A Look At Alkami Technology (ALKT) Valuation After Launch Of One Click SDK Manager

Alkami Technology Inc ALKT | 16.56 | +3.44% |

Alkami Technology (ALKT) has rolled out its One-Click SDK Manager, a new deployment tool for its digital banking platform that aims to cut friction for developers and financial institutions using its cloud-based services.

The One-Click SDK Manager arrives at a time when Alkami Technology’s share price, at US$22.18, has seen a 7 day share price return decline of 2.20%, while its 1 year total shareholder return of 35.05% decline contrasts with a 48.66% gain over three years. This suggests that longer term momentum has been stronger than the recent pullback.

If this kind of digital banking toolkit catches your interest, it could be worth seeing how other tech names are setting up by scanning high growth tech and AI stocks today.

With Alkami trading at US$22.18 and indicators such as a value score of 2 and an estimated intrinsic discount of around 28%, the real question is whether this pullback signals an opening or if markets already see the future growth story.

Most Popular Narrative: 31.9% Undervalued

With Alkami Technology last closing at US$22.18 against a narrative fair value of about US$32.56, the valuation story leans toward upside based on projected earnings and cash flows discounted at 8.89%.

Continued rollout of new products and expansion into adjacent banking services (e.g., AI personalization, integrated data/marketing, payments), coupled with demonstrated high client retention rates, supports recurring revenue expansion and provides multiple avenues for margin improvement and long-term earnings upside.

Curious what justifies that higher fair value? The narrative leans heavily on rapid revenue compounding, earnings swinging into positive territory, and a future earnings multiple far above the sector norm. Want to see how those pieces fit together into one valuation story?

Result: Fair Value of $32.56 (UNDERVALUED)

However, softer revenue, fewer new implementations and pressure from larger fintech or big tech rivals could challenge the upbeat earnings and margin narrative that investors are leaning on.

Another View: Pricing Tension From Sales Ratios

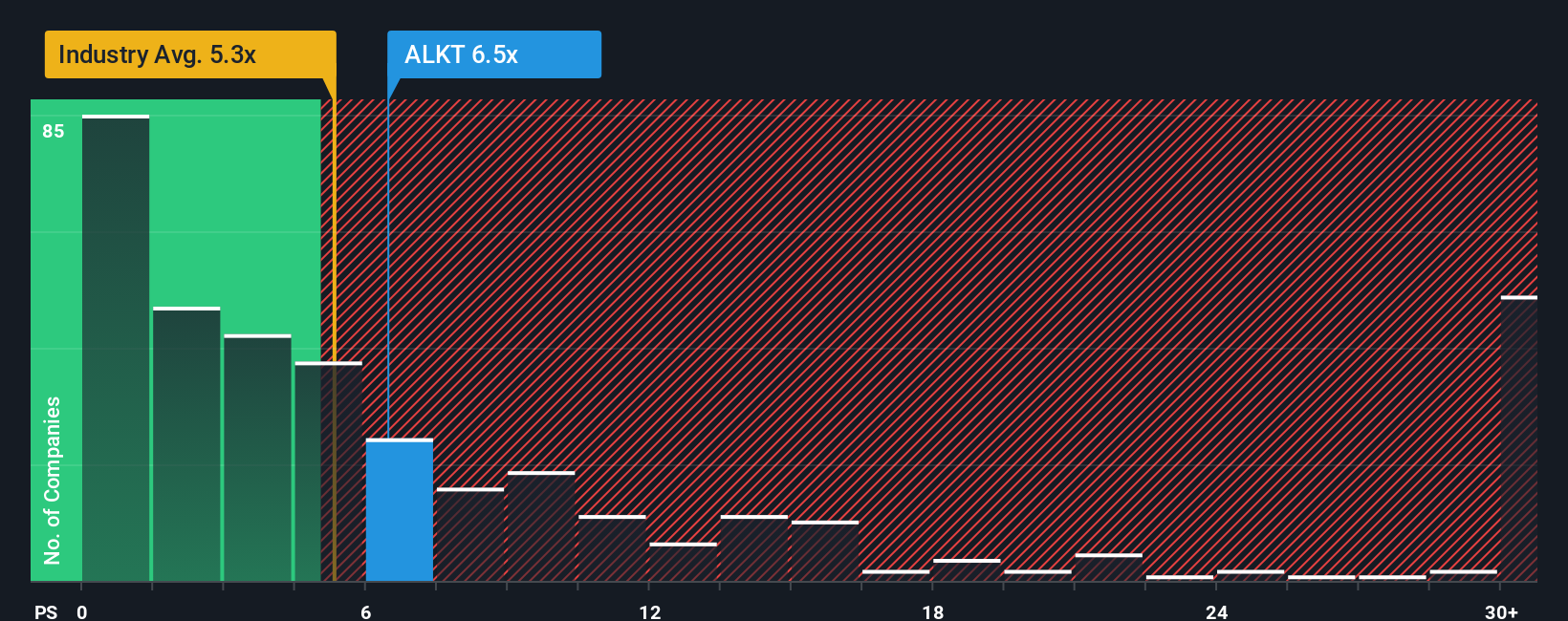

While the narrative and fair value estimates suggest Alkami Technology is trading below intrinsic value, its P/S ratio of 5.6x tells a different story. That is higher than the US Software industry at 4.9x, the peer average at 4.4x, and the fair ratio of 4.3x that the market could move toward, which points to valuation risk if sentiment cools.

So, is the current discount to fair value a cushion, or is the rich P/S multiple a sign that expectations are already running hot?

Build Your Own Alkami Technology Narrative

If you see the numbers differently, or simply prefer to test your own assumptions, you can build a custom Alkami story in minutes with Do it your way.

A great starting point for your Alkami Technology research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are weighing up Alkami, it makes sense to widen the net and compare it with other focused ideas that could sharpen your watchlist and research short-list.

- Spot potential high-upside names early by scanning these 3538 penny stocks with strong financials that already show solid financial underpinnings instead of relying on hype alone.

- Target companies riding powerful data and automation trends by running through these 28 AI penny stocks and see which ones line up with your risk and return expectations.

- Zero in on ideas where price and estimated cash flows look out of sync by checking these 879 undervalued stocks based on cash flows before the crowd starts paying closer attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.