A Fresh Look at Tyler Technologies’s Valuation Following Raised 2025 Outlook and Q3 Growth

Tyler Technologies, Inc. TYL | 342.38 | +0.36% |

Tyler Technologies (TYL) just released its third-quarter results, showing growth in both revenue and net income compared to last year. The company also raised its 2025 guidance and is forecasting around 10% higher revenue.

Despite upbeat quarterly results and raised full-year guidance, Tyler Technologies’ share price return has struggled lately, slipping 8% over the past month and down 19% year-to-date. However, looking further back, the stock’s three-year total shareholder return remains a robust 43%. This shows longer-term investors have still been rewarded even as near-term momentum fades.

If you’re weighing long-term resilience or searching for what else the market’s offering right now, expand your view with fast growing stocks with high insider ownership

Given the recent pullback in share price despite strong financial results, the key question now becomes whether Tyler Technologies is trading at an attractive value or if the market has already factored in its growth outlook. Could this be a buying opportunity, or is everything priced in?

Most Popular Narrative: 30% Undervalued

Compared to its latest closing price of $463.43, the narrative fair value for Tyler Technologies comes in much higher. This highlights a strong upside based on forward-looking fundamentals. The stage is set for a debate on whether robust cloud growth and premium pricing power justify this more optimistic valuation.

Ongoing investment in AI-powered tools and automation, as seen in product launches like the AI-driven Resident Assistant and enhanced budgeting solutions, addresses public sector labor challenges and the need for data-driven decision-making. This enables premium pricing, reduces customer churn, and provides opportunities for scalable margin improvements over time.

Want to know which financial levers are fueling this huge upside? The narrative is built on a handful of bullish assumptions that could surprise you. Curious about the underestimated factors driving the fair value sky-high? See what powers the boldest forecast in the sector.

Result: Fair Value of $664.06 (UNDERVALUED)

However, Tyler Technologies still faces potential pressure from its reliance on government budgets and ongoing unpredictability in large deal bookings. These factors could affect future performance.

Another View: Multiples Tell a Different Story

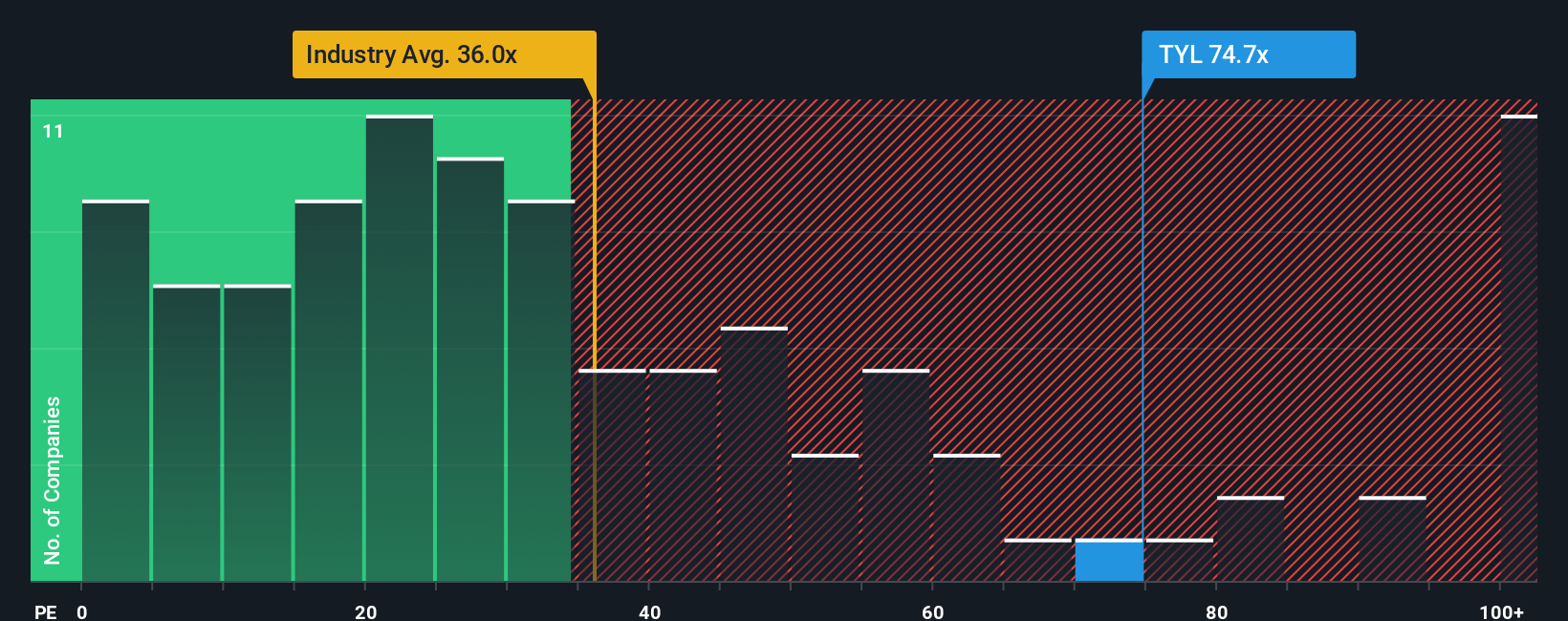

Looking at Tyler Technologies through the lens of earnings multiples offers a contrasting take. The company currently trades at 63.2 times earnings, which is not only far above the US Software industry average of 34.3 but also exceeds its peers’ average of 58.2 and its own fair ratio of 34.3. This wide gap suggests the market has priced in a premium, creating a valuation risk if expectations are not met. Does this hefty multiple signal lasting confidence, or leave room for a pullback?

Build Your Own Tyler Technologies Narrative

If you see things differently or want to dive deeper into the numbers, you can put together your own narrative in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Tyler Technologies.

Looking for More Investment Ideas?

Don't let market momentum pass you by. Expand your strategies and uncover stocks with unique growth angles using these targeted picks from Simply Wall Street's screener:

- Scan the market for deeply undervalued opportunities by starting with these 875 undervalued stocks based on cash flows to uncover companies trading well below their fair value.

- Tap into the power of artificial intelligence by seeking out innovation leaders through these 24 AI penny stocks and take part in the next wave of digital transformation.

- Strengthen your portfolio with steady income by checking out these 16 dividend stocks with yields > 3% which features stocks with yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.