A Look At Allison Transmission Holdings (ALSN) Valuation As Recent Share Momentum Draws Attention

Allison Transmission Holdings, Inc. ALSN | 128.26 128.26 | -1.03% 0.00% Pre |

With no single headline event driving attention today, Allison Transmission Holdings (ALSN) is drawing interest as investors weigh its recent share performance, business profile, and current valuation signals around the stock.

The recent 30 day share price return of 11.98% and 90 day share price return of 38.80% suggest momentum has been building. The 3 year total shareholder return of 161.39% and 5 year total shareholder return of 190.39% point to a strong longer term record, despite a slightly negative 1 year total shareholder return.

If ALSN's run has you thinking about where else performance could be building, it might be a good time to scan our list of 22 power grid technology and infrastructure stocks.

Given that Allison Transmission trades near its US$114.80 analyst price target yet screens with a high intrinsic discount and strong value score, the key question is whether you are seeing a genuine opening or a market that is already pricing in future growth?

Most Popular Narrative: 13.5% Overvalued

Compared with Allison Transmission Holdings' last close at $113.75, the most followed narrative fair value of $100.20 points to a valuation gap that hinges on future execution and capital allocation.

The analysts have a consensus price target of $104.889 for Allison Transmission Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $129.0, and the most bearish reporting a price target of just $84.0.

Curious what sits behind that fair value and spread of price targets? The narrative leans heavily on ambitious revenue expansion, shifting profit margins, and a specific earnings multiple that all have to line up.

Based on that narrative, Allison Transmission's fair value of $100.20 sits around 13.5% below the current share price, using a discount rate of 9.19% and long term assumptions for revenue growth, profitability, and valuation multiples that aim to tie 2028 earnings back to today's price.

Result: Fair Value of $100.20 (OVERVALUED)

However, that story could easily change if electrification pulls demand away from traditional transmissions faster than expected or if the Dana Off-Highway acquisition underdelivers on planned synergies.

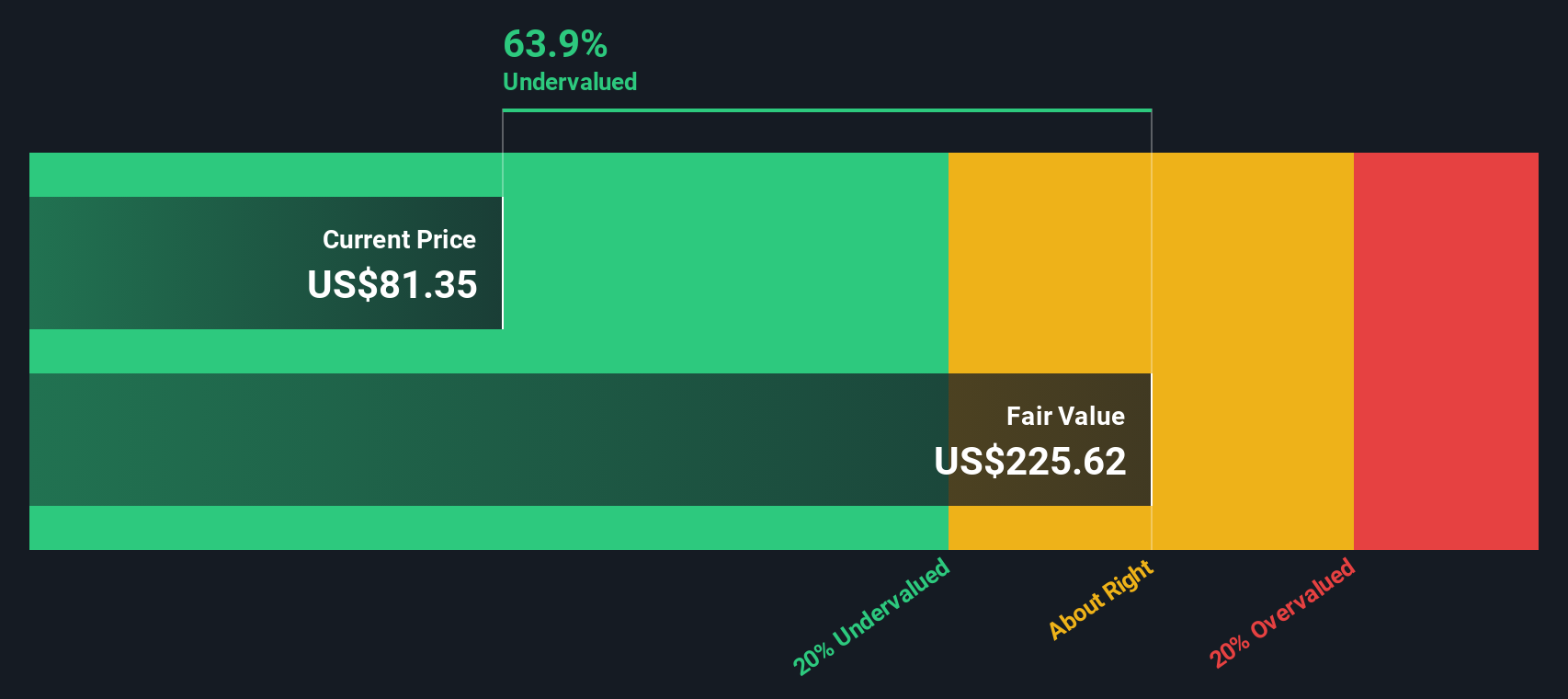

Another Angle on Value

While the consensus narrative flags Allison Transmission as about 13.5% overvalued versus a fair value of $100.20, our DCF work tells a very different story. On that view, the shares trade 53.3% below an estimated future cash flow value of $243.79, which is a wide gap for you to judge.

Build Your Own Allison Transmission Holdings Narrative

If you look at these numbers and come to a different conclusion, or simply prefer to rely on your own work, you can build a tailored view in just a few minutes with Do it your way.

A great starting point for your Allison Transmission Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Allison Transmission has sharpened your thinking, do not stop here. Use the screener to surface fresh ideas that fit the portfolio you actually want to build.

- Hunt for value by checking companies trading on appealing metrics and quality fundamentals with 55 high quality undervalued stocks that might suit a disciplined buyer.

- Prioritise resilience and sleep better at night by scanning 81 resilient stocks with low risk scores that score well on our risk checks and business stability.

- Spot earlier stage opportunities with solid financial footing using our 25 elite penny stocks with strong financials that filter for smaller names backed by stronger balance sheets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.