A Look At BrightSpring Health Services (BTSG) Valuation After Bullish Analyst Actions And Strong Growth Signals

BrightSpring Health Services, Inc. BTSG | 46.01 46.01 | -0.07% 0.00% Post |

Why BrightSpring Health Services (BTSG) Is Back on Investor Screens

BrightSpring Health Services (BTSG) has jumped into focus after a mix of upbeat analyst actions, stronger quarterly results, and multi year growth in revenue and earnings per share attracted fresh investor attention.

At a share price of $39.68, BrightSpring’s recent gains include a 3.44% 1 day share price return and a 19.73% 90 day share price return, while the 1 year total shareholder return of 79.47% points to strong momentum building around the story.

If this kind of move has your attention, it could be a good moment to widen your watchlist with our screener of 26 healthcare AI stocks.

With BrightSpring trading at $39.68 against an average analyst target of about $44.47 and a higher $55 high-end target, investors may consider whether there is still an opportunity at the current price or if expectations are already fully reflected.

Most Popular Narrative: 5.4% Undervalued

At $39.68 against a narrative fair value of $41.93, BrightSpring is framed as modestly undervalued, with future cash flows and profitability assumptions doing the heavy lifting in that gap.

The analysts have a consensus price target of $28.708 for BrightSpring Health Services based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $41.0, and the most bearish reporting a price target of just $25.0.

Want to see what is sitting behind that fair value lift, despite such a wide range of price targets? The narrative leans heavily on rising margins, meaningful earnings growth and a future valuation multiple that assumes the market will reward those numbers. Curious which forecasts really move the model and how sensitive the outcome is to a few key inputs? The full story is in the detailed narrative.

Result: Fair Value of $41.93 (UNDERVALUED)

However, this hinges on access to limited distribution drugs, as well as managing labor and reimbursement pressures that could quickly test those upbeat margin assumptions.

Another Way To Look At BTSG’s Valuation

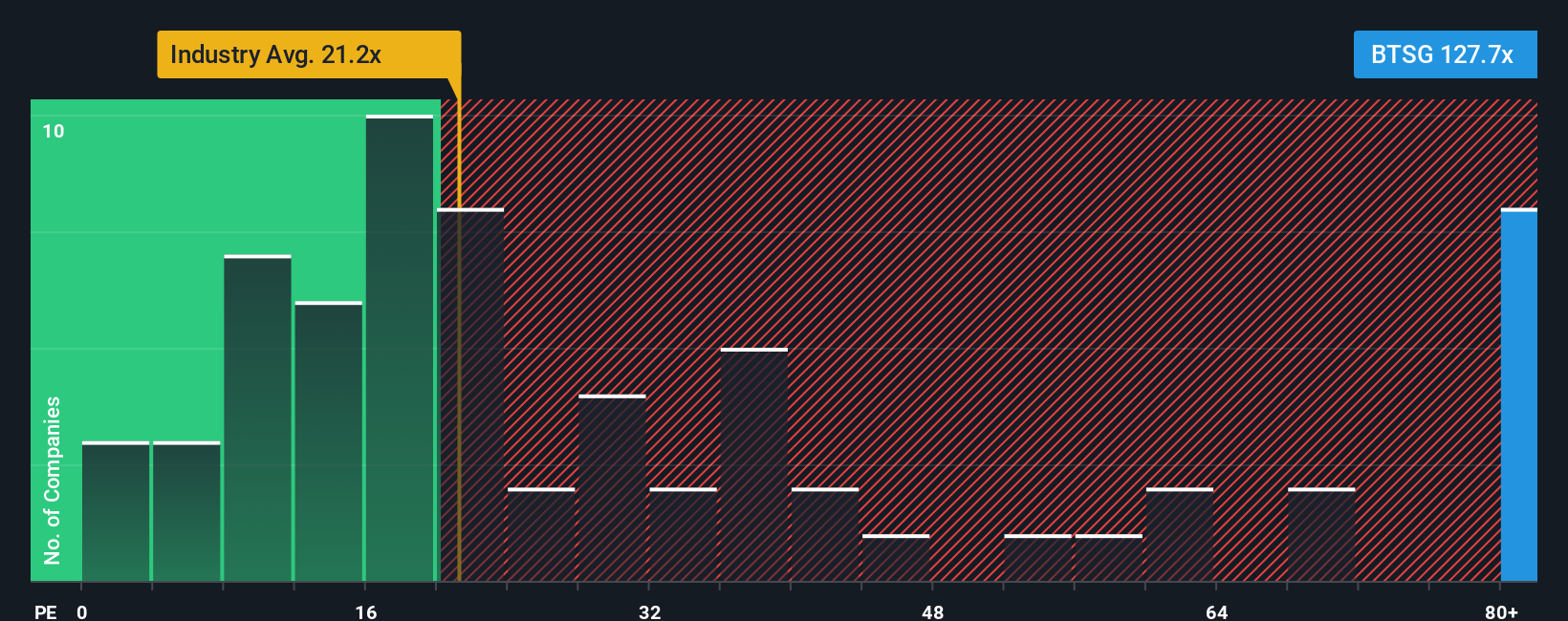

The earlier narrative suggests BrightSpring is modestly undervalued, but the P/E story pulls the other way. At about 74.3x earnings, the share price sits well above the fair ratio of 31.9x, the US Healthcare industry at 23.2x, and peers around 25.2x, which points to meaningful valuation risk if sentiment cools.

That kind of gap raises a simple question for you as an investor: are you comfortable paying a much higher P/E today on the view that future growth and margins will keep supporting it, or would you prefer to wait for the price and the fair ratio to move closer together?

Build Your Own BrightSpring Health Services Narrative

If you see the numbers differently or prefer to rely on your own checks, you can shape a complete BrightSpring story yourself in just a few minutes, starting with Do it your way.

A great starting point for your BrightSpring Health Services research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at a single company story. Broaden your search with data driven stock ideas.

- Target potential mispricings by running your own value hunt with our 53 high quality undervalued stocks that filters for quality businesses trading below their assessed worth.

- Strengthen your income stream by scanning for reliable payers using our 14 dividend fortresses focused on higher yielding companies with the potential for durable payouts.

- Prioritise resilience by zeroing in on companies flagged in our 86 resilient stocks with low risk scores designed to highlight stocks with fewer red flags on key risk checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.