A Look At Arthur J. Gallagher (AJG) Valuation As Earnings Growth Meets Profit Pressure And Deal Integration Questions

Arthur J. Gallagher & Co. AJG | 219.91 219.91 | -1.16% 0.00% Pre |

Fourth quarter earnings and dividend move draw investor focus

Arthur J. Gallagher (AJG) is back in the spotlight after fourth quarter 2025 earnings showed higher revenue alongside lower quarterly net income and diluted EPS, paired with a fresh increase to its quarterly dividend.

At a share price of $241.58, Arthur J. Gallagher has seen a 1 month share price return of an 8.70% decline and a 1 year total shareholder return of a 24.40% decline. The 3 and 5 year total shareholder returns of 27.35% and 118.35% suggest longer term momentum has been stronger than the recent pullback.

If this earnings reaction has you rethinking where growth might come from next, it could be worth scanning our list of 22 top founder-led companies as potential new ideas beyond the insurance space.

With revenue at US$13.9b, full year net income of US$1.5b and the shares trading at a discount to some analyst and intrinsic estimates, you need to ask whether AJG is undervalued or if markets are already pricing in future growth.

Most Popular Narrative: 50.3% Undervalued

Compared to Arthur J. Gallagher's last close at $241.58, the most followed narrative fair value of $485.74 implies a large valuation gap that turns attention to what is driving such a difference.

Arthur J. Gallagher & Co. (AJG) has been on an acquisition spree, with significant purchases including AssuredPartners, AnotherDay, Buck, and several others. These strategic moves are set to enhance Gallagher's market position and drive substantial growth in the coming year. AssuredPartners Acquisition: A Game Changer. The acquisition of AssuredPartners, valued at $13.45 billion, is one of the largest in Gallagher's history. This deal is expected to expand Gallagher's reach in the U.S. middle-market property/casualty and employee benefits space. Analysts project that this acquisition could lead to substantial revenue synergies, potentially exceeding initial estimates.

Curious what kind of revenue lift and margin profile would justify almost doubling the current share price? The narrative leans on acquisition driven growth, richer profitability, and a future earnings multiple that usually sits with higher growth sectors. Want to see how those moving parts combine into a $485.74 fair value for an insurance broker?

Result: Fair Value of $485.74 (UNDERVALUED)

However, this hinges on smooth deal integration and funding. Any hiccups around the AssuredPartners acquisition or share issuance could potentially undercut that undervalued thesis.

Another view on valuation

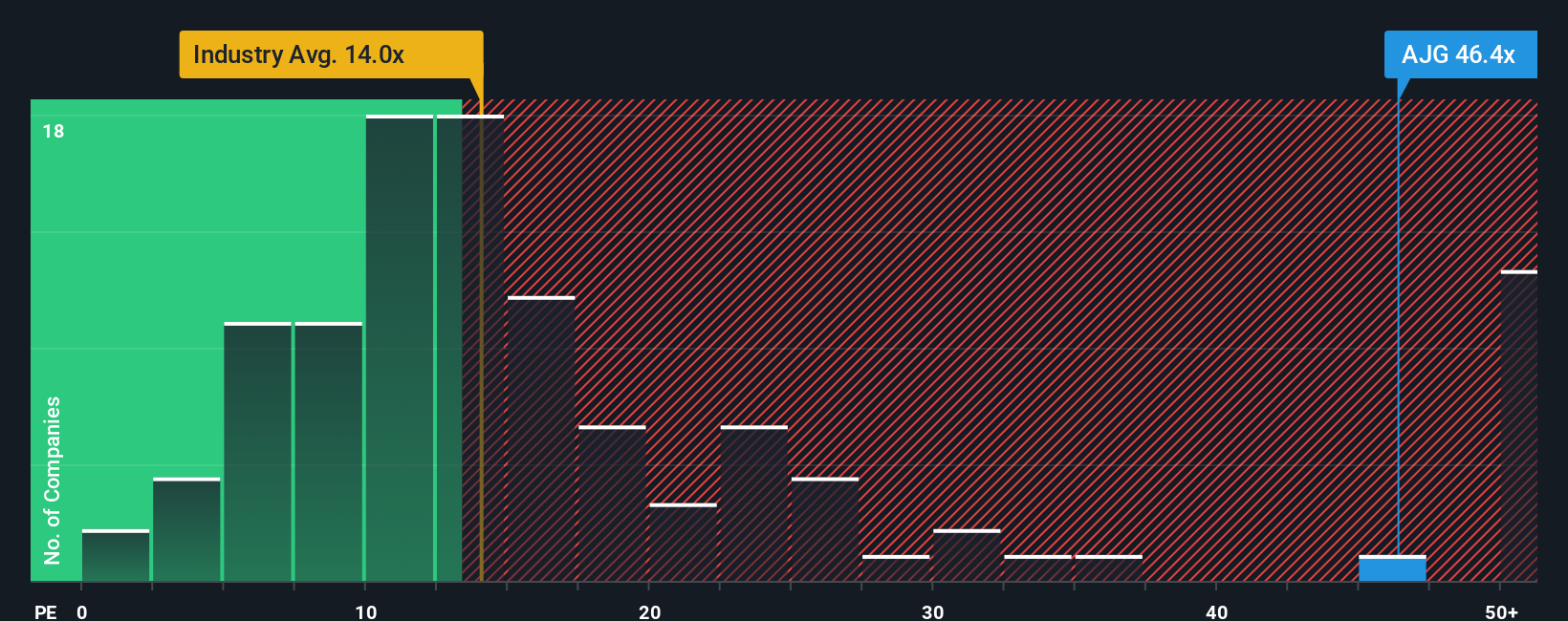

That $485.74 user fair value points to a big upside story, but the market is sending a different signal through the P/E. At $241.58, AJG trades on 41.6x earnings, far above the US Insurance industry at 13x, peers at 21.1x, and a fair ratio estimate of 19.8x.

In plain terms, the share price already reflects a lot of optimism. Any slip in execution or integration could therefore hit a highly valued stock harder than one closer to the fair ratio. The real question for you is which signal you trust more: the narrative fair value or the rich earnings multiple?

Build Your Own Arthur J. Gallagher Narrative

If you look at the numbers and reach a different conclusion, or simply want to test your own assumptions, you can build a custom thesis in just a few minutes, starting with Do it your way.

A great starting point for your Arthur J. Gallagher research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are weighing up what to do next after looking at Arthur J. Gallagher, it makes sense to widen your field of vision with a few focused stock lists.

- Target potential mispricing by scanning our list of 52 high quality undervalued stocks, built to highlight companies where the fundamentals may not match the current share price.

- Strengthen your income stream by checking out 14 dividend fortresses, a set of companies with higher yields that could help anchor total returns.

- Prioritise resilience with 82 resilient stocks with low risk scores, which spotlights businesses that our checks suggest carry fewer red flags than many of their peers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.