A Look At Boost Run (BRUN) Valuation After US$471.7 Million GPU Contract Announcement

Boost Run Inc. Class A BRUN | 0.00 |

Why the new GPU contract matters for Boost Run (BRUN)

The recent surge in interest around Boost Run (BRUN) centers on its new approximately US$471.7 million, three year GPU server rental and managed services agreement with Thinking Machines Lab, which commits the customer to multi year payments.

The contract covers 5,000 NVIDIA B300 GPUs deployed across Boost Run data centers, along with shared storage and CPU services, and adds a sizeable, time bound stream of contracted revenue to the company’s AI infrastructure business.

Since completing its SPAC merger in May and reporting rapid revenue growth from GPU leasing and enterprise AI contracts, Boost Run’s share price return has been strong. The 30 day share price return is 105.37% and the year to date share price return is 185.47%, while the 1 year total shareholder return of 261.61% points to powerful momentum behind the recent US$471.7 million contract news, despite a 1 day share price decline of 6.28% to US$36.74.

If you want to see what else is moving in AI infrastructure, it could be worth scanning a wider peer set through our 48 AI infrastructure stocks

With BRUN up 185.47% year to date and trading above one analyst price target of US$27.50, the key question is whether this recent GPU deal still leaves upside on the table or if the market is already pricing in future growth.

Price to book of 292.9x, is it justified?

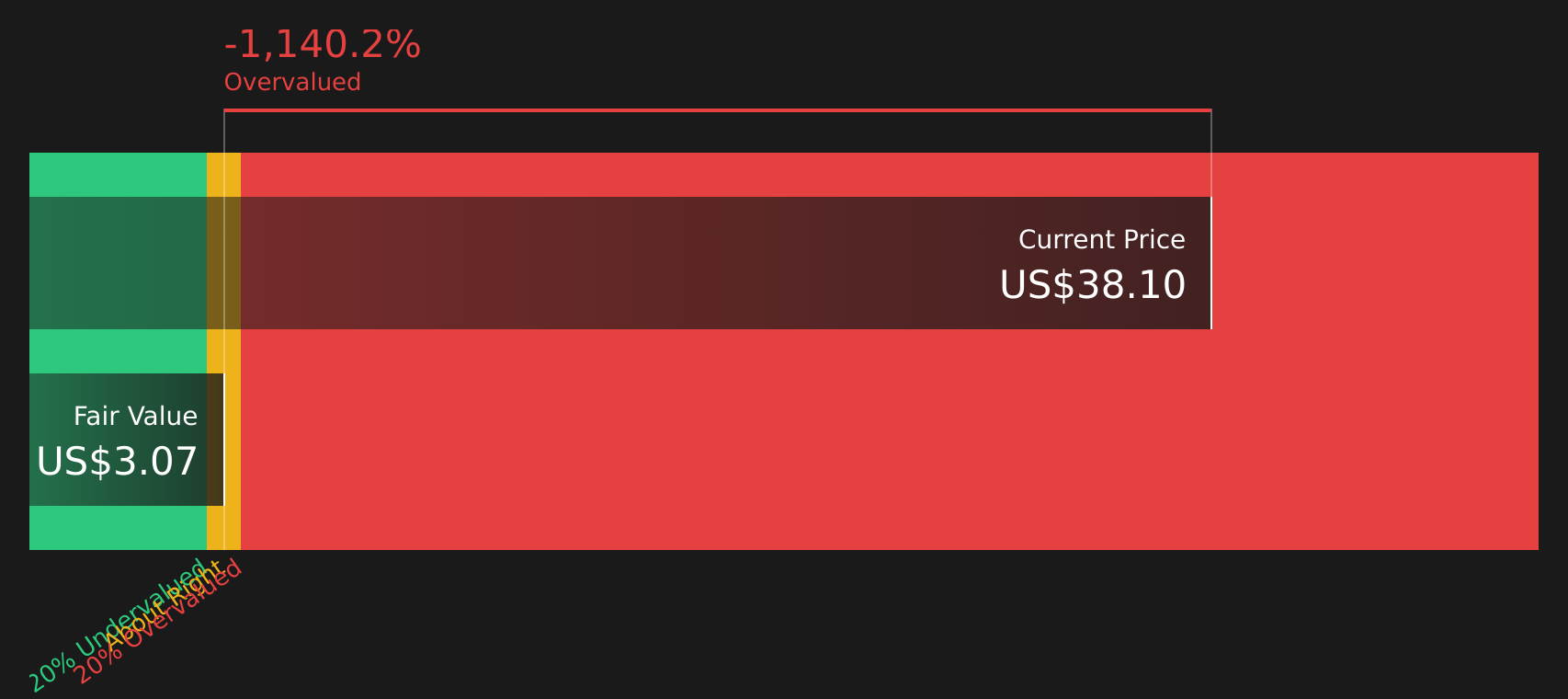

On simple P/B math, BRUN screens as very expensive, with a 292.9x multiple versus a peer average of 6.6x and a US IT sector average of 2.8x, even as the last close sits at $36.74 and above both the US$27.50 analyst target and the SWS DCF estimate of $3.04.

P/B compares the market value of a company to its accounting net assets, which can be a rough gauge of how much investors are willing to pay over the balance sheet for future cash flows. For a young, unprofitable AI infrastructure company like Boost Run, a high P/B usually reflects expectations around future revenue growth, progress toward profitability and the value investors place on scarce GPU capacity.

Here, the gap is wide. The 292.9x P/B stands far above the 6.6x peer average and the 2.8x broader US IT sector, while the SWS DCF model indicates a fair value of $3.04, materially below the current share price of $36.74. That combination suggests the market is assigning a very rich premium to BRUN relative to both asset value and modeled future cash flows.

Result: Price to book ratio of 292.9x (OVERVALUED)

However, investors also need to watch for contract concentration risk with Thinking Machines Lab and the ongoing loss of US$16.274 million, which could pressure sentiment.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another way to look at value

While the 292.9x P/B ratio makes Boost Run look very expensive relative to peers, the SWS DCF model points in the same direction, with an estimated fair value of $3.04 compared with the current $36.74 share price, which implies a very rich premium. The key issue is whether future execution can support that gap.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Boost Run for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing this mix of strong share price momentum, rich valuation and both risks and rewards, how does it stack up for you today? Take a closer look at the details, weigh the upside against the concerns, and then check out the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

Do not stop your research with just one fast moving stock. Broaden your watchlist with other clear ideas that suit your goals and risk comfort.

- Start with companies that combine quality and a potential discount by scanning our 46 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks in the 11 dividend fortresses.

- Sleep a little easier by focusing on companies flagged in the 63 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.