A Look At ArcBest (ARCB) Valuation After Its Recent Share Price Surge

ArcBest Corporation ARCB | 0.00 |

ArcBest (ARCB) is catching investor attention after a strong run in the stock, with returns of 37.4% over the past month and 77.5% over the past 3 months, prompting closer scrutiny of fundamentals.

At a share price of US$166.22, ArcBest’s recent gains have been rapid, with strong short term share price returns building on already solid multi year total shareholder returns. This may indicate shifting expectations around its growth prospects and risk profile.

If ArcBest’s surge has you thinking about what else is moving in logistics and infrastructure, it could be a good time to scan 34 power grid technology and infrastructure stocks

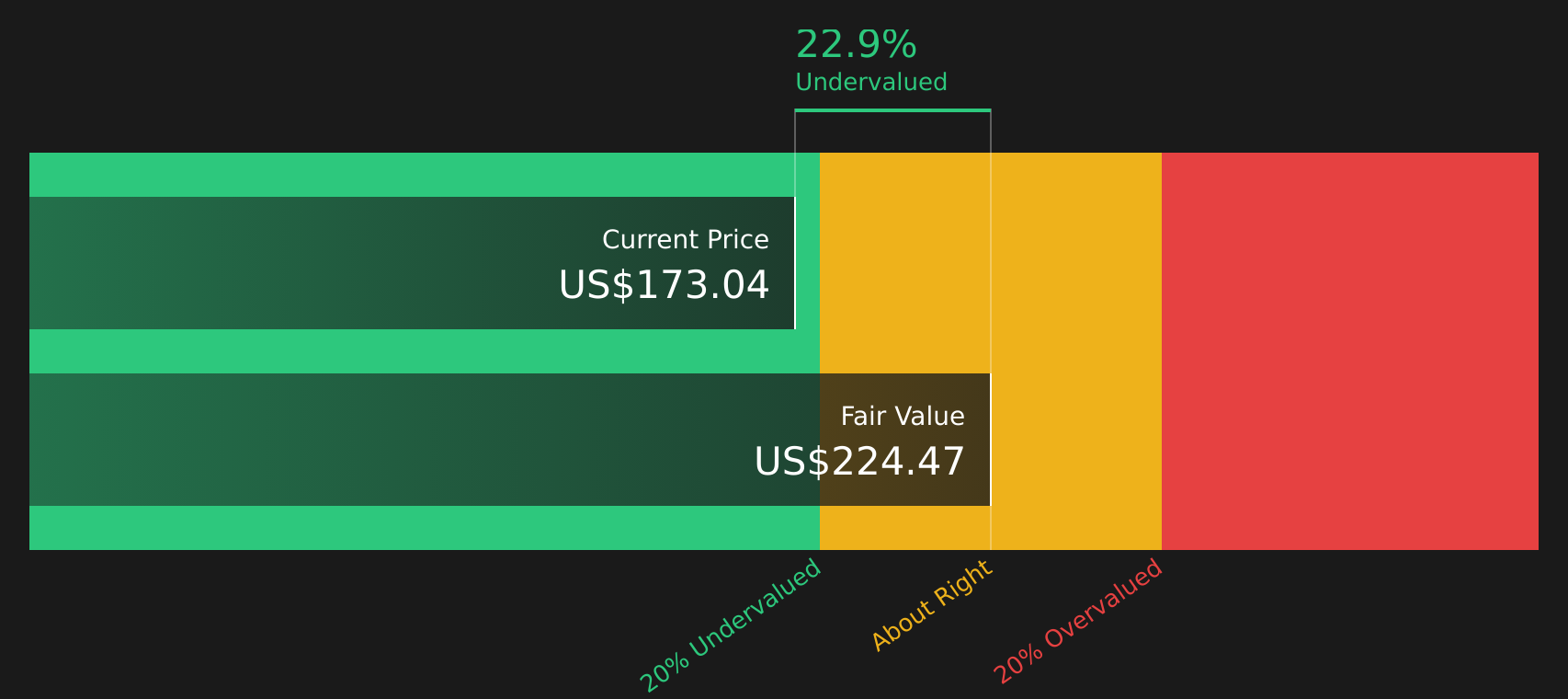

With ArcBest trading at US$166.22 and showing an intrinsic discount of about 21%, the key question is whether the stock still offers value or if the market is already pricing in much stronger future growth.

Most Popular Narrative: 71% Overvalued

ArcBest’s most followed narrative points to a fair value of about $97.42, well below the last close of $166.22, which raises clear questions about how much future execution is already baked into the price.

Broad deployment of AI-driven optimization tools, such as real-time route and dock management systems, are driving measurable productivity gains and cost savings. These are expected to translate into improved net margins and operational earnings as automation and technology adoption intensify across the industry.

Curious what earnings profile and long term margin path underpin that gap between fair value and today’s price? The narrative leans on compounding revenue, a reset in profitability, and a future earnings multiple that sits below many transport peers but still implies a material upgrade from current levels.

Result: Fair Value of $97.42 (OVERVALUED)

However, softer freight demand and persistent rate pressure, together with higher labor costs, could easily limit the margin and earnings path that this narrative relies on.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another Angle on Value

While the SWS DCF model points to ArcBest trading about 21% below an estimated future cash flow value of US$209.55, the stock also sits on a P/E of 66.2x versus a fair ratio of 34x and a US Transportation industry average of 39.6x. This suggests a rich pricing point that could leave less room for disappointment if expectations reset.

For a closer look at how those cash flow assumptions stack up against the current price, and how sensitive that view is to margins and growth, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ArcBest for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Balancing upbeat returns with real questions about valuation and execution risk is never straightforward, so do not let the headline figures tell the whole story. If you want to weigh the upside against the downside for yourself, start by reviewing the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If ArcBest’s run has sharpened your focus, do not stop here. Broaden your watchlist with targeted stock ideas that match the type of opportunities you care about most.

- Target value potential by checking companies that appear mispriced on quality and fundamentals through the 47 high quality undervalued stocks.

- Boost income potential by scanning for reliable high yield opportunities using the 10 dividend fortresses.

- Prioritize resilience by reviewing companies with strong finances through the 63 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.