A Look At Arcos Dorados (NYSE:ARCO) Valuation After New 2026 Comparable Sales Guidance

Arcos Dorados Holdings, Inc. Class A ARCO | 8.72 | +1.04% |

Arcos Dorados Holdings (ARCO) issued fresh guidance for the first quarter of 2026, indicating higher systemwide comparable sales growth compared with late 2025, with stronger local currencies expected to support additional US dollar revenue.

The fresh guidance comes after a 9.42% 1 month share price return and a 14.68% year to date share price return to US$8.36. The 5 year total shareholder return of 74.54% contrasts with a more modest 1 year total shareholder return of 1.95%, suggesting momentum has picked up recently compared with longer term gains.

If this update has you thinking about where else consumer facing growth could come from, it might be a good time to scan our 23 top founder-led companies as another source of potential ideas.

Given the recent share price gains, mixed profit growth and guidance pointing to higher comparable sales with currency support, the key question now is whether Arcos Dorados is still undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 12% Undervalued

With Arcos Dorados last closing at $8.36 against a most followed narrative fair value of $9.50, the gap hinges on how growth and margins evolve from here.

Continued digital adoption, including loyalty program rollouts, app engagement, and digital ordering, are driving higher visit frequency, stronger customer retention, and higher identified sales, which is likely to support future revenue growth and improve gross margins as digital channels scale.

Want to see what sits behind that $9.50 figure? Revenue expectations, margin shifts, and a future earnings multiple all come together here. The tension between current guidance and those long term assumptions is where the story really gets interesting.

Result: Fair Value of $9.50 (UNDERVALUED)

However, you still need to weigh risks such as softer consumer demand in Brazil and higher beef costs, which could pressure margins and slow the recovery story.

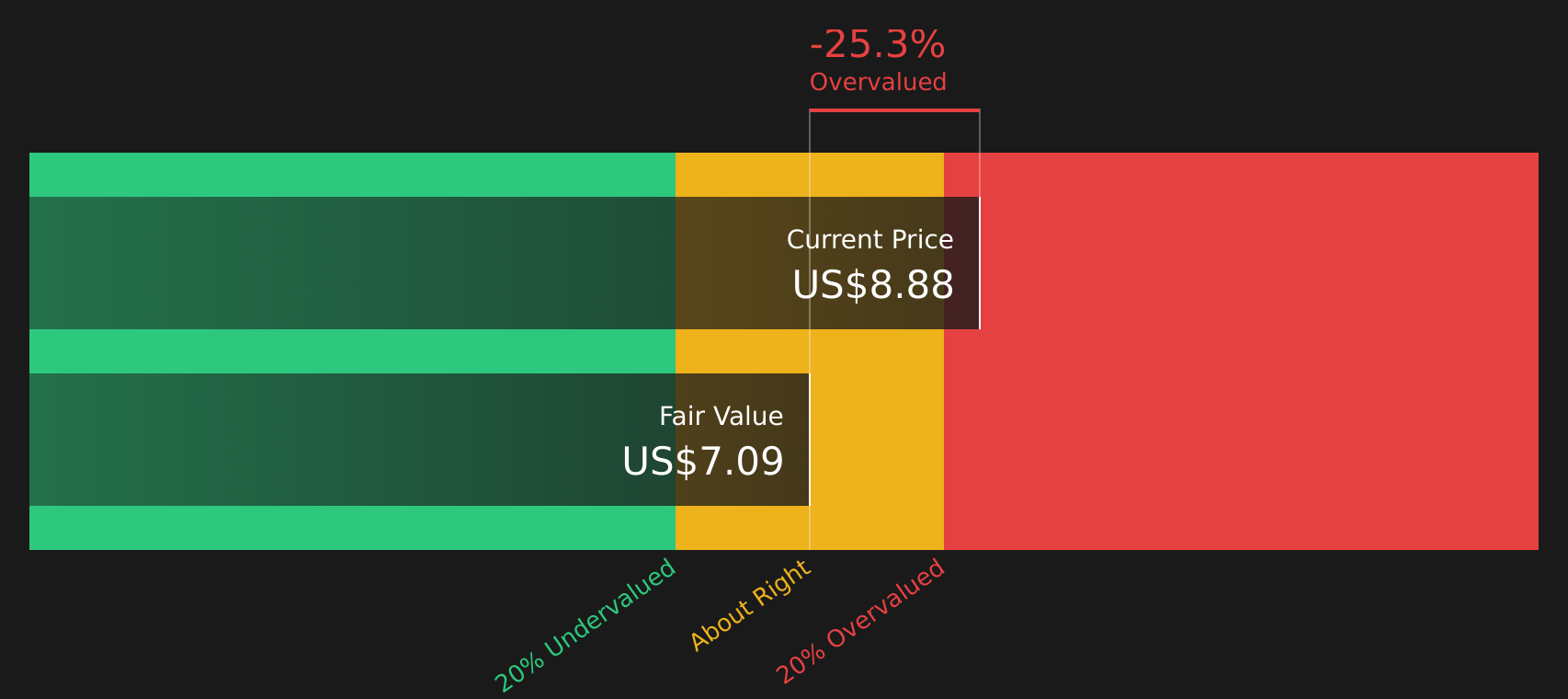

Another View Using Cash Flows

There is a twist when you look at Arcos Dorados through our DCF model. On this approach, the fair value sits at $6.94, below the current $8.36 share price. This suggests the stock may be trading at a premium instead of being 12% undervalued. Which interpretation do you think aligns better with your own expectations?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Arcos Dorados Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Arcos Dorados Holdings Narrative

If you see the data differently or just prefer to test your own assumptions, you can build a custom Arcos Dorados view in minutes: Do it your way.

A great starting point for your Arcos Dorados Holdings research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop with just one company today, you could miss opportunities that better fit your goals, so give yourself options with a quick screener check.

- Target potential upside by scanning 53 high quality undervalued stocks, a group of companies that pair solid fundamentals with prices the market may not fully appreciate yet.

- Strengthen your income focus by reviewing 13 dividend fortresses, a set of 5%+ yield candidates where payouts sit at the center of the story.

- Simplify risk management by shortlisting 85 resilient stocks with low risk scores, so you are not ignoring companies with steadier profiles while you research higher octane ideas.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.