A Look At Bright Horizons (BFAM) Valuation As Investors Await The Next Earnings Report

Bright Horizons Family Solutions, Inc. BFAM | 83.81 | +3.18% |

Investors are watching Bright Horizons Family Solutions (BFAM) ahead of Thursday afternoon’s earnings, after the child care provider exceeded analyst expectations on revenue and adjusted earnings last quarter. The company enters this release with forecasts for slower, but still solid, year-on-year growth.

At a share price of $85.04, Bright Horizons has seen a 17.0% 1 month share price return decline and a 14.4% year to date share price return decline. The 1 year total shareholder return of 27.3% and 5 year total shareholder return of 53.2% show that longer term holders have faced meaningful pressure, hinting that expectations around growth and risk have been reset even after the recent earnings beat.

If this earnings update has you reassessing growth stories, it could be a good moment to widen your watchlist with 23 top founder-led companies that might not yet be on your radar.

With shares down recently and trading at a sizable discount to analyst targets and some intrinsic estimates, the real question is whether Bright Horizons is quietly undervalued or if the market already reflects all the future growth you are hoping for.

Most Popular Narrative: 33.2% Undervalued

Bright Horizons Family Solutions' most followed narrative places fair value at $127.33 per share versus the last close of $85.04, framing a sizeable valuation gap that rests on specific growth and margin assumptions rather than sentiment alone.

Operating margin improvement is being realized and guided to continue due to investments in technology and enhanced center efficiencies, as well as ongoing rationalization (exiting or improving underperforming centers). Incremental enrollment in 'improver' centers, alongside digital initiatives streamlining the parent experience, should lead to operating leverage and higher net margins over time.

Want to see what kind of revenue climb and margin rebuild could justify that fair value gap? The narrative leans on specific earnings targets and a future profit multiple usually reserved for higher growth names, all built around detailed assumptions you will only see laid out inside the full story.

Result: Fair Value of $127.33 (UNDERVALUED)

However, that valuation gap depends on enrollment and occupancy improving, and on wage pressures staying manageable. Both of these factors could easily challenge the bullish narrative.

Another Angle: Multiples Paint A Tougher Picture

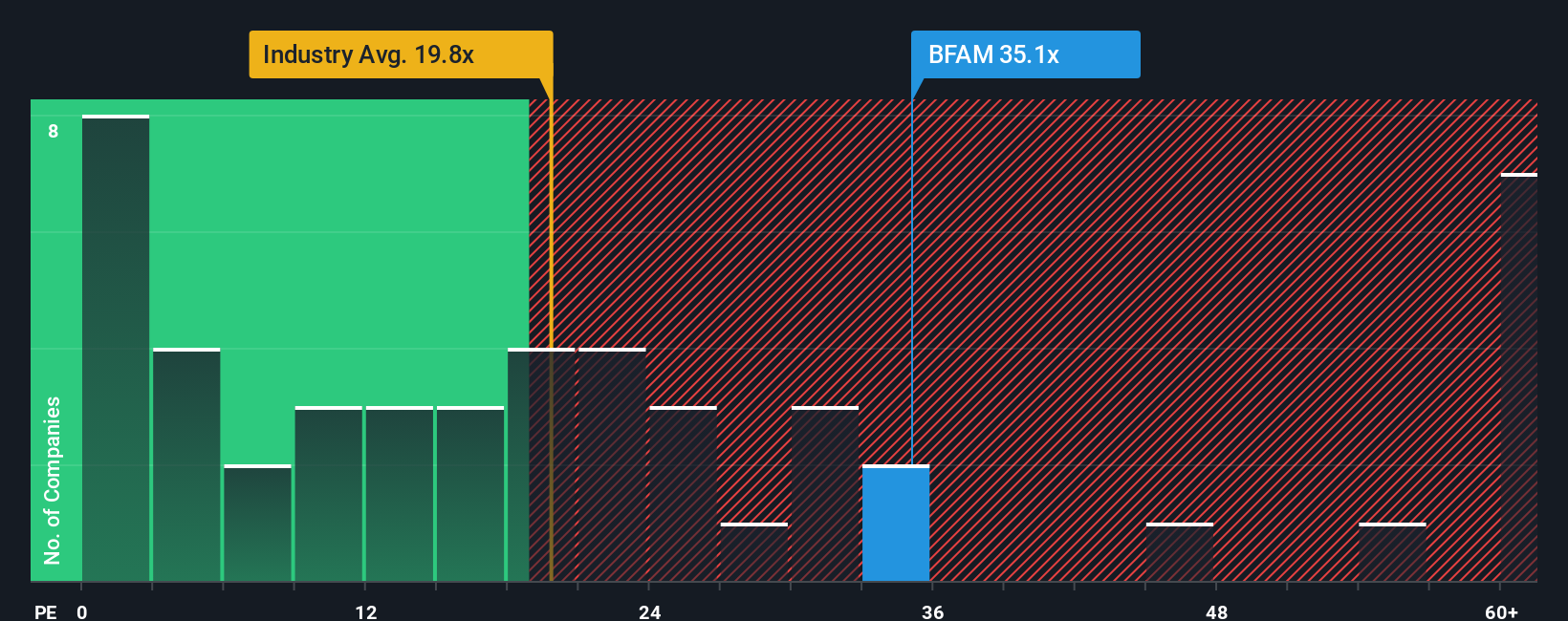

While our fair value estimate suggests Bright Horizons looks undervalued, its current P/E of 24x is higher than both the US Consumer Services industry at 16.8x and the peer average at 16.5x, and above a fair ratio of 21.6x. That richer pricing can mean less room for error if growth or margins disappoint.

For a closer look at how that P/E gap could close over time, and whether the market might move toward the fair ratio instead, See what the numbers say about this price — find out in our valuation breakdown. can help you stress test your own expectations.

Build Your Own Bright Horizons Family Solutions Narrative

If the data or assumptions here do not quite fit how you see Bright Horizons, you can review the same numbers yourself and Do it your way in just a few minutes.

A great starting point for your Bright Horizons Family Solutions research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready to hunt for your next idea?

If Bright Horizons has sharpened your thinking, do not stop here. The Simply Wall St screener can surface other opportunities that deserve a spot on your watchlist.

- Zero in on quality at a discount by checking companies our screener flags as 51 high quality undervalued stocks before the crowd pays closer attention.

- Protect your downside first and scan for 83 resilient stocks with low risk scores that aim to keep risk scores in check while still offering room for returns.

- Spot potential future leaders early by reviewing our screener containing 24 high quality undiscovered gems that combine solid fundamentals with relatively low market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.