A Look At Brookfield Infrastructure Partners (NYSE:BIP) Valuation After A Recent Share Price Pullback

Brookfield Infrastructure Partners L.P. BIP | 36.51 | +0.44% |

Why Brookfield Infrastructure Partners (BIP) is on investors’ radar today

Brookfield Infrastructure Partners (BIP) has drawn fresh attention after recent share price moves, with the units closing at US$34.29 and showing mixed returns over the past week, month, and past 3 months.

The recent 1 day share price decline of 2.45% to US$34.29 comes after a relatively steady few months, while a 1 year total shareholder return of 11.41% points to momentum that has been built over a longer horizon.

If you are comparing BIP's moves with other income focused utilities and infrastructure names, this could be a useful moment to scan stable growth stocks screener (None results) for ideas with similar steady profiles.

With units trading at US$34.29, an indicated 21% discount to a US$42.91 analyst price target and an intrinsic value marker at roughly 78% of that level, you have to ask: is this a genuine opening, or is the market already recognising Brookfield Infrastructure Partners’ future growth potential?

Price-to-Earnings of 49x: Is it justified?

At a last close of US$34.29, Brookfield Infrastructure Partners is on a P/E of 49x, which screens as expensive next to both peers and the wider integrated utilities space.

The P/E multiple tells you how much investors are currently paying for each dollar of earnings and it is a common yardstick for utilities and infrastructure names where earnings are a key anchor for valuation.

For Brookfield Infrastructure Partners, a 49x P/E suggests the market is attaching a relatively rich price tag to its earnings profile, even as earnings have only recently turned positive and revenue growth has been negative on an annual basis. At the same time, the estimated fair P/E of 40.9x implies a lower level that the market could eventually gravitate toward if sentiment or expectations cool off.

Set against an 18.6x average for the global integrated utilities industry and a 22.2x peer average, Brookfield Infrastructure Partners trades on a clearly higher multiple that assumes stronger earnings power than the group, while also sitting above the fair P/E estimate of 40.9x.

Result: Price-to-Earnings of 49x (OVERVALUED)

However, you also have to weigh risks such as 11.8% annual revenue contraction and a P/E that already reflects a relatively optimistic earnings profile.

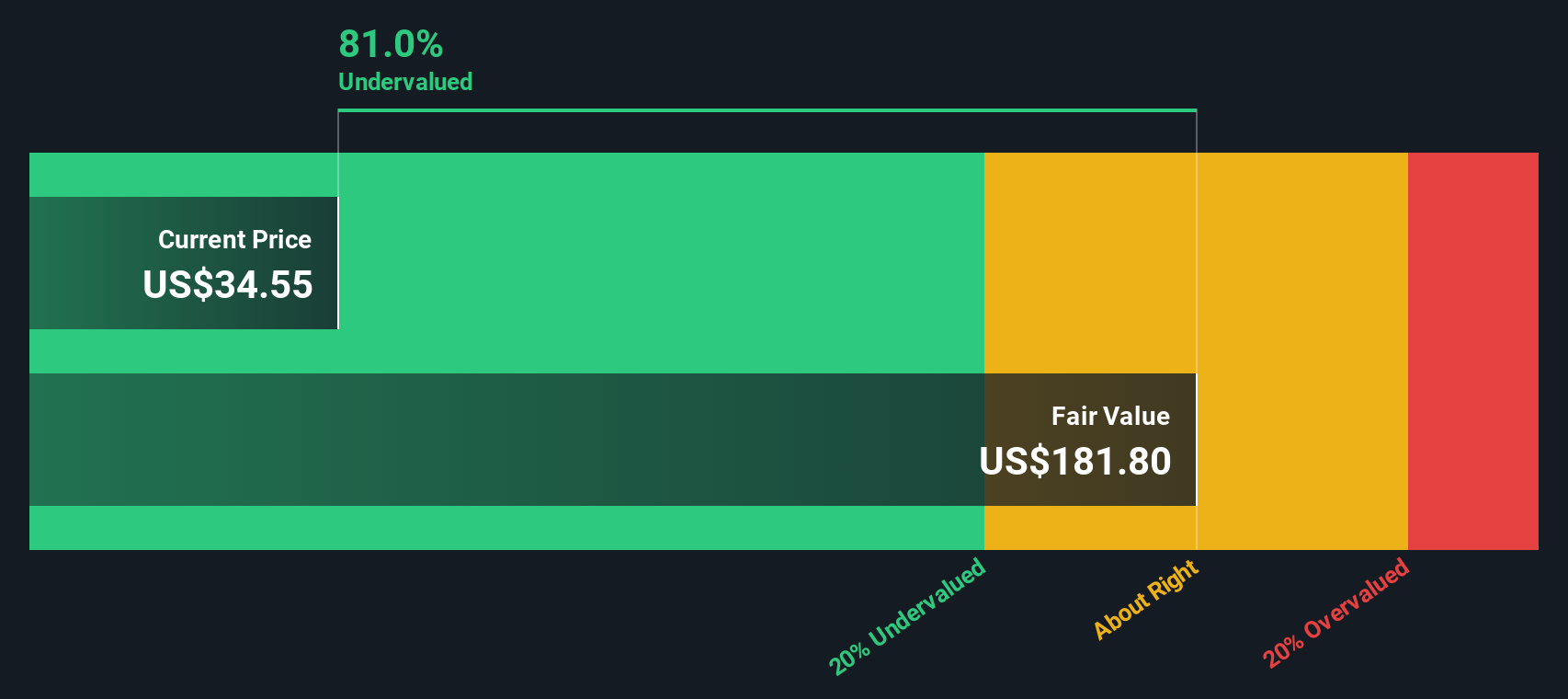

Another View: What Our DCF Model Suggests

If the 49x P/E makes BIP look expensive, our DCF model tells a very different story. On that framework, Brookfield Infrastructure Partners at US$34.29 is trading about 78.3% below an estimated fair value of US$158.37, which points to a very wide gap between price and modelled cash flows.

That kind of disconnect can reflect overly cautious earnings based metrics, or assumptions inside the DCF that may prove too optimistic. The real question for you is which set of expectations feels more realistic over the long term.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Brookfield Infrastructure Partners for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 872 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Brookfield Infrastructure Partners Narrative

If you look at these numbers and reach a different conclusion, or just prefer to test your own assumptions, you can build a personalised Brookfield Infrastructure Partners view in a few minutes using Do it your way.

A great starting point for your Brookfield Infrastructure Partners research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Brookfield Infrastructure Partners has you thinking more broadly about your portfolio, do not stop here. Your next strong idea could be only one screener away.

- Spot potential value plays early by scanning these 872 undervalued stocks based on cash flows that may be pricing in more caution than their cash flows suggest.

- Tap into future focused themes by checking out these 23 AI penny stocks that sit at the intersection of technology and real world applications.

- Strengthen your income approach by reviewing these 13 dividend stocks with yields > 3% that offer yields above 3% alongside the potential for more resilient payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.