A Look At Atmus Filtration Technologies (ATMU) Valuation After Recent Share Price Weakness

Atmus Filtration Technologies, Inc. ATMU | 0.00 |

Recent trading performance and business snapshot

Atmus Filtration Technologies (ATMU) has drawn investor attention after the stock fell 2.3% in the latest session, extending declines of 6.4% over the past week and 13.2% over the past month.

Over the past 3 months, the share price is down 27.3%, even as the company reports revenue of US$1.83b and net income of US$211.1m from its filtration products and related technologies.

The recent 1-day share price decline of 2.31% extends a broader loss in momentum, with the 30-day share price return down 13.2% even as the 1-year total shareholder return stands at 26.97% and the 3-year total shareholder return at 117.72%.

If you are weighing what else to put on your radar, this could be a good moment to broaden your search and uncover 20 top founder-led companies

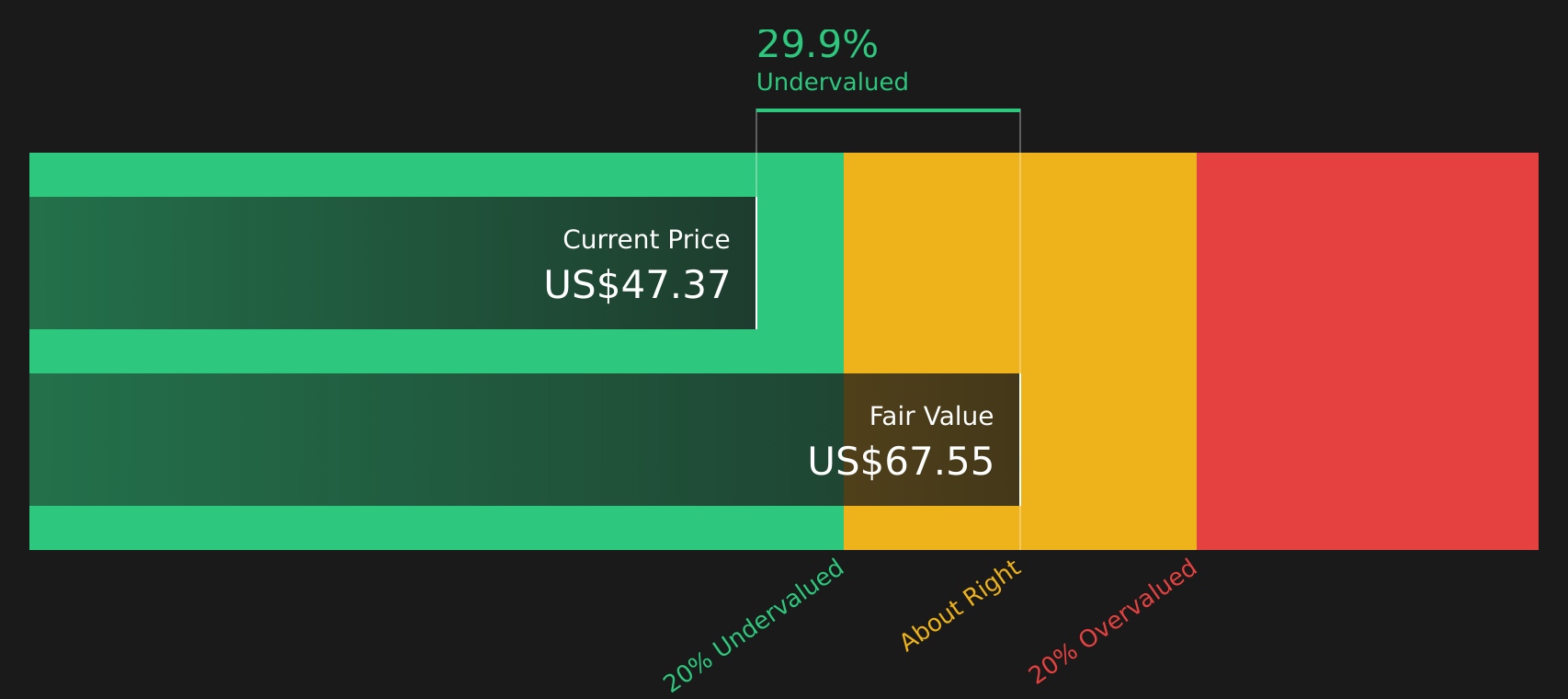

With Atmus shares down over the past quarter yet trading below analyst targets and an estimated intrinsic value, you have to ask: is this a genuine value opportunity, or is the market already pricing in future growth?

Price-to-Earnings of 17.7x: Is it justified?

On a P/E of 17.7x, Atmus Filtration Technologies looks inexpensive compared to both its own estimated fair multiple and the machinery peers it trades alongside.

The P/E ratio compares the share price to earnings per share and helps you see how much investors are willing to pay for each dollar of profit. For a business generating US$1.83b in revenue and US$211.1m in net income from filtration products and services, earnings-based metrics are a useful way to benchmark expectations.

Here, ATMU is flagged as good value in several ways. Its current P/E of 17.7x sits below an estimated fair P/E of 23.2x that our models suggest the market could move toward. It also comes in under both the peer average of 28x and the broader US Machinery industry average of 26.8x. Together with the view that the shares trade at a discount to an intrinsic value implied by future cash flows, this points to the market pricing ATMU more cautiously than those comparison points.

Result: Price-to-Earnings of 17.7x (UNDERVALUED)

However, the recent 27.3% share price decline over 3 months and reliance on cyclical commercial and off highway vehicle demand could quickly challenge any value-focused thesis.

Another view on value

While the current P/E of 17.7x suggests good value versus a fair ratio of 23.2x and a peer average of 28x, our DCF model also points to the stock trading below an estimated future cash flow value of $67.66. This reinforces the undervalued picture and raises a different question: what if the risk sits more in execution than in price?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Atmus Filtration Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed signals so far, it makes sense to look at the full picture yourself, weigh the concerns against the potential upside, and review the 5 key rewards and 1 important warning sign

Looking for more investment ideas?

If Atmus has your attention, do not stop here. Use this moment to widen your watchlist and uncover other stocks that could fit your approach.

- Target potential mispricings by scanning 47 high quality undervalued stocks that combine solid financials with attractive pricing signals.

- Build a steadier income stream by reviewing 10 dividend fortresses that focus on higher yields backed by robust metrics.

- Prioritise resilience by focusing on 62 resilient stocks with low risk scores that screen for companies with lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.