A Look At Black Hills (BKH) Valuation After Earnings Growth And Reinforced Analyst Optimism

Black Hills Corporation BKH | 76.60 | +6.14% |

Black Hills (BKH) is back in focus after reporting fourth quarter and full year 2025 earnings, with higher sales and net income, alongside a reaffirmed favorable analyst outlook that has supported recent stock interest.

The recent 6.3% year to date share price return, alongside a 29.7% total shareholder return over the past year, suggests positive momentum as investors respond to the earnings update and reaffirmed positive analyst views.

If Black Hills' move has you thinking about where else capital could work hard in essential infrastructure, it may be worth scanning our list of 25 power grid technology and infrastructure stocks for potential next ideas to research.

With the stock at $74.05 and the average analyst price target at $80.50, along with recent earnings strength, should you view Black Hills as trading at a discount, or is the market already pricing in future growth?

Most Popular Narrative: 8% Undervalued

Black Hills' most followed narrative places fair value at $80.50, a touch above the current $74.05 share price, framing the recent earnings strength in a slightly discounted light.

Large-scale capital investments such as the Ready Wyoming transmission expansion, Lange II natural gas generation, and Colorado Clean Energy Plan renewables projects are expected to materially expand Black Hills' regulated rate base, enabling predictable, above-sector-average long-term earnings and net margins through constructive rate recovery mechanisms and innovative tariffs.

Curious what sits behind that higher fair value? The narrative leans heavily on projected earnings growth, revenue expansion, and a richer future earnings multiple. The precise mix of growth, margins, and discount rate assumptions is where the story really gets interesting.

Result: Fair Value of $80.50 (UNDERVALUED)

However, this story can change quickly if large data center or blockchain customers scale back plans, or if big projects face regulatory delays and cost pressure.

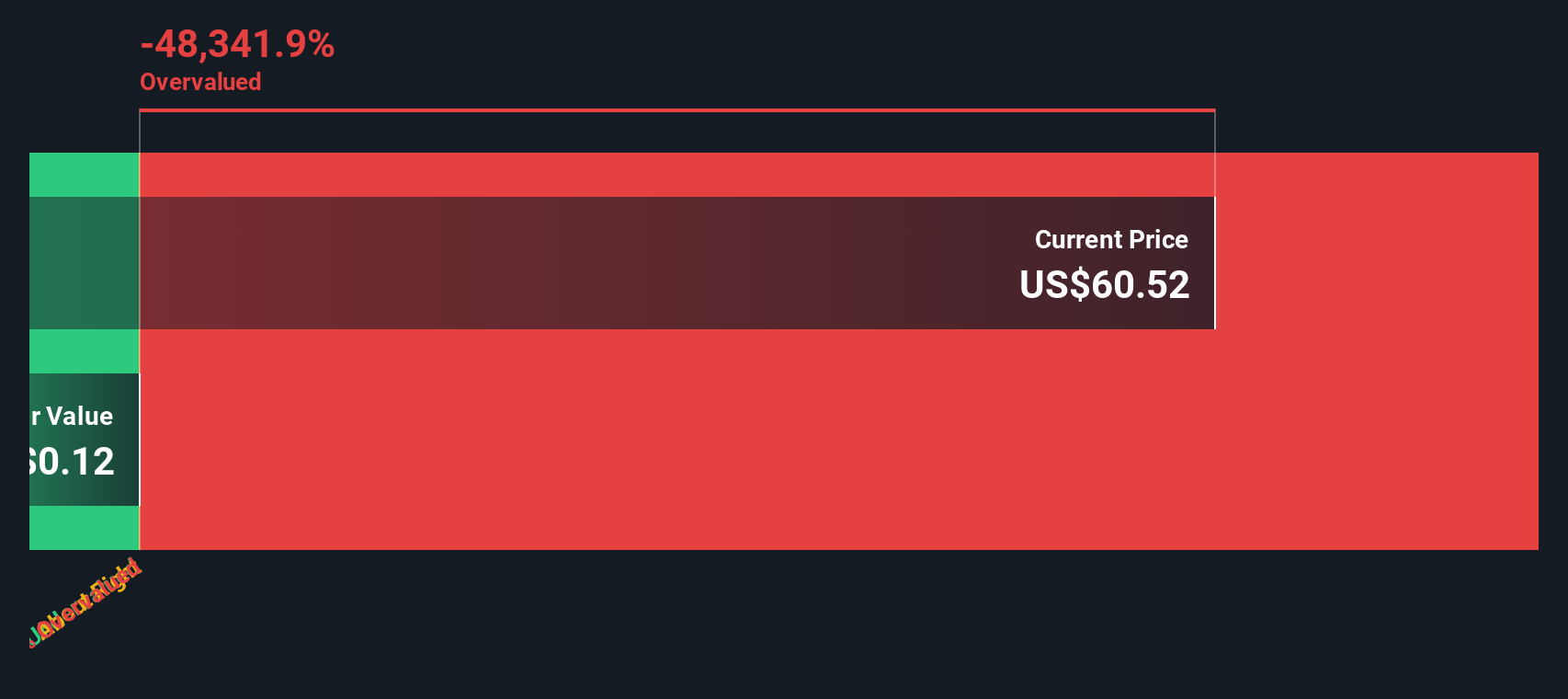

Another View: Cash Flows Paint A Tighter Picture

While the most followed narrative puts fair value at $80.50, our DCF model comes out a bit more cautious, at $71.66. The current $74.05 share price sits slightly above that. On this view Black Hills screens as modestly overvalued, so which story do you lean toward?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Black Hills for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Black Hills Narrative

If you see the numbers differently or prefer to test your own assumptions, you can pull the data together and Do it your way in just a few minutes.

A great starting point for your Black Hills research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Black Hills has caught your attention, do not stop there, broaden your watchlist with other stocks that match different goals, income needs, and risk comfort.

- Target long term value potential by checking out our 53 high quality undervalued stocks that combine solid fundamentals with attractive pricing signals.

- Strengthen your income focus by reviewing our 13 dividend fortresses that could help you build a more reliable cash return profile.

- Stay on the front foot with capital preservation by scanning our 85 resilient stocks with low risk scores aimed at businesses with more resilient risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.