A Fresh Look at MongoDB (MDB) Valuation as Earnings Anticipation and Analyst Optimism Build

MongoDB, Inc. Class A MDB | 253.12 | +1.51% |

MongoDB (MDB) is drawing attention as investors look ahead to its upcoming earnings report on December 1. The company’s performance and sustained analyst optimism are both fueling curiosity about its next move.

MongoDB’s share price has surged over 35% year-to-date, reflecting growing investor confidence as the company’s Atlas cloud platform and enterprise adoption trends gain traction. Despite a modest total shareholder return of just over 3% for the past year, momentum appears to be building with several well-received quarters and a consistently positive outlook from industry watchers.

If you want to see what other high-potential tech names are getting investor attention right now, your next move should be to check out See the full list for free.

With so much optimism and strong analyst backing ahead of earnings, investors now face the key question: Is MongoDB undervalued at current levels? Alternatively, has the market already priced in the anticipated growth, leaving limited room for upside?

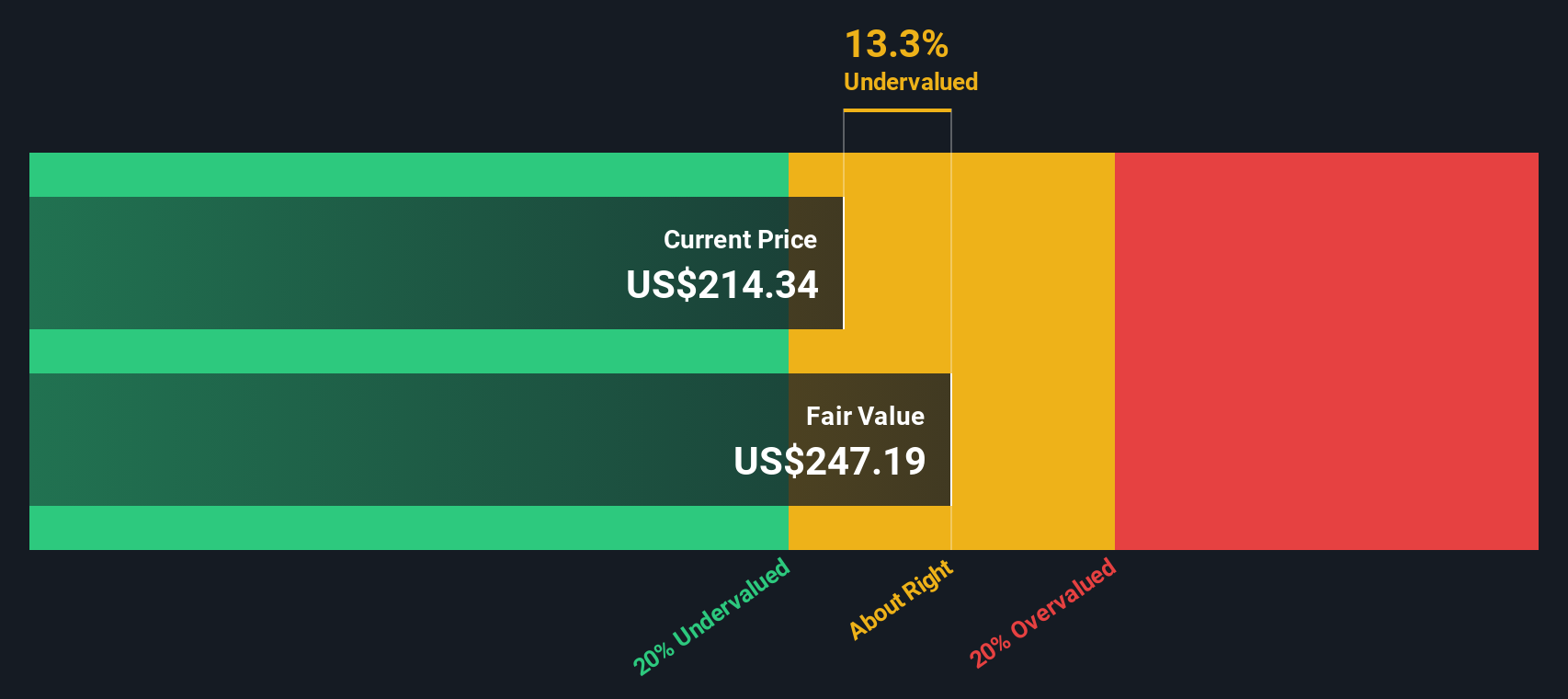

Most Popular Narrative: 10% Undervalued

MongDB’s current price sits below the most widely followed narrative's fair value estimate, suggesting a potential gap between market expectations and analyst projections. The discount rate applied by the narrative is 8.85%.

Ongoing product innovation, including integrated capabilities like search, vector search, and embeddings, increases platform stickiness and wallet share. This enables deeper penetration of current accounts and higher net revenue retention, which can drive both top-line and operating margin improvement over time.

Curious which numbers underpin this bullish stance? The narrative banks on a turbocharged rise in earnings and stronger profitability, all factored into a daunting future profit multiple. Discover the full forecast behind this seemingly aggressive valuation.

Result: Fair Value of $369.91 (UNDERVALUED)

However, some caution is warranted as competition from open-source rivals and reliance on large enterprise accounts could slow MongoDB’s longer term revenue momentum.

Another View: Discounted Cash Flow Signals Caution

While some argue MongoDB is undervalued compared to analyst price targets, our DCF model presents a different perspective. According to the SWS DCF model, MongoDB's current price of $332.37 is significantly higher than our estimated fair value of $216.91. This suggests the shares may be overvalued from a cash flow perspective. This raises the question of whether growth expectations might be too optimistic, or if the market is factoring in considerations that our model has not captured.

Build Your Own MongoDB Narrative

If the existing narratives aren’t your style or you’d rather dig through the facts yourself, you can quickly craft your own view in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding MongoDB.

Looking for more investment ideas?

Maximize your portfolio’s potential by tapping into curated stock ideas you might otherwise overlook. Staying ahead of the curve is easier with these powerful tools from Simply Wall Street.

- Uncover income opportunities when you scan for proven yields through these 15 dividend stocks with yields > 3% that consistently deliver solid payouts above 3%.

- Get ahead of tomorrow’s innovation by targeting these 28 quantum computing stocks, which is driving breakthroughs in computing and powering the next tech revolution.

- Leap into the future of healthcare by checking out these 30 healthcare AI stocks, where medical discovery meets artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.