A Look At Arista Networks (ANET) Valuation After Earnings Beat And Fresh AI Infrastructure Endorsements

Arista Networks, Inc. ANET | 126.25 | -0.34% |

Arista Networks (ANET) is back in focus after recent earnings outperformance and fresh endorsements as an AI infrastructure pick, prompting investors to reassess how its networking business lines up with the AI data center buildout.

The recent earnings beat and fresh AI-focused endorsements have arrived after a choppy few months, with the share price now at US$143.72 and recent momentum turning positive. This includes a 9.01% 1 month share price return and a 7.57% year to date share price return, while the 1 year total shareholder return of 43.29% and a very large 5 year total shareholder return show how strongly long term holders have been rewarded.

If Arista’s AI story has your attention, it could be a good moment to see what else is moving in related areas through high growth tech and AI stocks.

With ANET trading at US$143.72, a discount to some analyst targets but following a strong multiyear run, the key question now is whether there is still an opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 12% Undervalued

With Arista Networks trading at $143.72 against a widely followed fair value estimate of $163.37, the current price sits below that narrative anchor, which is built on detailed revenue, margin and valuation assumptions.

The renewed investment cycles in cloud infrastructure, driven by new traffic requirements from distributed AI workloads and front-end/top-of-rack network refreshes (for example, from 100G to 400G and 800G), create a robust pipeline for Arista's next-gen switching and routing products, underpinning both revenue and margin expansion as the company benefits from high-value product cycles.

Curious what kind of growth path and profit profile has to line up for that fair value to hold? The narrative leans on ambitious revenue scaling, firm margins and a future earnings multiple more often associated with market leaders. Want to see how those ingredients combine into that figure? Read on to see the full set of assumptions behind this pricing story.

Result: Fair Value of $163.37 (UNDERVALUED)

However, you also need to keep an eye on customer concentration and rising competition, either of which could quickly challenge the AI driven growth thesis you just read.

Another View: High Multiple, Different Message

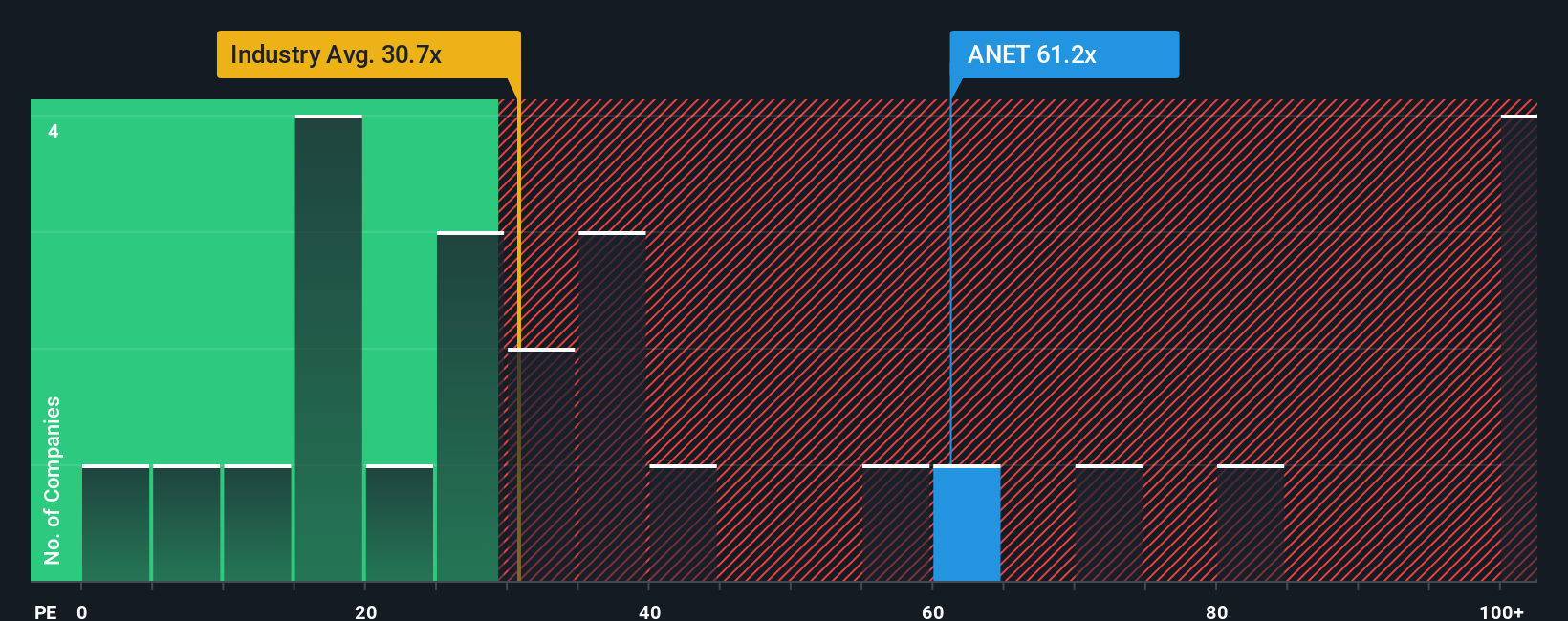

While the fair value narrative pegs Arista at $163.37, the current P/E of 53.9x tells a tougher story. That is richer than the US Communications industry at 31.6x, peers at 31.4x, and even the 38.9x fair ratio our model points to. Is the market already paying upfront for a lot of that AI growth story?

Build Your Own Arista Networks Narrative

If you look at these numbers and reach a different conclusion, or simply want to test your own assumptions, you can build a full narrative for yourself in just a few minutes, starting with Do it your way.

A great starting point for your Arista Networks research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Arista has sharpened your thinking, do not stop here. Broadening your watchlist with targeted screeners can surface opportunities you might otherwise miss entirely.

- Spot potential value plays early by scanning these 886 undervalued stocks based on cash flows that look attractively priced against their cash flow profiles and core fundamentals.

- Explore the AI buildout theme more broadly by checking these 24 AI penny stocks that line up with your conviction on data, compute and automation trends.

- Identify dependable income ideas by filtering for these 13 dividend stocks with yields > 3% that may help balance out higher growth names in your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.