A Look At Akamai Technologies (AKAM) Valuation After Recent Gartner Recognition And Deutsche Telekom Security Partnership

Akamai Technologies, Inc. AKAM | 118.00 | +1.94% |

Why recent recognition and partnerships matter for Akamai Technologies (AKAM)

Akamai Technologies (AKAM) has been in focus after being named a Customers’ Choice in Gartner Peer Insights for network security microsegmentation, along with deeper adoption of its security services by Deutsche Telekom Security across highly targeted industries.

The recent recognition in microsegmentation and the expanded Deutsche Telekom Security partnership arrive during a period of strong share price momentum, with a 90 day share price return of 38.10% and a more modest 1 year total shareholder return of 1.68%. Together, these figures indicate that investors may be reassessing Akamai’s growth potential and risk profile in security and cloud services.

If this security themed story has your attention, it could be a moment to see what else is gaining traction in high growth tech and AI stocks as AI and cloud driven opportunities evolve.

With Akamai shares up 38.10% over 90 days but a 1-year total return of just 1.68%, and an indicated intrinsic discount of 21.70%, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 0.9% Overvalued

Akamai Technologies’ most followed narrative places fair value at $101.16, just below the latest close of $102.10, which suggests a finely balanced setup.

Surging demand for secure, low-latency cloud and edge infrastructure, driven by AI and cybersecurity needs, positions Akamai for continued top-line and margin growth through value-added solutions.

Curious what has to happen in security, compute, and AI for that valuation to hold up? The narrative leans on steadier revenue growth, rising profitability, and a future earnings multiple that assumes the business mix keeps improving. Want to see the exact earnings and margin path that underpins that fair value call?

Result: Fair Value of $101.16 (OVERVALUED)

However, you still have to weigh the risk that heavier cloud and security investment may pressure margins, and that delivery revenue or large compute contracts may fall short of expectations.

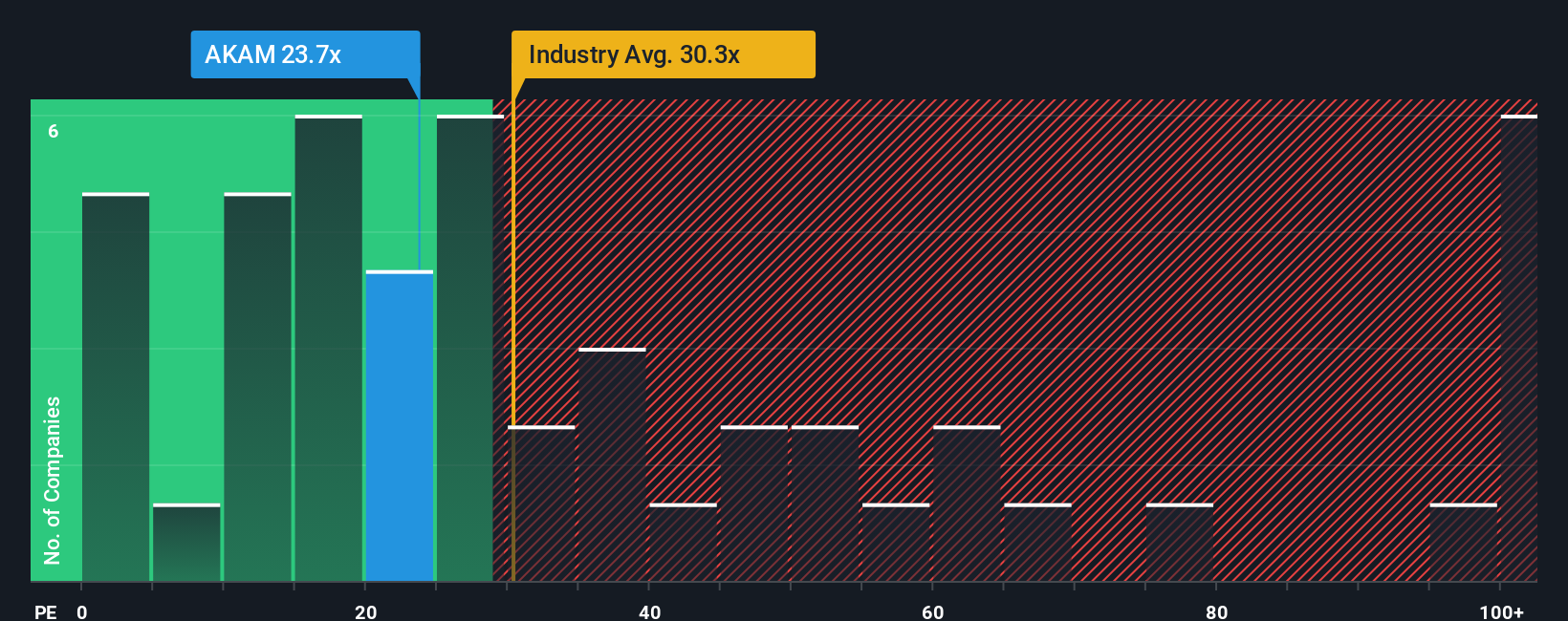

Another View: What The P/E Says

While the AI narrative pegs Akamai as 0.9% overvalued, the current P/E ratio of 29x tells a slightly different story. It sits below a fair ratio of 33.2x and below the peer average of 46.2x, and roughly in line with the US IT industry at 29.3x.

That gap suggests the market is not paying a premium for Akamai's earnings compared with peers, even as the stock trades 21.7% below one fair value estimate. Is that a signal of caution around execution, or an opening for investors willing to back the security and compute transition?

Build Your Own Akamai Technologies Narrative

If you look at the numbers and come to a different conclusion, or prefer to test your own assumptions, you can build a personalised Akamai story in just a few minutes by starting with Do it your way.

A great starting point for your Akamai Technologies research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

If Akamai has sparked your interest, do not stop here. The right screener can help you spot new ideas before they hit everyone’s radar.

- Hunt for potential setups by checking out these 3522 penny stocks with strong financials that already back their stories with stronger financials.

- Explore the next wave of AI opportunities by scanning these 23 AI penny stocks that tie artificial intelligence to real business models.

- Look for price and value alignment by filtering for these 879 undervalued stocks based on cash flows and see which companies trade below their estimated cash flow potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.