A Look At 10x Genomics (TXG) Valuation After A Strong Year Of Share Price Momentum

10x Genomics TXG | 0.00 |

Recent performance snapshot for 10x Genomics

10x Genomics (TXG) has drawn fresh attention after a strong run in the stock, with the share price up 4.5% over the past day and about 32% over the past month.

Over the past 3 months, the stock has gained about 31%, while the year to date return sits near 78%. On a 1 year view, the total return is about 3.1x, while 3 and 5 year total returns remain significantly lower.

The recent 1 day share price return of 4.54% and 7 day share price return of 24.96% at a share price of $29.59 sit alongside a very large 1 year total shareholder return, even though the 3 and 5 year total shareholder returns remain sharply lower. This points to momentum building in the shorter term while the longer term record is still weak.

If you are looking beyond 10x Genomics for other high growth ideas in related areas, this could be a good moment to scan for fast growing healthcare AI opportunities using the 40 healthcare AI stocks

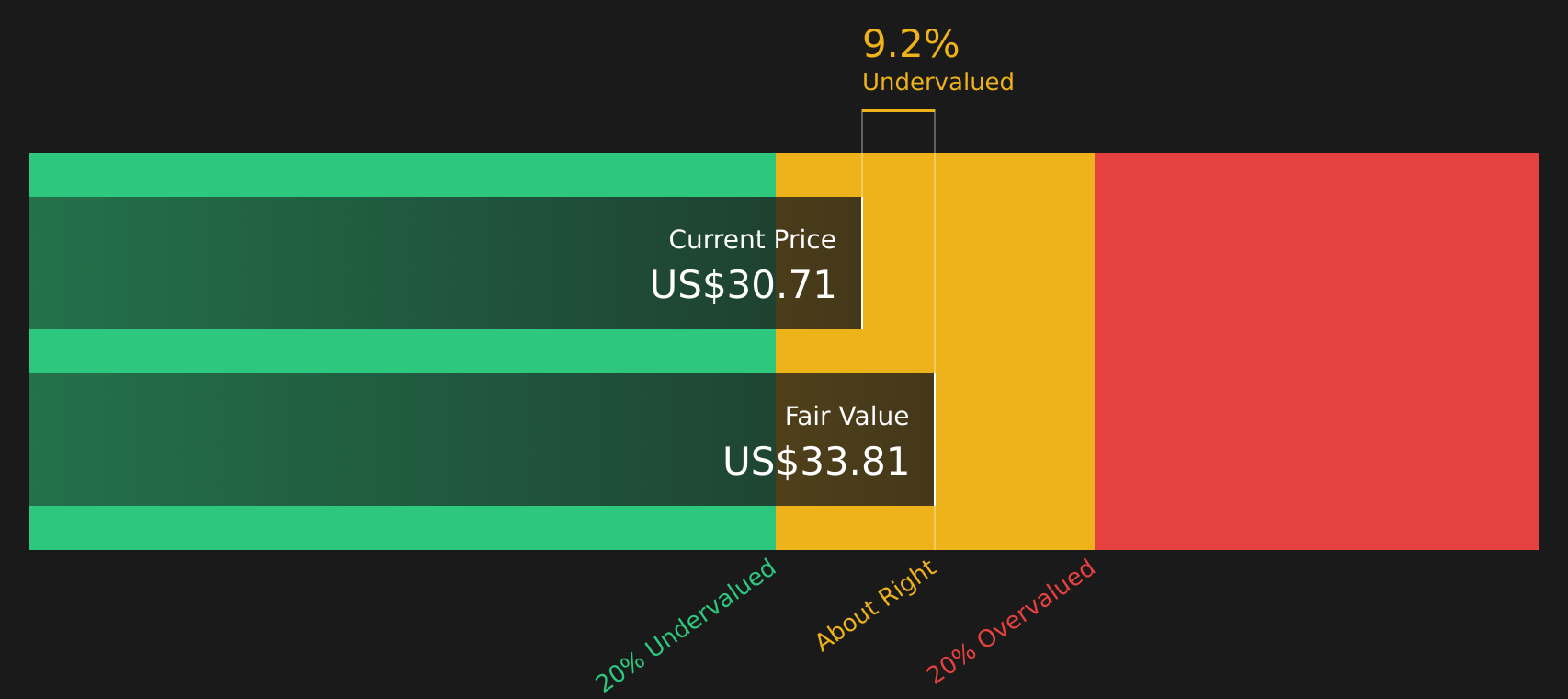

With 10x Genomics trading at $29.59, slightly above an average analyst price target of $25.23 yet showing a modest intrinsic discount, the key question now is whether there is still a buying opportunity or if markets are already pricing in future growth.

Most Popular Narrative: 46.9% Overvalued

The most followed narrative puts 10x Genomics’ fair value at $20.14, well below the recent $29.59 close, so the gap to current pricing is wide.

Recent and upcoming product launches including Flex v2 (targeting higher throughput, lower costs, and AI integration), Visium HD extensions, and Xenium RNA plus protein are expanding the range of applications and reinforcing 10x's leadership in advanced genomics tools, and are expected to drive both top-line growth and sustain premium pricing over time.

Want to see what kind of revenue path, margin lift, and future earnings multiple are built into that fair value gap? The core assumptions might surprise you.

Result: Fair Value of $20.14 (OVERVALUED)

However, shrinking pricing power on key instruments and continued operating losses could still pressure margins and challenge the assumptions behind that 46.9% overvaluation call.

Another View: Cash Flows Tell a Different Story

Analysts using earnings based assumptions see 10x Genomics as 46.9% overvalued at $29.59 versus a $20.14 fair value. Yet our DCF model, which focuses on future cash flows rather than earnings multiples, points to a fair value of $33.80, leaving the stock at roughly a 12.5% discount. Which lens do you trust more when the signals disagree?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out 10x Genomics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

After all this, are you leaning bullish, cautious, or somewhere in between? If this stock is on your radar, now is a good time to weigh the trade off between upside potential and the concerns already flagged and take a closer look at its 2 key rewards and 1 important warning sign

Ready for more investment ideas?

If 10x Genomics has your attention, do not stop here. Broader opportunities across different styles and risk levels could be just as important for your next move.

- Spot potential bargains early and review the screener containing 22 high quality undiscovered gems before others start paying attention.

- Build a sturdier core for your portfolio and scan the solid balance sheet and fundamentals stocks screener (45 results) for companies with stronger financial footing.

- Dial back risk without stepping away from the market completely by checking out the 62 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.