A Look At Babcock & Wilcox Enterprises (BW) Valuation After New Class Action Lawsuits Over Contract Disclosures

Babcock & Wilcox Enterprises Inc BW | 0.00 |

Multiple law firms have launched class action lawsuits against Babcock & Wilcox Enterprises (BW), focusing on allegations of misleading disclosures around a major power generation contract and related conflicts of interest.

Despite the class action headlines, the stock is still up strongly on a longer view, with a 157.64% year to date share price return and a very large 1 year total shareholder return. However, the 1 day share price return fell 12.23% as investors reassessed contract and legal risks.

If this legal saga has you comparing risk and opportunity across the energy space, it could be worth scanning 88 nuclear energy infrastructure stocks for other power and infrastructure stocks that fit your thesis.

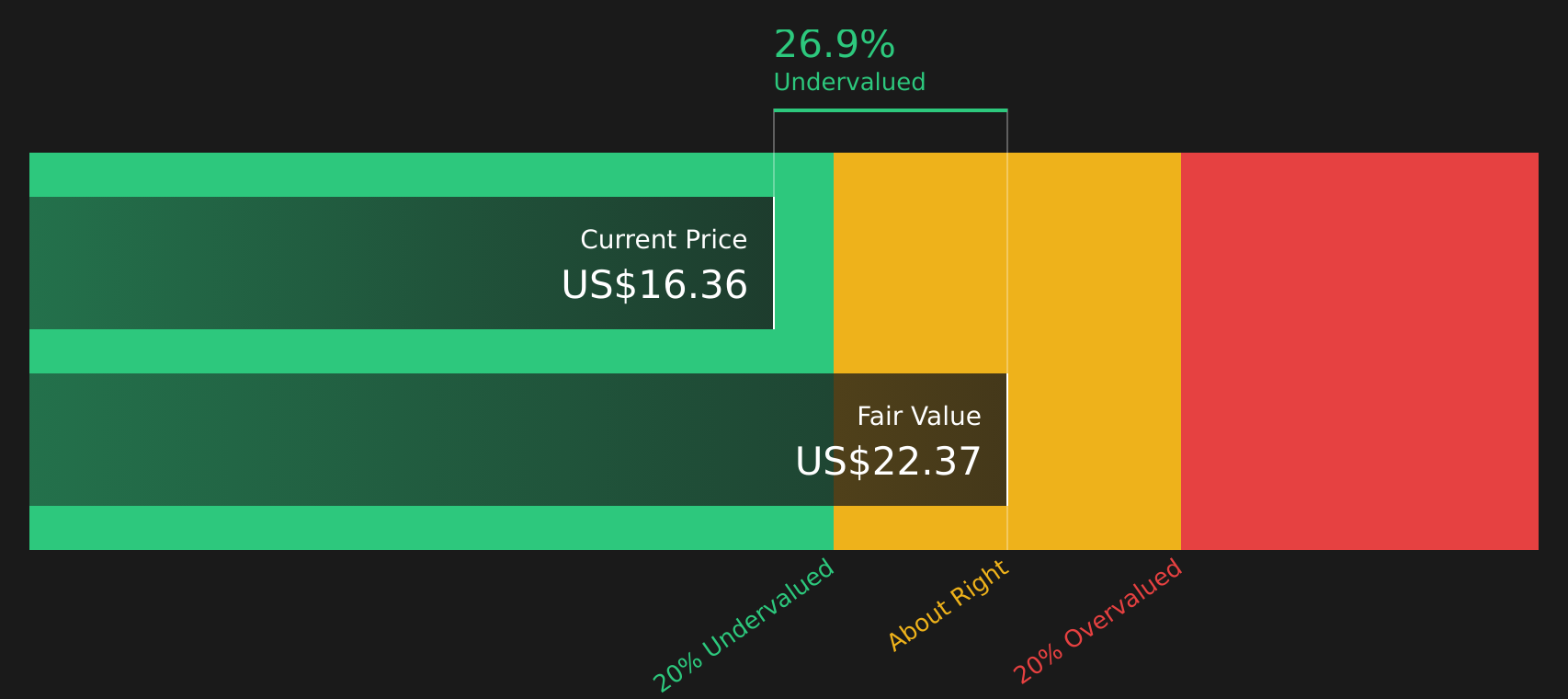

With the stock still showing a very large 1 year total shareholder return and trading at a 26.7% discount to one intrinsic value estimate, as well as around 49% below an analyst price target, investors have to ask whether this is a potential entry point or whether the market is already pricing in future growth.

Most Popular Narrative: 96.3% Overvalued

The most followed narrative sees fair value for Babcock & Wilcox Enterprises at $8.33, well below the last close at $16.36, and builds a case around long term earnings potential priced at a high future multiple.

The analysts have a consensus price target of $8.33 for Babcock & Wilcox Enterprises based on their expectations of its future earnings growth, profit margins and other risk factors. In order for you to agree with the analysts, you would need to believe that by 2029, revenues will be $769.0 million, earnings will come to $21.2 million, and it would be trading on a PE ratio of 72.8x, assuming you use a discount rate of 10.9%.

Curious what kind of revenue path, margin rebuild and share count assumptions sit behind that high earnings multiple and fair value gap? The full narrative lays out the detailed growth, profitability and dilution blueprint that underpins this valuation story.

Result: Fair Value of $8.33 (OVERVALUED)

However, this relies on demand for AI data centers and the successful execution of large projects. Any slowdown, delay or cost overrun could quickly challenge the optimistic scenario.

Another View: Cash Flows Point a Different Way

Analysts using earnings and a P/E style framework see Babcock & Wilcox Enterprises as about 96.3% above their $8.33 fair value. Yet our DCF model, which focuses on future cash flows rather than earnings multiples, suggests the stock at $16.36 sits below an estimated value of $22.31. That split raises a simple question for you: are earnings targets or cash flow assumptions the bigger swing factor here?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Babcock & Wilcox Enterprises for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between legal risks and potential upside, it makes sense to check the numbers yourself rather than wait for consensus views, then weigh up the 3 key rewards and 3 important warning signs

Looking for more investment ideas?

If this situation has sharpened your focus, now is a good time to broaden your watchlist and compare other stocks that might better match your risk and return goals.

- Spot potential bargains early by scanning screener containing 22 high quality undiscovered gems that pair solid fundamentals with relatively low market attention.

- Prioritize resilience by reviewing 64 resilient stocks with low risk scores that score well on stability and downside protection.

- Target quality at a sensible price by checking 49 high quality undervalued stocks that combine stronger financials with discounted valuations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.