A Look At Apellis Pharmaceuticals (APLS) Valuation After The Biogen Acquisition Announcement

Apellis APLS | 0.00 |

Why Apellis Pharmaceuticals (APLS) Is On Investors’ Radar

Apellis Pharmaceuticals (APLS) has drawn fresh attention after being acquired by Biogen, with the company now operating as a subsidiary as of May 14, 2026, while its stock continues to trade independently.

At a share price of US$41.03, Apellis has seen a sharp 90 day share price return of 89.08% and a 1 year total shareholder return of 135.13%. However, the 3 year total shareholder return is down 53.83%, so recent momentum contrasts with a weaker longer term record.

If you are curious about where else capital is moving in healthcare related AI, it is worth scanning 32 healthcare AI stocks

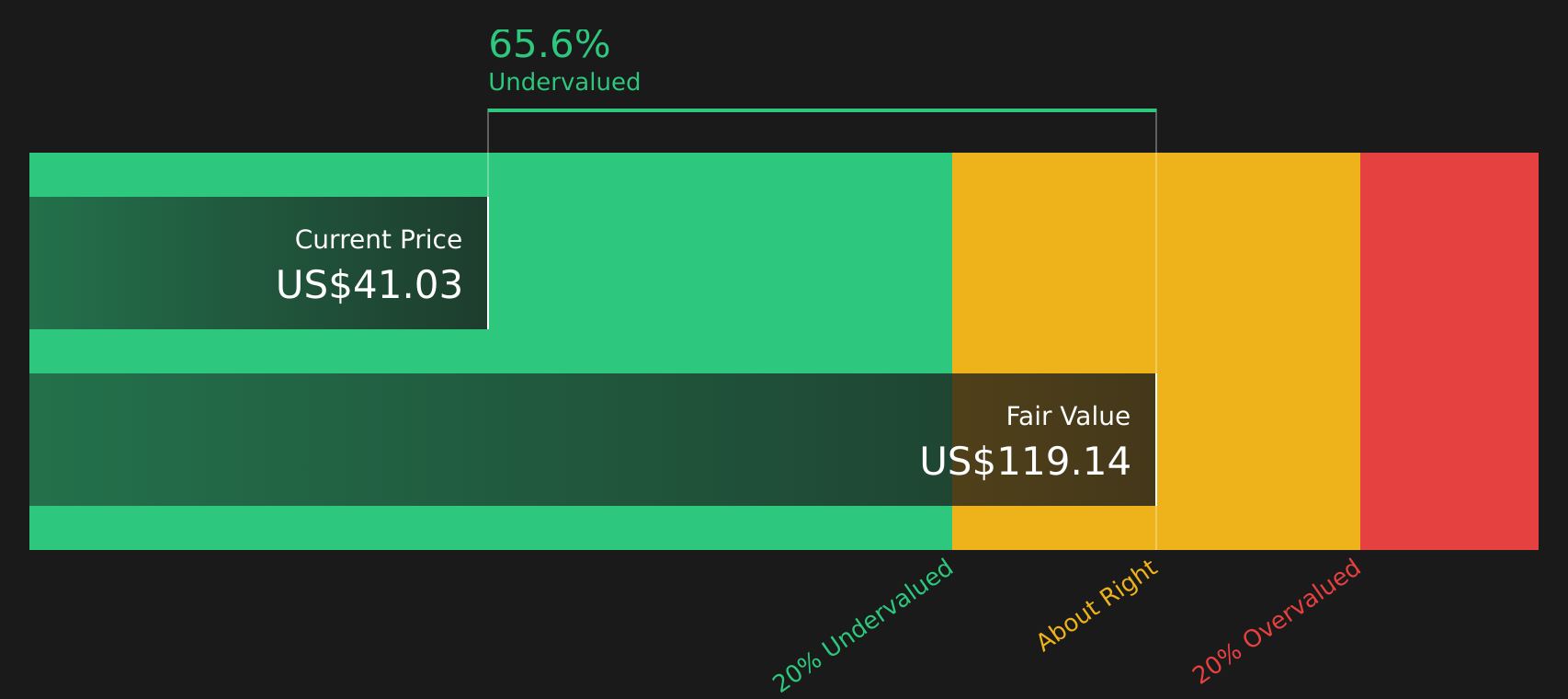

With Apellis trading at US$41.03, very close to its analyst price target but showing a sizeable intrinsic discount estimate, investors have to decide whether there is still hidden value here or whether the market is already pricing in future growth.

Most Popular Narrative: 20% Overvalued

Apellis is trading at about $41.03 against a widely followed fair value estimate of about $40.93, and the gap is small enough that the underlying story matters more than the headline number.

SYFOVRE maintains strong market leadership in geographic atrophy (GA), with over 60% market share and only ~10% market penetration to date, leaving significant runway for patient expansion as the global population ages and adoption among specialists and general ophthalmologists rises. Steady injection growth and broader awareness should drive increasing revenues over the long term.

Curious what kind of revenue curve sits behind that confidence, how profit margins are expected to shift, and which earnings multiple ties it all together? The full narrative walks through those assumptions in detail, including how fast analysts think profits step up and what discount rate is used to pull everything back to today.

Result: Fair Value of $40.93 (OVERVALUED)

However, the story can change quickly if SYFOVRE adoption or pricing falls short of expectations, or if key EMPAVELI trials in new kidney indications disappoint.

Another Angle On Value

The consensus narrative pegs Apellis as roughly fairly priced around $40.93, yet the SWS DCF model presents a different perspective, with a future cash flow value of $119.14 per share that suggests the stock is trading at a large discount. Which story do you think is closer to reality?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Apellis Pharmaceuticals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and sentiment, now is the time to check the underlying data yourself, weigh both sides, and see the full picture through 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If Apellis has sharpened your thinking, do not stop here. Use the Simply Wall St screener to uncover fresh opportunities that match your style before others move first.

- Target quality at a discount by scanning 50 high quality undervalued stocks that combine sensible valuations with fundamentals many investors overlook.

- Prioritize resilience by reviewing 66 resilient stocks with low risk scores that score well on stability so short term swings are less likely to rattle your portfolio.

- Spot future standouts early by checking the screener containing 22 high quality undiscovered gems before they draw wider market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.