A Look At Birkenstock (BIRK) Valuation After Revenue Growth Target Cut And Share Price Pullback

Birkenstock Holding Ltd. BIRK | 0.00 |

Birkenstock Holding (BIRK) is back in focus after management cut its fiscal 2026 revenue growth target to a range of 13% to 15%, a guidance reset that coincided with a pullback in the stock.

The revised outlook has come alongside weaker short term share price momentum, with a 7 day share price return of 11.48% and a 30 day share price return of 17.09%. This has contributed to a 1 year total shareholder return of 35.81%, which suggests sentiment has cooled after earlier enthusiasm.

If Birkenstock’s reset has you rethinking growth stories in consumer names, it may be a good time to widen your search and check out fast growing stocks with high insider ownership.

With the share price down over the past year despite double digit revenue and net income growth, and the stock trading at what some see as a conservative valuation, the key question is whether this pullback is a chance to buy, or if the market already reflects Birkenstock’s future growth.

Price to Earnings of 17.5x: Is it justified?

At a last close of US$38.47, Birkenstock Holding trades on a P/E of 17.5x, which current data suggests is lower than several key benchmarks.

P/E compares the share price with earnings per share, so a lower multiple can indicate the market is assigning a more conservative value to each unit of profit. For a profitable consumer brand with positive earnings growth forecasts, that comparison is often a key reference point.

Here, Birkenstock is described as trading at good value relative to peers and the wider luxury industry. Its 17.5x P/E is below the US Luxury industry average of 20.6x and well below a peer average of 37.7x. It is also judged attractive when set against an estimated fair P/E of 18.6x, a level the market could potentially move toward if sentiment and earnings expectations align with that fair ratio view.

Result: Price-to-Earnings of 17.5x (UNDERVALUED)

However, the reset to 13% to 15% revenue growth and recent share price weakness highlight execution risk and the possibility that expectations for consumer demand are too optimistic.

Another View: What Does The DCF Say?

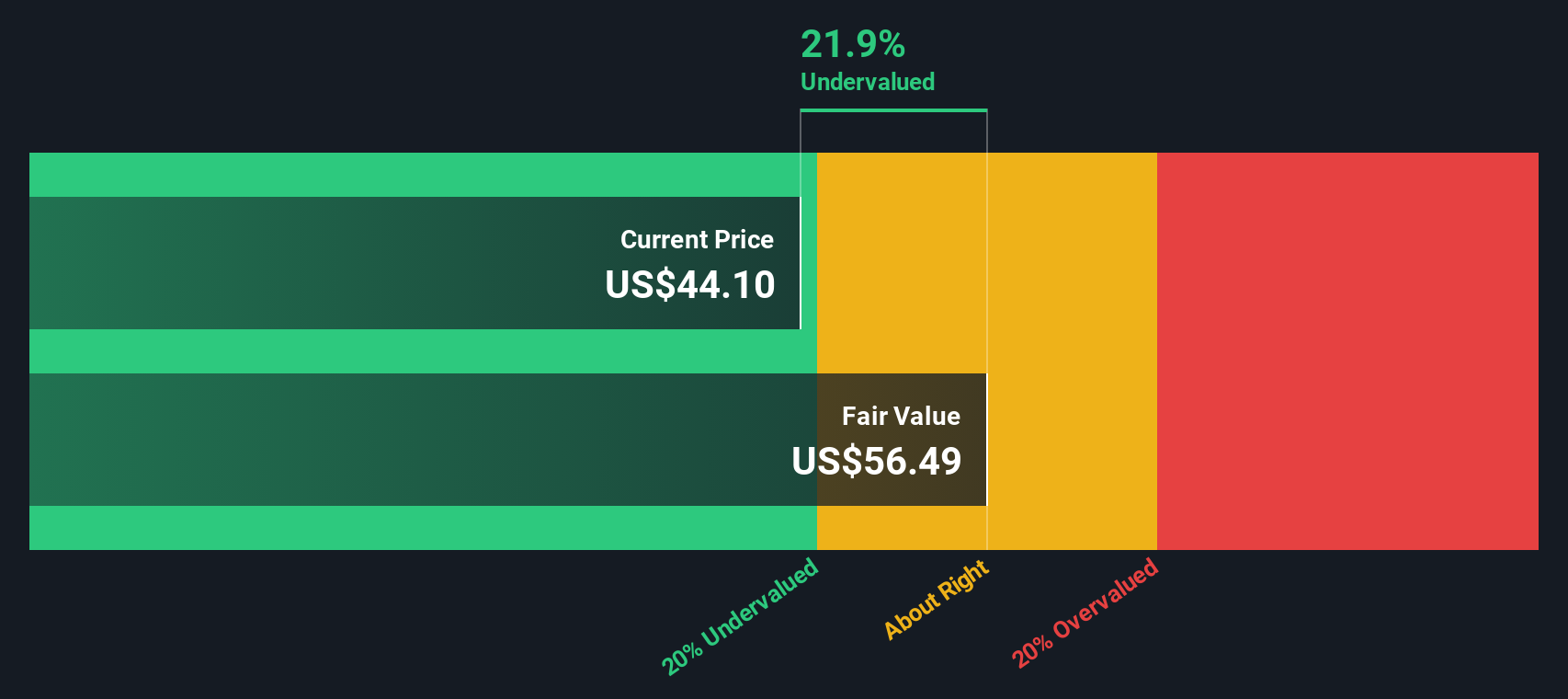

While the 17.5x P/E points to Birkenstock Holding trading at what is described as good value, our DCF model provides additional context. With an estimated fair value of US$56.09 per share versus a market price of US$38.47, it indicates the stock is undervalued by 31.4%.

This gap suggests the market may be placing a cautious price on Birkenstock’s future cash flows despite forecasts for 10.7% annual revenue growth and 14.14% annual earnings growth. The question for you is whether that caution is a useful warning or an opening.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Birkenstock Holding for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 863 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Birkenstock Holding Narrative

If you see the numbers differently or prefer to test your own assumptions, you can quickly build a custom Birkenstock story in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding Birkenstock Holding.

Looking for more investment ideas?

If Birkenstock is on your radar, do not stop there. Broaden your watchlist with other angles the market might be overlooking using the Simply Wall Street Screener.

- Spot potential bargains by checking out these 863 undervalued stocks based on cash flows that current market prices may not fully reflect.

- Zero in on income opportunities through these 12 dividend stocks with yields > 3% that might fit a yield focused approach.

- Tap into fast changing themes with these 80 cryptocurrency and blockchain stocks that are tied to blockchain and digital asset trends.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.