A Look At Aon (AON) Valuation After Its New GLP 1 Employer Health Outcomes Study

Aon Plc Class A AON | 323.14 | +0.56% |

Aon (AON) is back in focus after releasing fresh findings from its multi year GLP 1 study, which links sustained use of these therapies to slower medical cost growth for employers and better health outcomes for covered workers.

At a share price of $338.69, Aon’s 1 day share price return of 0.81% comes after a softer patch, with a 30 day share price decline of 5.04% and a 1 year total shareholder return decline of 9.37%. The 5 year total shareholder return of 70.09% shows that longer term holders have still seen solid gains as the company rolls out new research, leadership appointments and product launches.

If this GLP 1 work has you thinking more broadly about health risk, it could be a good moment to scan healthcare stocks for other insurance and healthcare names shaping employer benefits.

With the shares trailing their 1 year and year to date returns, while sitting about 17% below the average analyst price target, is Aon offering value after a reset, or is the market already pricing in its next chapter?

Most Popular Narrative: 14.2% Undervalued

Aon’s most followed narrative pegs fair value at $394.84 versus the $338.69 last close, framing the current pullback against a higher long term outlook.

Aon's 3x3 Plan and the deployment of Risk Analyzers have increased new business and improved client retention, strengthening the foundation for ongoing revenue growth and margin expansion. Investment in priority hires and expanding Aon Business Services (ABS) capabilities are creating capacity to fund growth initiatives and drive operational efficiencies, benefiting net margins and earnings.

Curious what sits behind that fair value gap? The narrative leans heavily on compounded revenue gains, thicker margins, and a future earnings multiple that is described as anything but conservative.

Result: Fair Value of $394.84 (UNDERVALUED)

However, softer P&C pricing and higher debt costs could pressure Aon’s revenue growth and margins, which challenges the idea that today’s discount reflects easy upside.

Another View: Rich Multiples Temper The Undervaluation Story

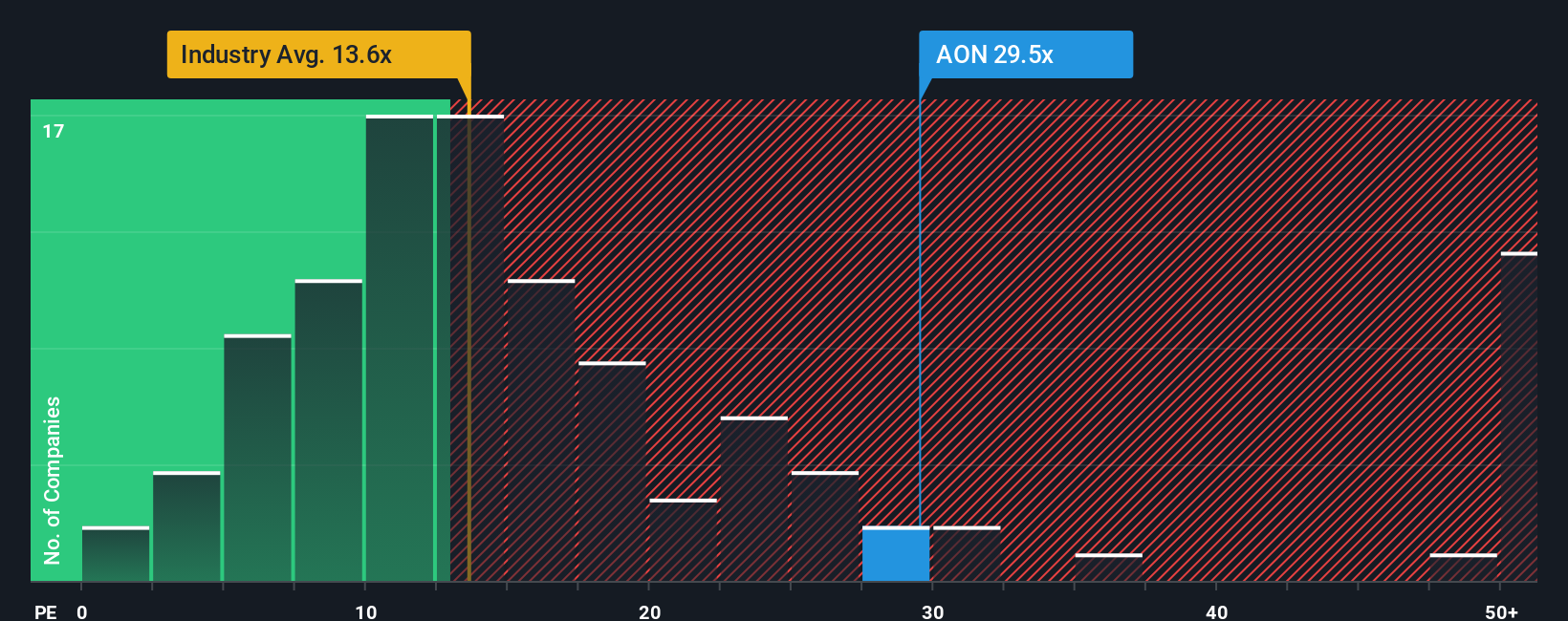

The narrative flags Aon as 14.2% undervalued on fair value, yet the current P/E of 26.8x sits well above both the US Insurance industry at 12.7x and peers at 26.1x, and also above a fair ratio of 15.9x. That gap points to valuation risk rather than a clear bargain, so which signal do you trust?

Build Your Own Aon Narrative

If you see the numbers differently or want your own angle on Aon’s story, you can spin up a custom narrative in minutes, Do it your way.

A great starting point for your Aon research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop with Aon, you could miss other setups that fit your style, so put the Simply Wall St Screener to work and widen your opportunity set.

- Spot potential fast movers early by scanning these 3521 penny stocks with strong financials that combine smaller market sizes with stronger balance sheets and cleaner financial profiles than many expect.

- Tap into the push toward smarter software by checking out these 23 AI penny stocks shaping everything from automation to data driven decision tools across multiple industries.

- Hunt for price gaps by reviewing these 867 undervalued stocks based on cash flows where current market prices sit below cash flow based fair value estimates.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.