A Look At Akamai Technologies (AKAM) Valuation After Deutsche Telekom Security Partnership Spurs Investor Interest

Akamai Technologies, Inc. AKAM | 118.00 | +1.94% |

Why Akamai’s Deutsche Telekom Security partnership matters for investors

Akamai Technologies (AKAM) is back in focus after highlighting how Deutsche Telekom Security is using its Security Certified Service Provider program to deliver API protection and microsegmentation services for heavily targeted, regulated industries.

Akamai shares have picked up momentum recently, with a 25.61% 90 day share price return and a 10.13% year to date share price return to US$93.72. However, the 1 year total shareholder return of a 1.46% decline and 5 year total shareholder return of a 22.19% decline show a tougher longer term picture as investors reassess growth potential and risk around security driven partnerships like Deutsche Telekom Security and upcoming earnings.

If this security story has your attention, it could be a good moment to see what else is moving among high growth tech and AI stocks that are shaping how digital infrastructure gets defended.

With Akamai trading at US$93.72 against an average analyst price target of about US$101 and an estimated intrinsic value gap of around 26%, you have to ask yourself whether this is a genuine mispricing or if the market is already factoring in the next leg of growth.

Price-to-Earnings of 26.6x: Is it justified?

At a last close of US$93.72, Akamai trades on a P/E of 26.6x, which screens as cheaper than both peers and the broader US IT industry.

The P/E multiple compares the share price with earnings per share, so it gives you a quick sense of how much you are paying for each dollar of profit. For a security and cloud infrastructure business that is earnings positive, this is a common way investors compare it with alternatives in the same space.

On the numbers provided, Akamai is described as trading at good value compared to peers and industry, with its 26.6x P/E sitting below a peer average of 43.9x and below the US IT industry average of 27.4x. It is also below an estimated fair P/E of 32.7x, which indicates the market is pricing the stock at a discount to the level that model implies it could reach if sentiment and expectations aligned with those inputs.

Result: Price-to-Earnings of 26.6x (UNDERVALUED)

However, you also have to weigh risks, such as execution on security partnerships translating into sustained demand, and any slowdown in revenue or net income growth resetting expectations.

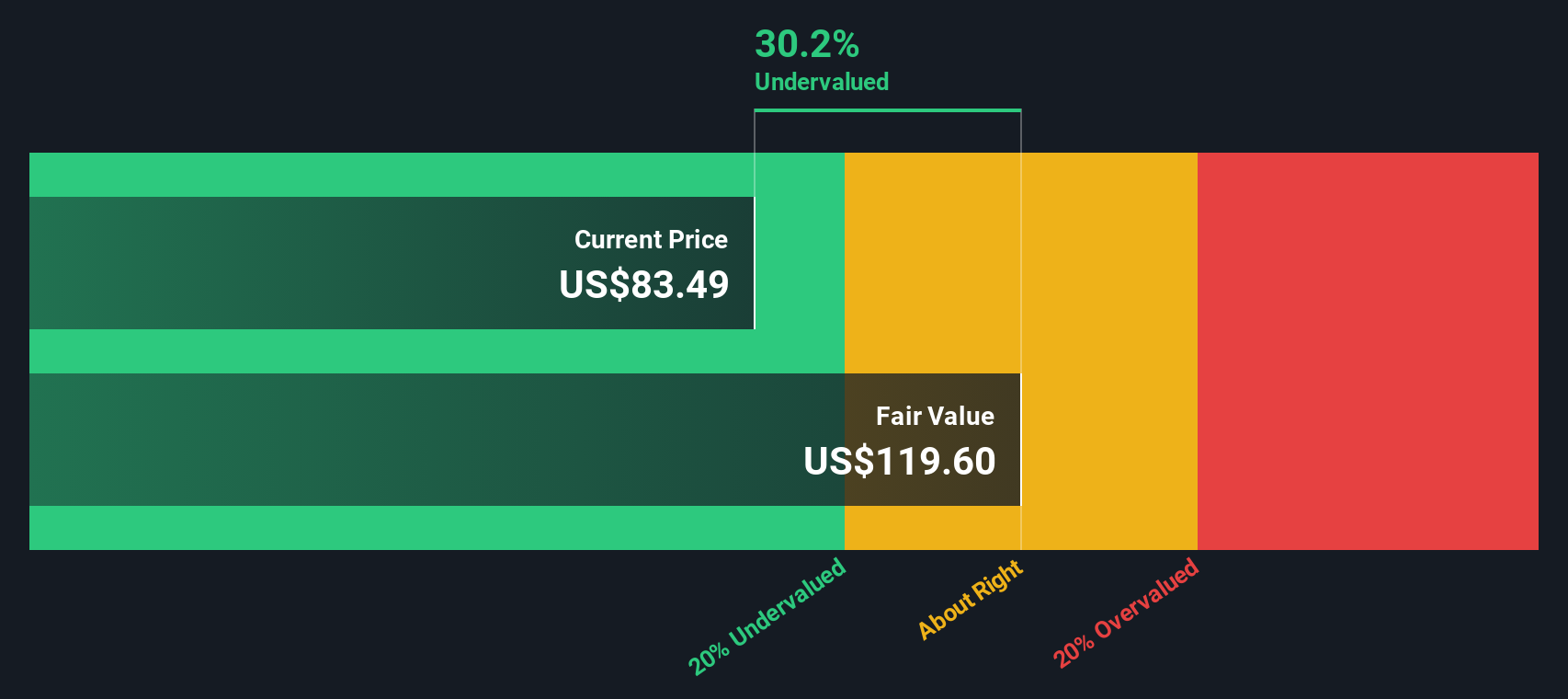

Another take using our DCF model

While the 26.6x P/E suggests Akamai is priced below peers and an estimated fair ratio of 32.7x, our DCF model points to a much larger gap. With the shares at US$93.72 versus a future cash flow value estimate of US$125.90, the model indicates the stock may be undervalued. The real question is which yardstick you place more weight on, given that cash flow, growth forecasts and risk can each point in slightly different directions.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Akamai Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 876 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Akamai Technologies Narrative

If you look at these numbers and reach a different conclusion, or just want to stress test the assumptions yourself, you can create your own view in a few minutes, starting with Do it your way.

A great starting point for your Akamai Technologies research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Akamai has sharpened your focus, do not stop here. Broaden your watchlist with focused stock ideas that match how you like to invest.

- Chase potential income by reviewing these 13 dividend stocks with yields > 3% that might suit a portfolio built around regular cash returns.

- Back future tech trends by checking out these 23 AI penny stocks shaping how artificial intelligence reaches real world applications.

- Hunt for mispriced opportunities by scanning these 876 undervalued stocks based on cash flows where current prices differ from underlying cash flow estimates.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.