A Look At Broadridge Financial Solutions (BR) Valuation After DeepSee Agentic AI Partnership Expansion

Broadridge Financial Solutions, Inc. BR | 160.93 | +0.59% |

Broadridge Financial Solutions (BR) has taken a minority stake in Utah based DeepSee, extending their partnership to bring agentic AI into post trade operations through AI powered email orchestration, which is already running across more than 60 client operations.

The DeepSee investment and growth of Broadridge’s Distributed Ledger Repo platform sit against a share price of US$223.36, with a year to date share price return of 1.31% and a 5 year total shareholder return of 60.17%, suggesting long term holders have seen stronger gains than more recent buyers.

If this kind of AI focused infrastructure story interests you, it may be worth scanning high growth tech and AI stocks to see which other names are building similar capabilities into their business models.

With the stock up only 1.3% year to date but trading at roughly a 29% discount to one intrinsic value estimate and about 21% below analyst targets, investors may be wondering whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 17.1% Undervalued

Broadridge Financial Solutions' most followed narrative puts fair value at US$269.38, above the current US$223.36 share price, framing the stock as undervalued.

The company's increasing share of SaaS and recurring subscription models, combined with consistently high client retention rates (97–98%), is associated with more predictable and resilient revenues and earnings, and is presented as positioning Broadridge for sustainable EPS growth and ongoing dividend increases.

Curious what earnings profile and profit margins are baked into that valuation gap, and how much of it leans on future pricing power and retention economics? The full narrative spells out the growth path and the profit multiple investors would effectively be paying for that story.

Result: Fair Value of $269.38 (UNDERVALUED)

However, the story also leans on event driven revenues not repeating and on longer sales cycles easing; any disappointment there could quickly challenge that 17.1% undervalued case.

Another View: Market Multiple Sends A Different Signal

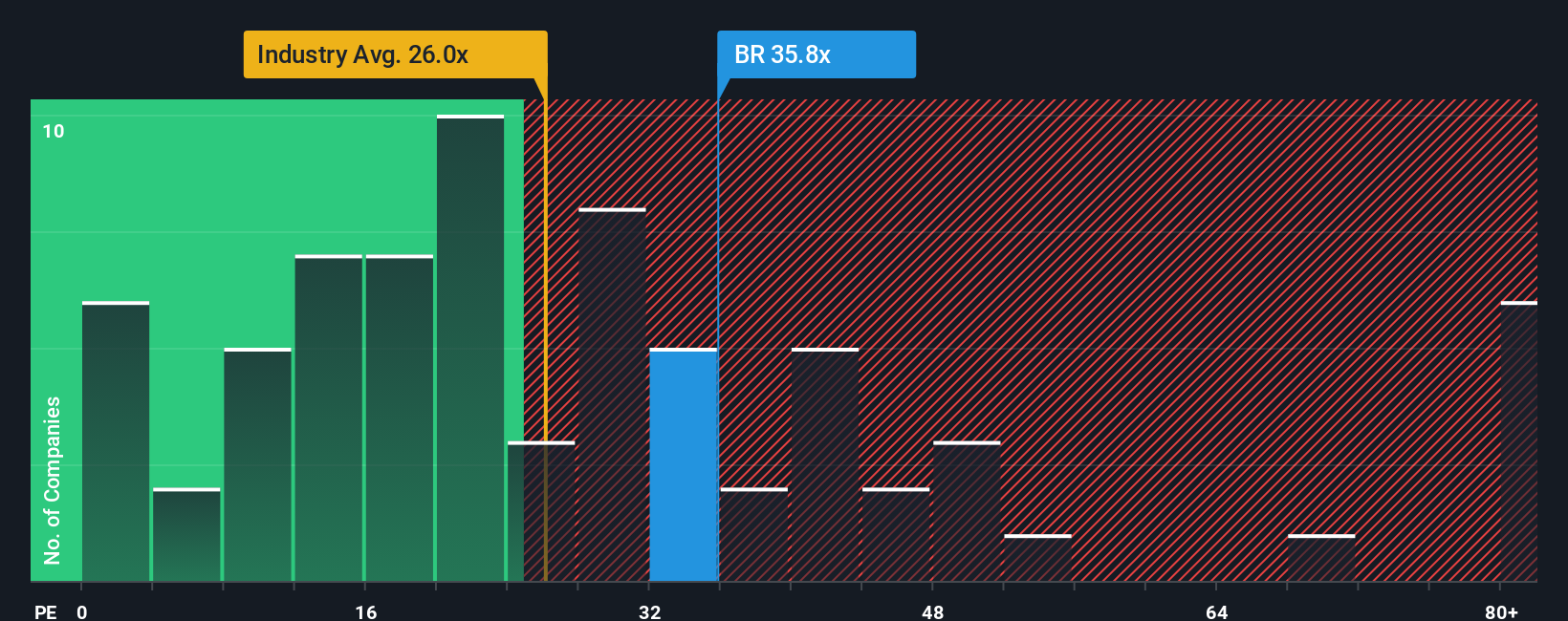

While the popular narrative frames Broadridge as 17.1% undervalued at US$269.38, the current P/E of 28.2x tells a more cautious story. It sits above the US Professional Services industry at 25.1x, the peer average at 21.1x, and even the estimated fair ratio of 26.6x.

That gap suggests the market already pays a premium for Broadridge, which could limit upside if expectations ease or growth cools. The question for you is whether the business quality and AI push justify paying more than both peers and the fair ratio, or if patience is the better call.

Build Your Own Broadridge Financial Solutions Narrative

If you look at this and think the assumptions miss the mark, or simply want to test your own data driven view, you can sketch out a complete thesis in just a few minutes, starting with Do it your way.

A great starting point for your Broadridge Financial Solutions research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Broadridge has you thinking about where to put your next dollar, it is worth lining up a few fresh ideas before the next move.

- Spot potential mispricings early by scanning these 882 undervalued stocks based on cash flows that flag companies where market prices differ from underlying cash flow metrics.

- Target future facing themes by reviewing these 28 AI penny stocks that tie artificial intelligence trends to listed companies across sectors.

- Lean into income focused opportunities by checking these 12 dividend stocks with yields > 3% that highlight companies with dividend yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.