A Look At Atlantic Union Bankshares (AUB) Valuation After Zacks Buy Rating Upgrade

Atlantic Union Bankshares Corporation AUB | 36.09 | +0.28% |

Zacks recently upgraded Atlantic Union Bankshares (AUB) to a Buy rating after analysts raised their earnings estimates, a shift that has drawn fresh attention to the bank’s dividend profile and recent payout decisions.

Beyond the dividend news and analyst upgrade, Atlantic Union Bankshares has seen firm positive momentum, with a 30 day share price return of 11.59% and a 90 day share price return of 27.92% from a last close of $41.78. Over longer periods, the 1 year total shareholder return of 13.61% and 5 year total shareholder return of 39.89% point to gains that investors may weigh against the bank’s current earnings outlook and valuation.

If this renewal of interest in bank stocks has you thinking more broadly about where leadership matters, it could be worth broadening your search with our 22 top founder-led companies.

With the shares at $41.78, a value score of 3, an implied 8.6% gap to the average analyst target and a modelled intrinsic discount of around 29%, the key question is whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 6% Undervalued

Atlantic Union Bankshares' fair value in the most followed narrative sits at $44.44 versus the recent $41.78 share price, setting up a modest value gap investors are watching closely.

The company's geographic expansion into fast-growing markets in North Carolina, Maryland, and Northern Virginia, supported by recent acquisitions and plans to open 10 new branches in the Research Triangle and Wilmington, positions Atlantic Union to capture increased population and economic growth in the U.S. Southeast, driving above-peer organic loan and deposit growth over the coming years and lifting revenues.

Curious what is baked into that $44.44 fair value? The narrative leans heavily on stronger revenue momentum, wider margins, and a valuation multiple that assumes meaningful earnings progress. Want to see exactly how those moving parts fit together and what kind of profit profile the narrative is building in?

Result: Fair Value of $44.44 (UNDERVALUED)

However, this hinges on regional strength and clean execution. Setbacks from Mid Atlantic economic weakness or tougher Sandy Spring integration could quickly challenge that fair value story.

Another View: Earnings Multiple Sends a Different Signal

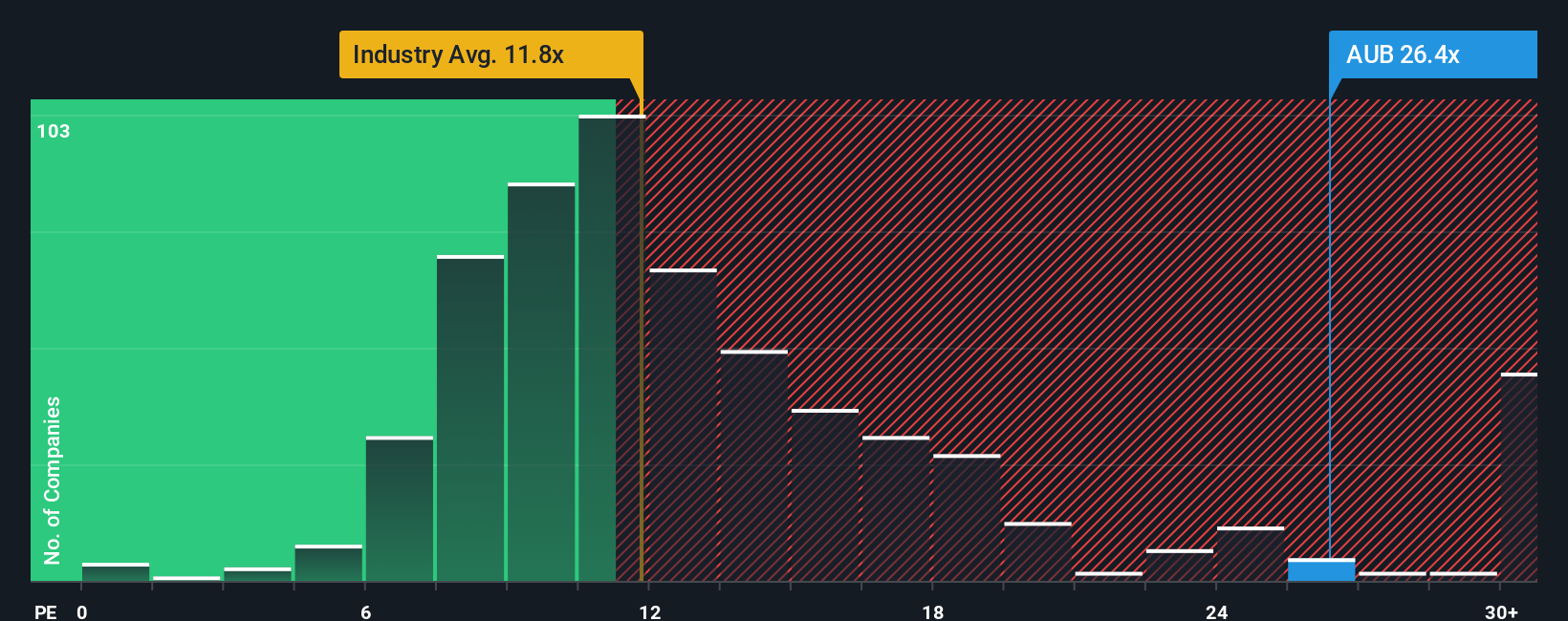

While the most followed narrative points to a modest 6% undervaluation, the current 22.6x P/E paints a more demanding picture. That level sits well above the US Banks industry at 12x and even above AUB's own fair ratio of 17.6x. This suggests less room for error if growth or profitability disappoint.

Put simply, the market is pricing AUB roughly in line with peers at 22.9x on average, but at a premium to where our fair ratio suggests the P/E could move over time. For you, that raises a simple question: is this a quality premium you are comfortable paying, or a valuation risk you would rather avoid?

Build Your Own Atlantic Union Bankshares Narrative

If you are not fully sold on these narratives, or simply prefer to test your own assumptions against the data, you can use our tools to build a complete Atlantic Union Bankshares view in just a few minutes, then shape it exactly how you want with Do it your way.

A great starting point for your Atlantic Union Bankshares research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If AUB has sharpened your thinking, do not stop here. Some of the most interesting opportunities often sit just outside the first stock on your radar.

- Spot potential value opportunities early by scanning our 52 high quality undervalued stocks that highlight companies with supportive fundamentals and room, in some cases, for sentiment to catch up.

- Steady your portfolio with income ideas using our 14 dividend fortresses focused on companies offering higher yields that investors often watch for more consistent cash returns.

- Strengthen your watchlist with companies that appear built to handle tougher conditions through our solid balance sheet and fundamentals stocks screener (45 results) that focuses on financial resilience and balance sheet quality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.