A Look at Aramark’s (ARMK) Valuation After New Guidance, Segment Sale, and Dividend Boost

Aramark ARMK | 42.55 | +1.60% |

Aramark revealed several updates that caught investors' attention this week. These include its latest annual 10-K filing, new fiscal 2026 revenue guidance, and a 14% boost to its quarterly dividend payout.

Aramark’s recent moves, including a major segment divestiture and the launch of advanced hospitality solutions, landed just as its stock has struggled to maintain upward momentum. While the past twelve months show a total shareholder return of -7.7%, its three- and five-year total returns of 26% and 42% hint at longer-term strength and resilience amid changing market dynamics and new growth strategies.

If these developments have you curious about other industry standouts, it’s a great time to broaden your search and discover fast growing stocks with high insider ownership

With Aramark trading at a noticeable discount to analyst price targets and delivering double-digit dividend growth, investors may be considering whether this is a compelling entry point for value-focused portfolios or if the market is already factoring in its next stage of expansion.

Most Popular Narrative: 16.3% Undervalued

With Aramark’s last close at $37.17 and the most popular narrative estimating fair value at $44.43, expectations for a potential re-rating stand out against the subdued share performance. Here is a catalyst from the consensus view fueling that optimism:

Accelerating wins of large, multi-year contracts, particularly in Sports & Entertainment, Education, and Healthcare, as organizations turn to outsourcing non-core services, point to sustained, above-trend future revenue growth and long-term contract expansion. Expansion in international markets, with double-digit organic growth in regions like the U.K., Chile, and Spain, and strategic wins in healthcare and entertainment sectors, demonstrates a deliberate move to diversify and lower cyclicality, which should bolster overall revenue and earnings stability.

Want to know what makes Aramark’s valuation tick? The narrative combines ambitious contract expansion with a bold growth forecast and margin rebound. Uncover the factors driving the analysts’ fair value, and see what is fueling their conviction and raising eyebrows on Wall Street.

Result: Fair Value of $44.43 (UNDERVALUED)

However, persistent labor cost pressures or delays in ramping up new contracts could quickly dampen the upside in Aramark’s growth story.

Another View: What Do the Numbers Really Say?

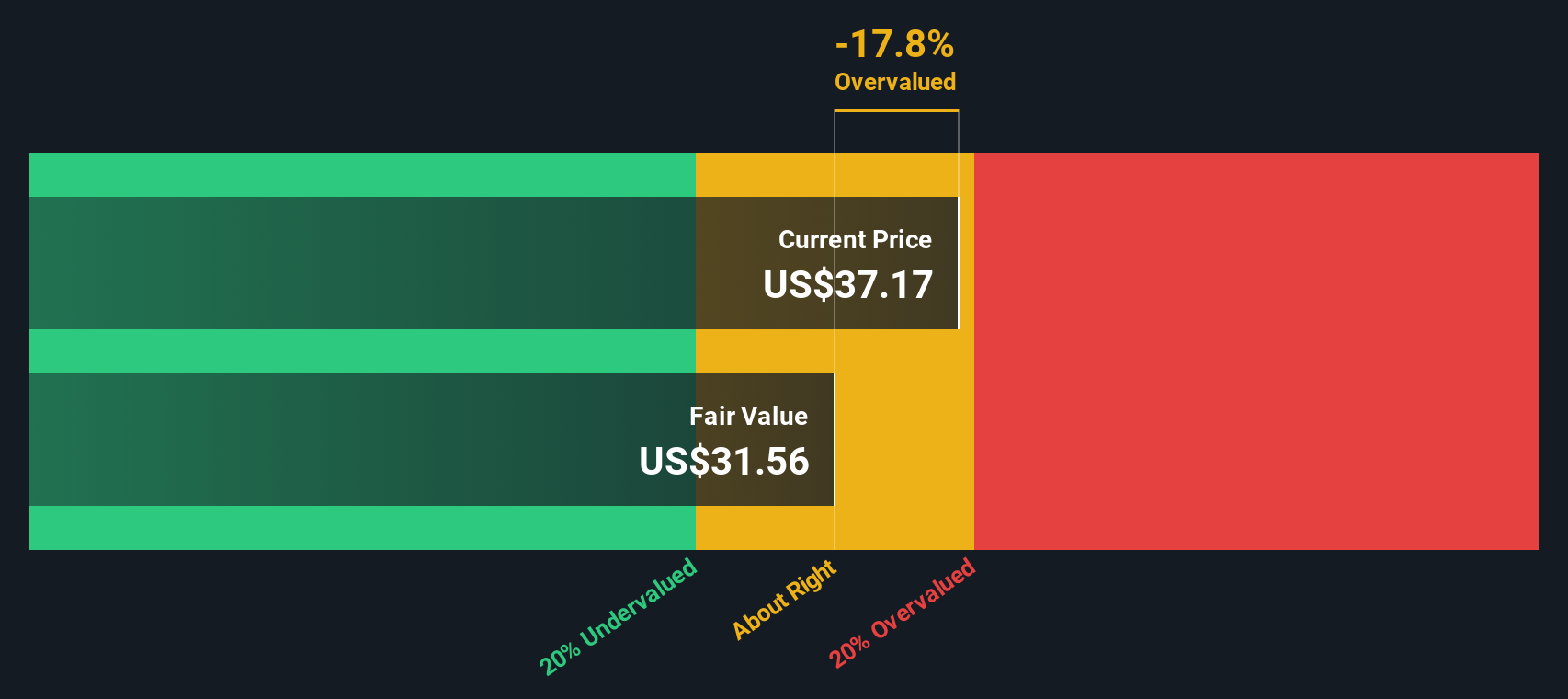

While the consensus narrative labels Aramark as attractive, our SWS DCF model takes a more cautious stance. It pegs fair value at $31.56, below today’s price. This suggests Aramark could be trading above its underlying worth. Does DCF highlight hidden risks, or is the market seeing something more?

Build Your Own Aramark Narrative

If you want to go beyond consensus or dig into the details yourself, you can easily put together your own take. Doing so takes less than three minutes. Do it your way

A great starting point for your Aramark research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Step ahead of the crowd and position yourself for tomorrow's opportunities by targeting unique growth areas, income streams, and disruptive trends that others might miss.

- Capitalize on potential market upswings by reviewing these 920 undervalued stocks based on cash flows, filled with companies trading below their intrinsic values and primed for re-rating.

- Boost your portfolio’s yield by locking in passive income through these 15 dividend stocks with yields > 3%, featuring stocks with reliable payouts and attractive returns above 3%.

- Ride the next wave of innovation by tapping into the future with these 25 AI penny stocks and see which companies are set to redefine industries through artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.