A Look At American Electric Power Company (AEP) Valuation After Earnings Beat Dividend Hike And Capital Plan Update

American Electric Power Company, Inc. AEP | 132.68 | +0.77% |

American Electric Power Company (AEP) just posted quarterly earnings and revenue ahead of analyst expectations, raised its quarterly dividend, reaffirmed 2026 earnings guidance, and highlighted a large multiyear capital plan tied to rising data center demand.

The strong Q4 update, higher dividend, reaffirmed 2026 outlook and large capital plan have come alongside a 1 year total shareholder return of 31.86% and a year to date share price return of 12.20%. This suggests that momentum has been building recently.

If this update has you thinking more broadly about power infrastructure and grid demand, it could be worth scanning 25 power grid technology and infrastructure stocks as a starting list of potential ideas.

With AEP shares returning 31.86% over the past year and recently trading near the average analyst price target, the key question now is whether the strong earnings, dividend and capital plan still leave upside on the table, or if markets are already pricing in future growth.

Most Popular Narrative: 1% Overvalued

At a last close of $129.94 versus a most followed fair value estimate of $128.75, AEP is framed as slightly premium to that narrative, which leans on detailed growth and discount rate assumptions rather than big headline calls.

The analysts have a consensus price target of $115.0 for American Electric Power Company based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $24.6 billion, earnings will come to $4.1 billion, and it would be trading on a PE ratio of 18.5x, assuming you use a discount rate of 6.8%.

Curious how AEP gets from today’s earnings to that higher profit base and premium P/E in just a few years? The narrative quietly leans on assumptions of steadier revenue compounding, slightly thinner margins, and a valuation reset that still sits below where many peers trade. The details behind that mix of growth, profitability and discount rate assumptions are where the real story lives.

Result: Fair Value of $128.75 (OVERVALUED)

However, the story can change quickly if commercial and industrial load growth falls short of expectations, or if regulatory shifts in key states slow project approvals.

Another Angle On Value

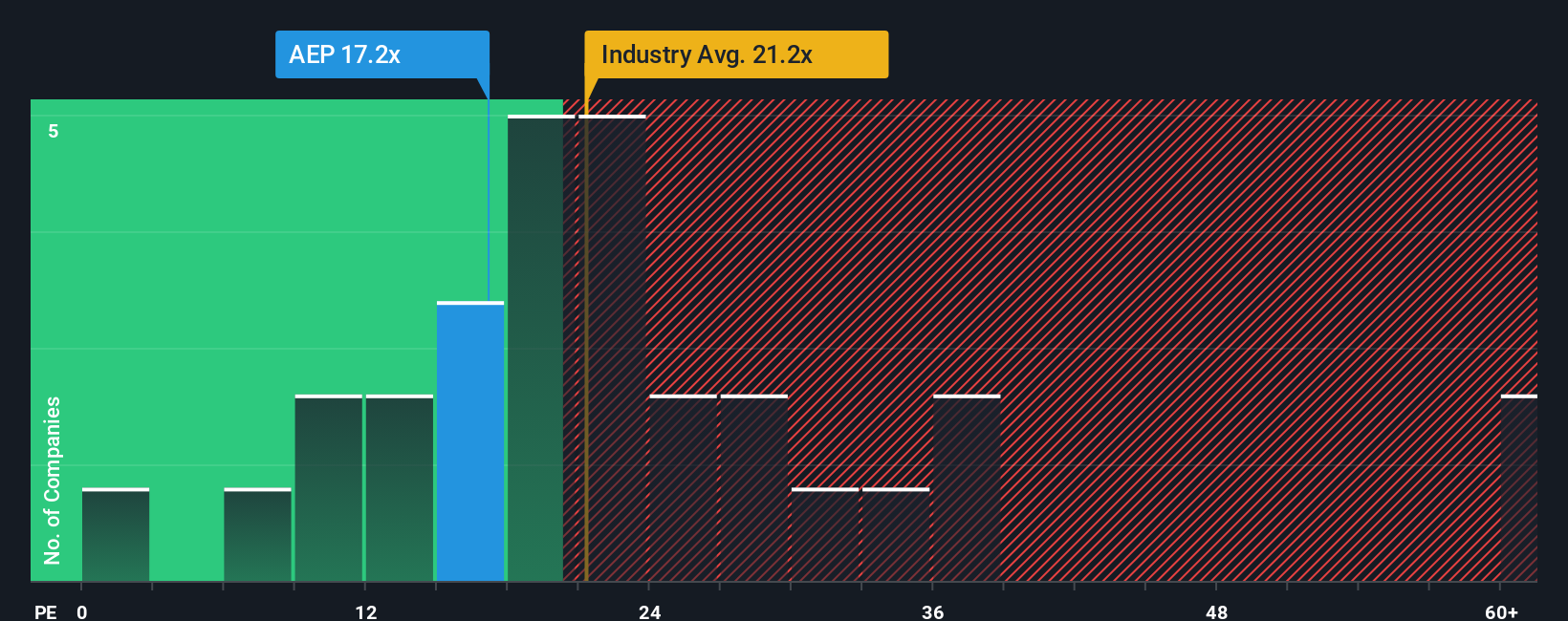

While the narrative pegs AEP at around 1% above fair value, its P/E of 19.4x is below the US Electric Utilities average of 21.9x and under a fair ratio of 25x. That gap points to some valuation cushion, so is the premium label too harsh here?

Build Your Own American Electric Power Company Narrative

If the story laid out here does not quite fit how you see AEP, or you prefer to weigh the data yourself, you can put together a custom view of the company in just a few minutes and Do it your way.

A great starting point for your American Electric Power Company research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Ready To Hunt For Your Next Idea?

If you stop with just one stock, you risk missing other opportunities quietly lining up on your watchlist, so put the Simply Wall St Screener to work for you.

- Target quality at a discount by checking companies our screener tags as 53 high quality undervalued stocks with strong fundamentals and room for potential re rating.

- Lock in potential income ideas by scanning 13 dividend fortresses that pair higher yields with resilient payout profiles.

- Prioritize resilience by reviewing 85 resilient stocks with low risk scores that score well on stability and financial strength, before the crowd catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.