A Look At AllianceBernstein (AB) Valuation As Analyst Targets And DCF Offer Mixed Signals

AllianceBernstein Holding L.P. AB | 0.00 |

AllianceBernstein Holding overview

AllianceBernstein Holding (AB) has drawn investor attention after recent trading, with the stock closing at $38.06 and its market value sitting around $3.6b in the US investment management sector.

Recent trading has been a bit softer, with the share price down 8.1% over the past 90 days and 2.1% over the past month. However, longer term total shareholder returns of 42.7% over three years and 30.3% over five years point to a much stronger hold period experience.

If you are comparing AllianceBernstein with other ways to put capital to work in the market, this could be a good time to broaden your search and check out 18 top founder-led companies

With the stock trading close to the latest analyst price target and recent returns mixed, the key question is whether AllianceBernstein is quietly undervalued or whether the market is already pricing in all the future growth.

Most Popular Narrative: 3.5% Undervalued

The most followed narrative puts AllianceBernstein Holding’s fair value at $39.43, a little above the last close at $38.06. This frames a modest undervaluation story.

The analysts have a consensus price target of $39.43 for AllianceBernstein Holding based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $4.4 billion, earnings will come to $275.0 million, and it would be trading on a PE ratio of 13.3x, assuming you use a discount rate of 7.8%.

If you want to understand why this fair value sits above today’s price, the narrative explains that it is based on a combination of ambitious revenue growth, slim margins and a future earnings multiple that is very different from where the broader Capital Markets group is currently priced.

Result: Fair Value of $39.43 (UNDERVALUED)

However, this setup still relies on healthy fee levels and private markets demand. As a result, fee compression or weaker alternative inflows could quickly challenge the current narrative.

Another angle on value

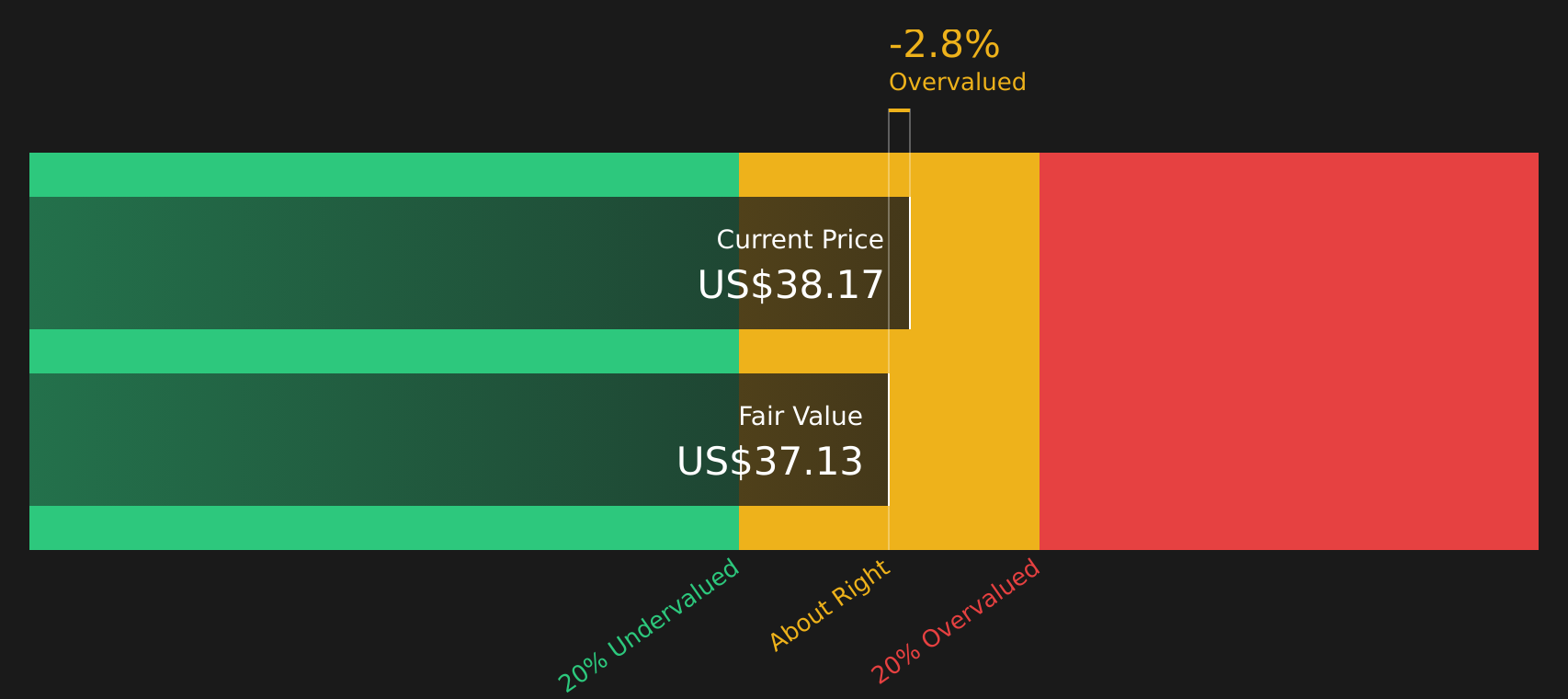

The analyst narrative points to a fair value of $39.43, which suggests mild undervaluation compared with the $38.06 share price. Our DCF model tells a different story, with a future cash flow value of $37.09, so on that view the stock looks slightly expensive. Which lens do you think fits your own assumptions better?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out AllianceBernstein Holding for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mixed signals around valuation, risks and rewards make this a good moment to look at the numbers yourself and decide what truly matters. To round out that view, focus on the 2 key rewards and 4 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that better match your goals, time horizon and comfort with risk.

- Spot potential value opportunities early by scanning screener containing 21 high quality undiscovered gems that pair strong fundamentals with lower market attention.

- Strengthen your core holdings by reviewing solid balance sheet and fundamentals stocks screener (45 results) that combine financial resilience with consistent business profiles.

- Dial back volatility while still staying invested by assessing 66 resilient stocks with low risk scores designed to highlight companies with relatively lower risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.