A Look At Akamai Technologies (AKAM) Valuation After New AI Security Launches

Akamai Technologies, Inc. AKAM | 118.00 | +1.94% |

Akamai Technologies (AKAM) has rolled out Akamai Brand Guardian, an AI-powered upgrade to its existing brand protection tools. The new solution is aimed at helping enterprises manage large scale impersonation and fraud attempts across their digital presence.

The recent AI-focused launches, including Brand Guardian and new Guardicore Segmentation features, come after a strong run in the shares. Akamai’s 30-day share price return of 17.1% and 1-year total shareholder return of 43.8% suggest that momentum has been building as the market reassesses growth potential and risk profile.

If you are looking beyond Akamai’s AI push, this could be a good moment to scan other names benefiting from similar themes using our screener for 35 AI infrastructure stocks

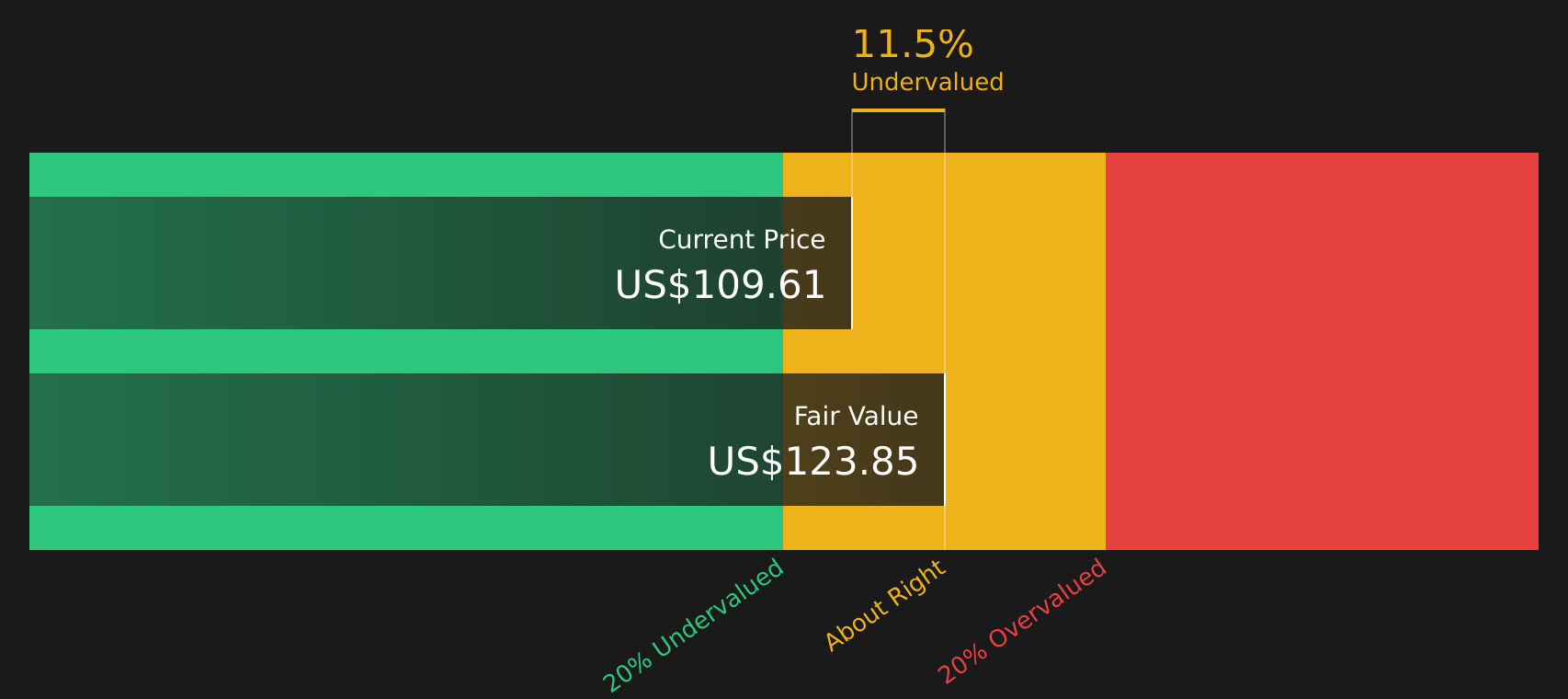

With Akamai shares up 17.1% in 30 days and 43.8% over the past year, yet still showing a small intrinsic discount and trading above the average analyst target, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 14.1% Overvalued

With Akamai shares at $117.25 and the most followed narrative pointing to a fair value of $102.72, the story hinges on how future growth and profitability are expected to develop under that framework.

Akamai's continued investment and go to market transformation in security and compute, including expanded sales capacity and channel partnerships, should enable it to tap further into the expanding addressable market for cloud and edge security, likely contributing to both top line growth and long term earnings leverage as these businesses scale.

Curious what revenue profile, margin path, and future earnings multiple are baked into that fair value line? The narrative leans on specific growth rates, a higher profitability mix and a re rated valuation that all need to work together.

Result: Fair Value of $102.72 (OVERVALUED)

However, this hinges on delivery headwinds easing and large compute contracts ramping as expected; any setback there could quickly challenge the current growth and valuation story.

Another Take: Cash Flows Paint A Different Picture

The fair value from the most followed narrative suggests Akamai is 14.1% overvalued at $117.25, but the SWS DCF model points the other way, with a future cash flow value of $123.15. That implies a small valuation gap. Which story do you think comes closer to reality?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Akamai Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 61 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals in the story so far? With both risks and rewards identified for Akamai, move quickly, review the underlying data, and weigh the 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Akamai has caught your attention, do not stop here. Broaden your watchlist with other high quality ideas that could sharpen your overall portfolio mix.

- Target value by scanning for companies that pair quality with attractive pricing using our 61 high quality undervalued stocks.

- Strengthen your portfolio resilience by filtering for businesses with sturdier finances through the solid balance sheet and fundamentals stocks screener (39 results).

- Spot off the radar opportunities by checking the screener containing 25 high quality undiscovered gems before they are widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.