A Look At ADTRAN Holdings (ADTN) Valuation After Improved Q1 Results And Updated Earnings Guidance

ADTRAN Holdings, Inc. ADTN | 0.00 |

ADTRAN Holdings earnings and guidance move into focus

ADTRAN Holdings (ADTN) has come under closer scrutiny after first quarter results showed higher revenue and a smaller net loss, alongside fresh second quarter revenue guidance that framed expectations for the rest of 2026.

Despite the latest quarterly update, the stock’s 1-day share price return of 7.38% and 7-day share price return of 17.75% were weak. However, the 90-day share price return of 47.57% and 1-year total shareholder return of 88.72% still point to strong momentum from a low base.

If ADTRAN’s swings have you thinking about diversification, this could be a good moment to broaden your search with our screener of 40 AI infrastructure stocks

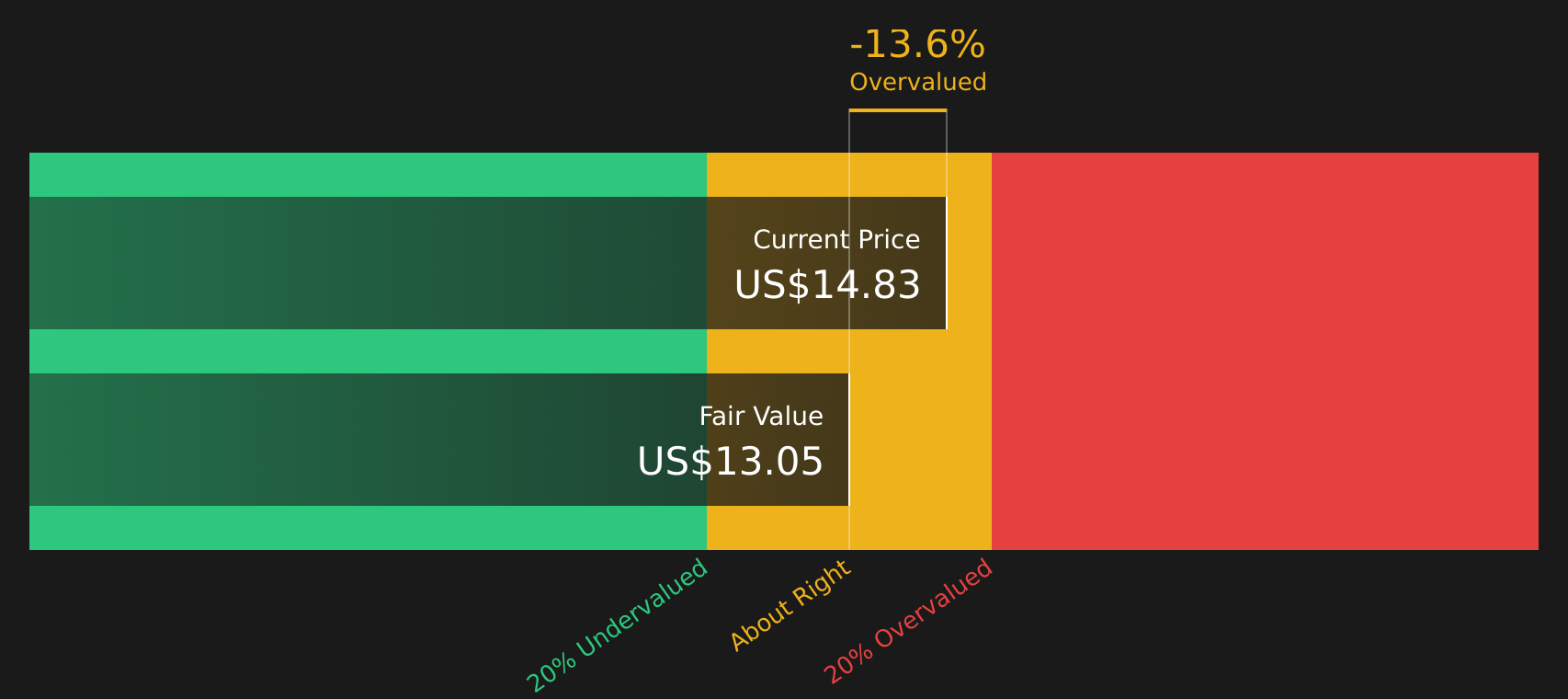

With revenue at US$286.09 million, a net loss trimmed to US$1.32 million, and the stock trading around US$14.55 versus an average analyst target of US$19.50, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 25.4% Undervalued

With ADTRAN Holdings trading at $14.55 against a widely followed fair value narrative of $19.50, the core question is whether earnings and margins can eventually catch up to that gap.

Rising infrastructure investment for AI computing, cloud, and 5G densification is driving higher demand for ADTRAN's optical networking solutions and cross-selling opportunities, which should boost both revenue and market share as these trends intensify.

Read the complete narrative. Read the complete narrative.

Want to see what is actually baked into that higher fair value? The narrative leans on stronger broadband demand, margin repair and a richer earnings multiple. The main point of interest is how those three pieces interact across the next few years.

Result: Fair Value of $19.50 (UNDERVALUED)

However, you also need to weigh FX swings and any slowdown in U.S. or European broadband spending, which could challenge margin repair and the higher future P/E expectations.

Another Angle On Value: Cash Flows Tell A Different Story

The fair value narrative of $19.50 leans on earnings and multiples, but the SWS DCF model points the other way, with an estimated future cash flow value of $12.84. That implies ADTRAN could be trading above its cash flow value. Which signal do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ADTRAN Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Curious whether the optimism in this story really holds up? Take a closer look at the data, compare it with your own expectations, and weigh the 3 key rewards

Looking for more investment ideas?

If ADTRAN has sharpened your interest in new opportunities, do not stop here. Broaden your watchlist now so you are not chasing ideas after they move.

- Spot potential mispricings early by checking companies that look cheap on quality metrics using our 51 high quality undervalued stocks.

- Strengthen your comfort with balance sheet quality by scanning companies highlighted in the solid balance sheet and fundamentals stocks screener (44 results).

- Get ahead of the crowd by tracking lesser-known opportunities surfaced through the screener containing 23 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.