A Look At BGC Group (BGC) Valuation After New FCA Benchmark Administrator Approval

BGC Group, Inc. Class A BGC | 9.98 | +1.42% |

BGC Group (BGC) shares are in focus after the company reported that BGC Brokers L.P. is now authorized as a U.K. registered benchmark administrator with the Financial Conduct Authority under U.K. Benchmarks Regulation.

The FCA benchmark approval comes as BGC Group’s 1-month share price return of 3.36% and year to date share price return of 3.36% contrast with a 1-year total shareholder return decline of 2.61%, while the 3-year and 5-year total shareholder returns, at over 2x, point to longer term investors still seeing value in the story.

If this kind of regulatory progress has your attention, it could be a good moment to see what else is on the move and check out fast growing stocks with high insider ownership.

With the shares up 3.4% over the past month but the 1 year return still slightly negative, is BGC Group quietly trading below what its fundamentals and new FCA benchmark license might justify, or is the market already pricing in future growth?

Most Popular Narrative: 36.3% Undervalued

Compared to BGC Group's last close at $9.24, the most followed narrative points to a fair value of $14.50, setting up a wide gap in expectations.

Continued expansion and strong revenue growth from BGC's electronic trading platforms (notably Fenics and FMX), supported by substantial increases in electronic volumes and market share across asset classes, suggest that BGC is positioned to capitalize on the accelerating shift toward technology-driven trading. This is likely to boost top-line revenue and expand margins due to the higher scalability and profitability of electronic versus voice-driven trading.

Curious what kind of revenue growth, margin expansion and earnings profile have to line up to support that $14.50 fair value on a 9.18% discount rate? The full narrative breaks down how electronic platforms, higher margin services and future profitability assumptions all feed into that price target and why the current share price sits well below it.

Result: Fair Value of $14.50 (UNDERVALUED)

However, this depends on volatile trading conditions and the successful integration of recent acquisitions, and setbacks in either area could quickly challenge that 36.3% undervalued story.

Another Angle on Valuation

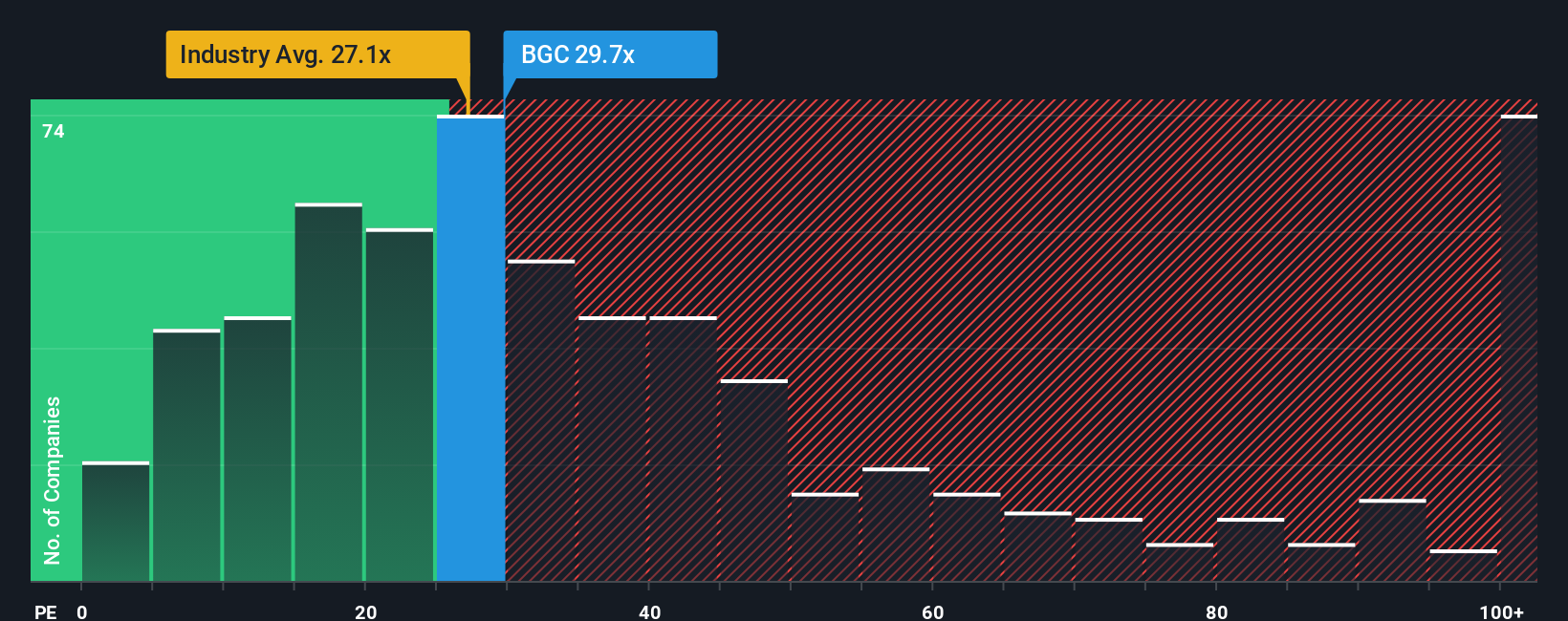

The popular $14.50 fair value story leans on future earnings and margins, but today the market is charging a P/E of 27.2x for BGC Group, compared with 23.6x for the US Capital Markets industry and 9.2x for peers. That richer multiple raises a simple question: is this a rerating in progress or a lot of optimism already baked in?

Build Your Own BGC Group Narrative

If you look at the numbers and come to a different conclusion, or simply prefer running your own checks, you can build a custom BGC story in just a few minutes with Do it your way.

A great starting point for your BGC Group research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If BGC Group is on your radar, do not stop there. Widen your watchlist with a few focused idea sets that could help inform your next move.

- Spot potential high risk high reward opportunities early by scanning these 3542 penny stocks with strong financials that already show stronger financial foundations than many peers.

- Target the intersection of computing power and returns with these 22 quantum computing stocks, where companies are working on the next wave of quantum technology.

- Strengthen your income focus by checking these 13 dividend stocks with yields > 3% that offer yields above 3% and may suit a dividend oriented approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.