A Look At Alnylam Pharmaceuticals (ALNY) Valuation As 2026 Revenue Guidance Signals Strong Growth Potential

Alnylam Pharmaceuticals, Inc ALNY | 318.85 | -3.01% |

Alnylam Pharmaceuticals (ALNY) recently issued full year 2026 revenue guidance, projecting combined net product revenue of US$4.9b to US$5.3b. The company states this represents 71% growth versus 2025.

The updated 2026 revenue guidance comes after a softer patch for the share price, with a 30-day share price return of 10.64% and a 90-day share price return of 25.20%, even though the 1-year total shareholder return is 28.42% and the 5-year total shareholder return is 137.89%. Recent analyst commentary has mostly kept existing ratings in place while adjusting price expectations. This suggests the new guidance and ongoing clinical progress are being weighed against recent share price volatility.

If Alnylam’s guidance has you reassessing your healthcare exposure, this can be a good moment to scan the wider market using healthcare stocks for other potential ideas.

With Alnylam guiding to up to US$5.3 billion in 2026 revenue, a recent share price pullback, and a market price below average analyst targets, investors may be wondering whether there is still a buying opportunity here or if potential future growth is already reflected in the current valuation.

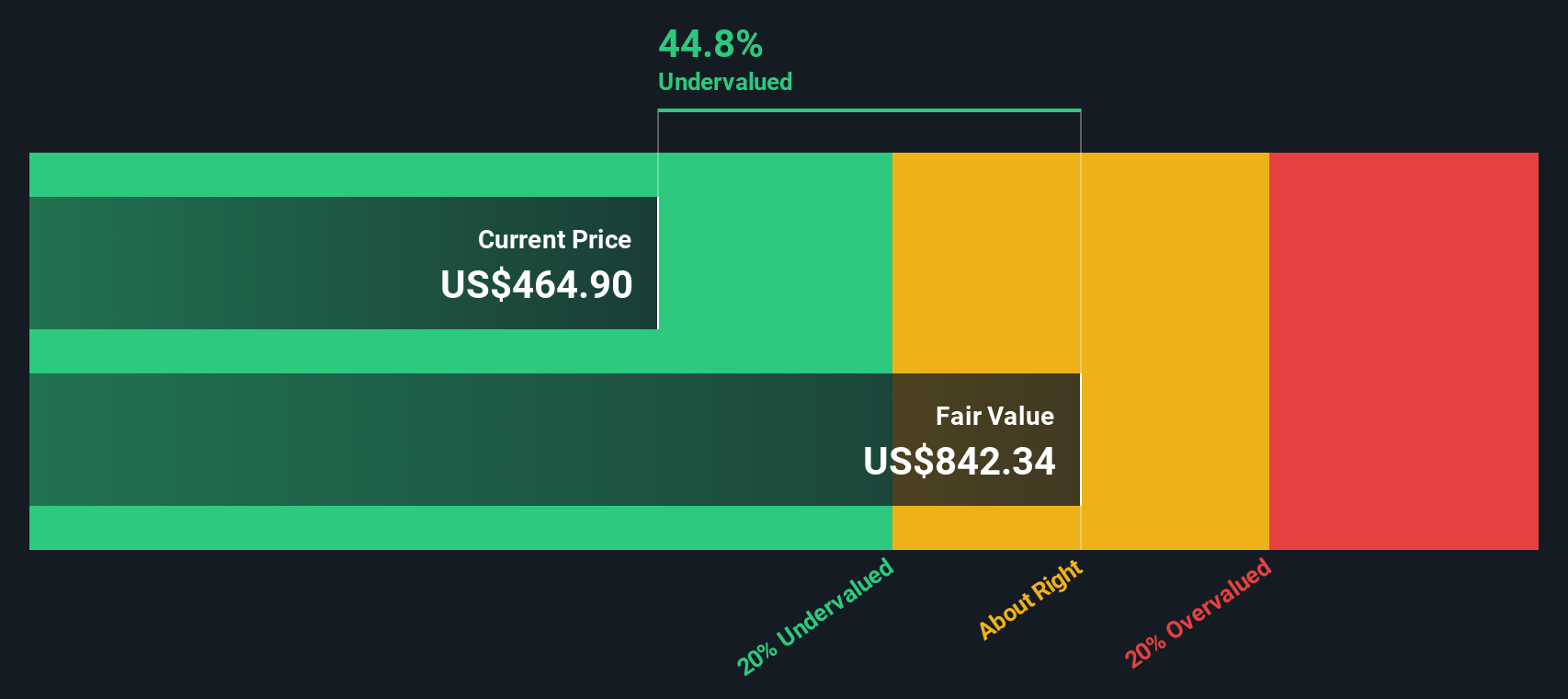

Most Popular Narrative: 27.2% Undervalued

Alnylam Pharmaceuticals’ most followed narrative points to a fair value of $491.92, compared with the last close of $357.98, framing a sizeable valuation gap for investors to consider.

The analysts have a consensus price target of $426.26 for Alnylam Pharmaceuticals based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $583.0, and the most bearish reporting a price target of just $236.0.

Curious what kind of revenue expansion, margin shift and earnings profile have to line up for that valuation view to hold? The key factors include how quickly profitability scales, how long high growth is assumed to last, and what type of premium multiple the company is given at the end of the forecast window. If you want to see exactly which assumptions carry the most weight in that fair value, the full narrative lays them out step by step.

Result: Fair Value of $491.92 (UNDERVALUED)

However, heavy reliance on the TTR franchise, along with potential pricing or reimbursement pressure, could quickly challenge the optimistic revenue and margin assumptions investors are currently debating.

Another View: Rich On Sales, Even If Cash Flows Look Attractive

Our DCF model flags Alnylam as trading about 58.6% below an estimated future cash flow value of $864.08 per share, which points to an undervalued picture. Yet the market is already paying 14.7x sales versus a 11.9x industry average, so how comfortable are you with paying a premium for that cash flow story?

Build Your Own Alnylam Pharmaceuticals Narrative

If you see the numbers differently, or prefer to test your own assumptions against the data, you can build a custom view in minutes with Do it your way.

A great starting point for your Alnylam Pharmaceuticals research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas beyond Alnylam?

If you are weighing what to do next, do not stop with one stock. Use the screeners to pressure test your thinking across different corners of the market.

- Spot potential value in overlooked cash flow stories by checking out these 871 undervalued stocks based on cash flows that might fit your return and risk preferences.

- Explore AI trends by scanning these 23 AI penny stocks where earnings potential and real world use cases are already in focus.

- Identify income themed ideas with these 13 dividend stocks with yields > 3% that could help you build a more resilient, cash focused portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.