A Look At American Eagle Outfitters (AEO) Valuation After Record Q1 Revenue And Reaffirmed Outlook

American Eagle Outfitters, Inc. AEO | 0.00 |

American Eagle Outfitters (AEO) stock is back in focus after the retailer posted record first quarter revenue and reaffirmed its full year operating income outlook, supported by strong Aerie and Offline performance.

Yet despite the earnings beat and reaffirmed outlook, the stock has fallen about 30% on a 3 month share price return and is down around 40% year to date. The 1 year total shareholder return of roughly 49% still reflects a much stronger longer term picture as investors reassess growth prospects and tariff risks.

If this kind of volatility has you looking beyond apparel, it could be a good moment to scan other themes and check out 20 top founder-led companies

With record quarterly revenue, double digit same store sales growth and guidance that still points to higher comparable sales, the recent share price slide raises a simple question for you: Is this a reset that creates opportunity, or a signal that the market is already pricing in the growth story ahead?

Most Popular Narrative: 33.9% Undervalued

With American Eagle Outfitters last closing at $15.80 against a narrative fair value of $23.89, the market price and consensus story are clearly not aligned.

American Eagle Outfitters is expanding brand awareness and strengthening customer engagement with targeted strategies, particularly for Aerie and OFFLINE. By increasing brand visibility and expanding collections, they aim to drive strong revenue growth.

Want the full picture behind that valuation gap? The narrative leans on steady revenue expansion, higher margins and a future earnings multiple that may surprise you.

Result: Fair Value of $23.89 (UNDERVALUED)

However, there are still clear watchpoints, including softer consumer demand and potential tariff or currency pressures that could squeeze revenue and margins if conditions worsen.

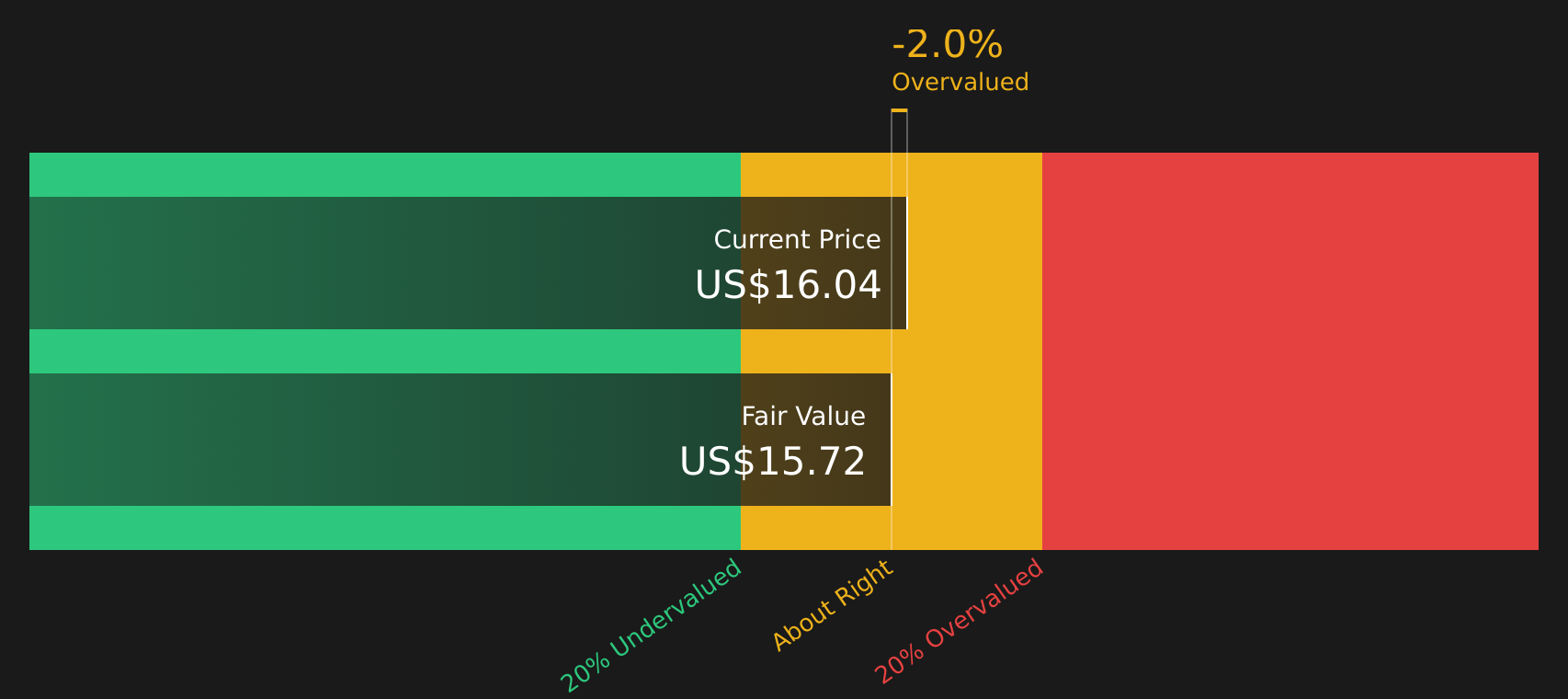

Another View: DCF Says AEO Is Fairly Priced

While the narrative fair value points to American Eagle Outfitters trading at a 33.9% discount, the SWS DCF model tells a cooler story. On projected future cash flows, the stock appears close to fair value at about $15.48, which limits the margin of safety implied by that first approach.

DCF models are sensitive to small shifts in growth or discount rate inputs. However, they also direct attention to cash generation rather than headline earnings. If cash flow assumptions prove too optimistic or too cautious, how much weight would you still put on that 33.9% undervaluation?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out American Eagle Outfitters for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of caution and opportunity feels familiar, take a closer look at the data now and decide where you stand with 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop with just one stock, you could miss opportunities that fit your goals even better, so use the screener to widen your watchlist intelligently.

- Strengthen your core holdings by checking companies with robust finances through the solid balance sheet and fundamentals stocks screener (46 results).

- Target value opportunities by scanning companies that look mispriced using the 46 high quality undervalued stocks.

- Add potential future standouts by reviewing the screener containing 22 high quality undiscovered gems before others start paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.