A Look At ATRenew (NYSE:RERE) Valuation After Circular Markets London Recognition

AiHuiShou International Co. Ltd. RERE | 4.42 | -5.56% |

ATRenew (RERE) drew fresh investor attention after serving as the sole Chinese representative at Circular Markets London, where it outlined how its pre-owned electronics platform links China’s large device supply with global circular value chains.

ATRenew’s recent role at Circular Markets London comes as the stock trades at US$6.06, with a 44.29% 90 day share price return and a 98.04% 1 year total shareholder return. This suggests momentum has been building over the past year despite short term swings.

If this circular economy story has you thinking about where else growth could emerge, now may be a time to look at 58 profitable AI stocks that aren't just burning cash as potential next ideas to research.

With ATRenew trading at US$6.06 and sitting at a 16% discount to its analyst price target and a 14% intrinsic discount, you have to ask: is there still value on the table, or is future growth already priced in?

Most Popular Narrative: 8.3% Undervalued

At $6.06, ATRenew sits slightly below the most followed fair value estimate of $6.61, which is built on detailed revenue and earnings projections.

The continued integration of government-backed trade-in subsidies and eco-friendly consumption policies is associated with accelerating consumer adoption of device recycling and recommerce in China, presenting a structural long-term tailwind for transaction volume and revenue.

Rising consumer preference for sustainable consumption and the normalization of secondhand trading, particularly among younger demographics, are expanding ATRenew's addressable market and are viewed as potential drivers of sustained increases in user acquisition and recurring revenue.

Want to see what kind of revenue changes and margin shifts would need to occur for that fair value to hold up? The full narrative lays out the assumptions around growth and the profit profile that underpin this 8.3% gap.

Result: Fair Value of $6.61 (UNDERVALUED)

However, there are still pressure points to watch, including reliance on Chinese subsidies and thin margins that could quickly feel the impact of higher costs or weaker demand.

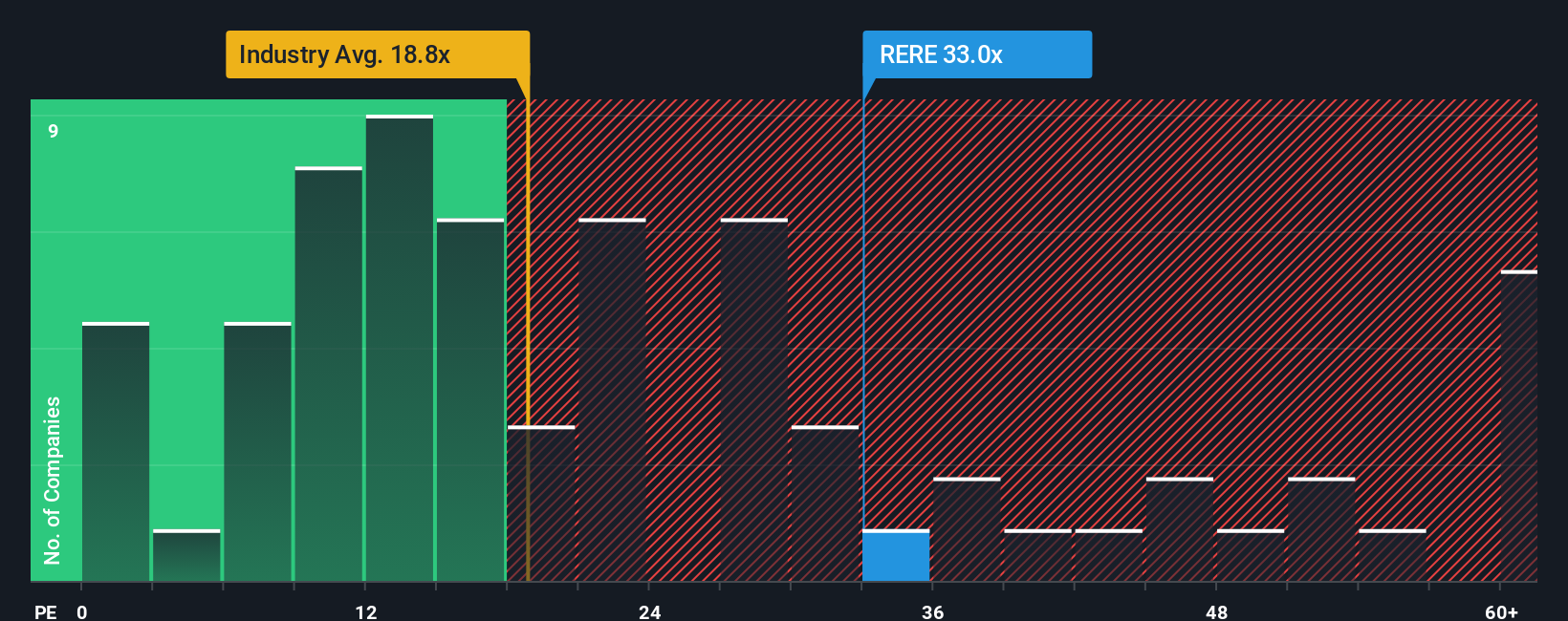

Another View: P/E Tells A Different Story

Our DCF work suggests ATRenew is trading below estimated cash flow value, but the P/E ratio paints a different picture. At 33x earnings compared to 20.7x for the US Specialty Retail industry and 16.2x for peers, the stock screens as expensive.

The estimated fair ratio of 40x is higher than today, which implies the market could still re-rate either way. For you, that raises a simple question: is this a quality premium you are comfortable paying, or a valuation gap that could close the other way?

Build Your Own ATRenew Narrative

If you look at the numbers and come to a different conclusion, or simply prefer your own framework, you can build a custom view in minutes. Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding ATRenew.

Looking for more investment ideas?

If ATRenew has you thinking more broadly about opportunities, do not stop here. There are other stocks with different risk and income profiles worth a closer look.

- Target steadier compounding by checking out 83 resilient stocks with low risk scores, where companies score well on resilience and tend to have fewer red flags on core fundamentals.

- Pursue value opportunities with screener containing 24 high quality undiscovered gems, a curated group of lesser known businesses that our models flag for strong quality metrics.

- Strengthen the income side of your portfolio by reviewing 14 dividend fortresses, focused on companies offering higher yields supported by their financial profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.