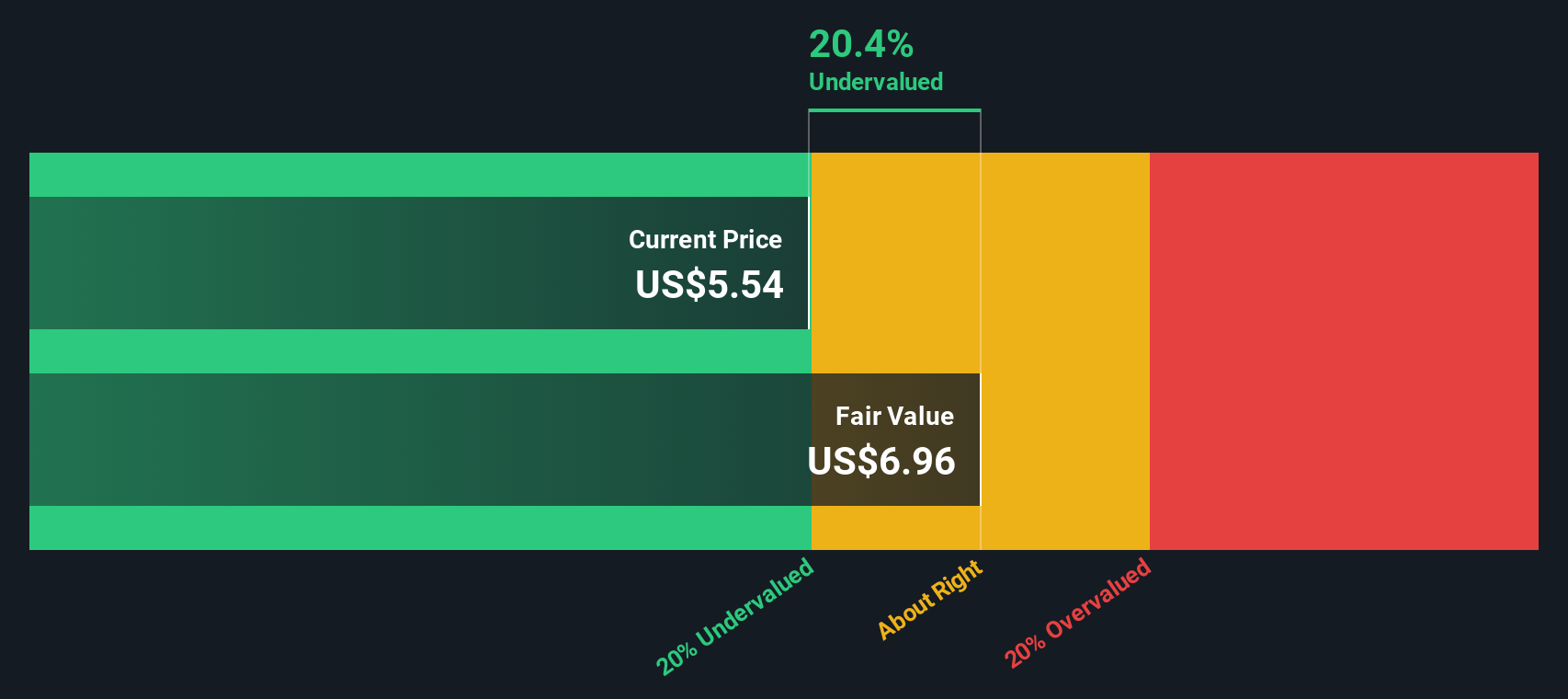

Another View: Discounted Cash Flow Suggests Undervaluation

While the fair value assessment points to Medical Properties Trust being about fairly priced, our SWS DCF model offers a different perspective. Based on projected future cash flows, the DCF model finds the shares are trading at a substantial 25.6% discount to intrinsic value. Could this deep discount be a real opportunity, or is the gap a sign that risks remain underappreciated?

Build Your Own Medical Properties Trust Narrative

If you see things differently or like to back your own analysis, you can build your own narrative in just a few minutes: Do it your way

A great starting point for your Medical Properties Trust research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Expand your horizons and increase your chances of spotting tomorrow’s winners by checking out these hand-picked opportunities available right now on Simply Wall Street:

- Tap into stocks with stable cash flows and long-term upside by starting your search with these 870 undervalued stocks based on cash flows.

- Seize the high-yield advantage by jumping straight to these 16 dividend stocks with yields > 3% and uncovering companies offering attractive payouts above 3%.

- Ride the wave of AI innovation and uncover hidden gems among these 24 AI penny stocks powering the next generation of intelligent solutions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.