A Look At Cadence Design Systems (CDNS) Valuation After Strong Q1 2026 Earnings And Raised Guidance

Cadence Design Systems, Inc. CDNS | 0.00 |

Cadence Design Systems (CDNS) just posted first quarter 2026 results that included US$1,474.22 million in revenue and US$335.66 million in net income, alongside raised full year guidance and fresh details on its expanded collaboration with TSMC.

The latest earnings and raised guidance appear to be feeding into strong momentum, with a 1 month share price return of 22.32% and a 3 year total shareholder return of 66.12% showing material longer term gains.

If Cadence’s AI driven story has your attention, it can be useful to see what else is moving in related areas by checking out 37 AI infrastructure stocks

With the shares up 22.32% in a month and trading at US$340.94, yet some models still suggesting the stock is undervalued, are you looking at an attractive entry point, or at a market that is already pricing in years of growth?

Most Popular Narrative: 1.1% Undervalued

Cadence’s most followed narrative pencils in a fair value of $344.64 versus the last close of $340.94, which points to only a small valuation gap but leans toward upside based on that framework.

My financial model (2024A–2030E) identifies a critical shift in the company's financial profile. While historical revenue growth clocked in at ~14% CAGR, I am modeling a more conservative 10–12% revenue growth going forward. However, the investment case relies on a massive expansion in profitability.

Read the complete narrative. Read the complete narrative.

Curious what kind of earnings power sits behind that fair value line? The narrative leans heavily on higher margins and a richer profit profile than today, driven by specific long term assumptions that are not fully obvious from headline numbers alone.

Result: Fair Value of $344.64 (UNDERVALUED)

However, this hinges on assumptions that could shift quickly, including potential P/E compression if sentiment cools and revenue pressure if China related restrictions tighten.

Another Way To Look At Value

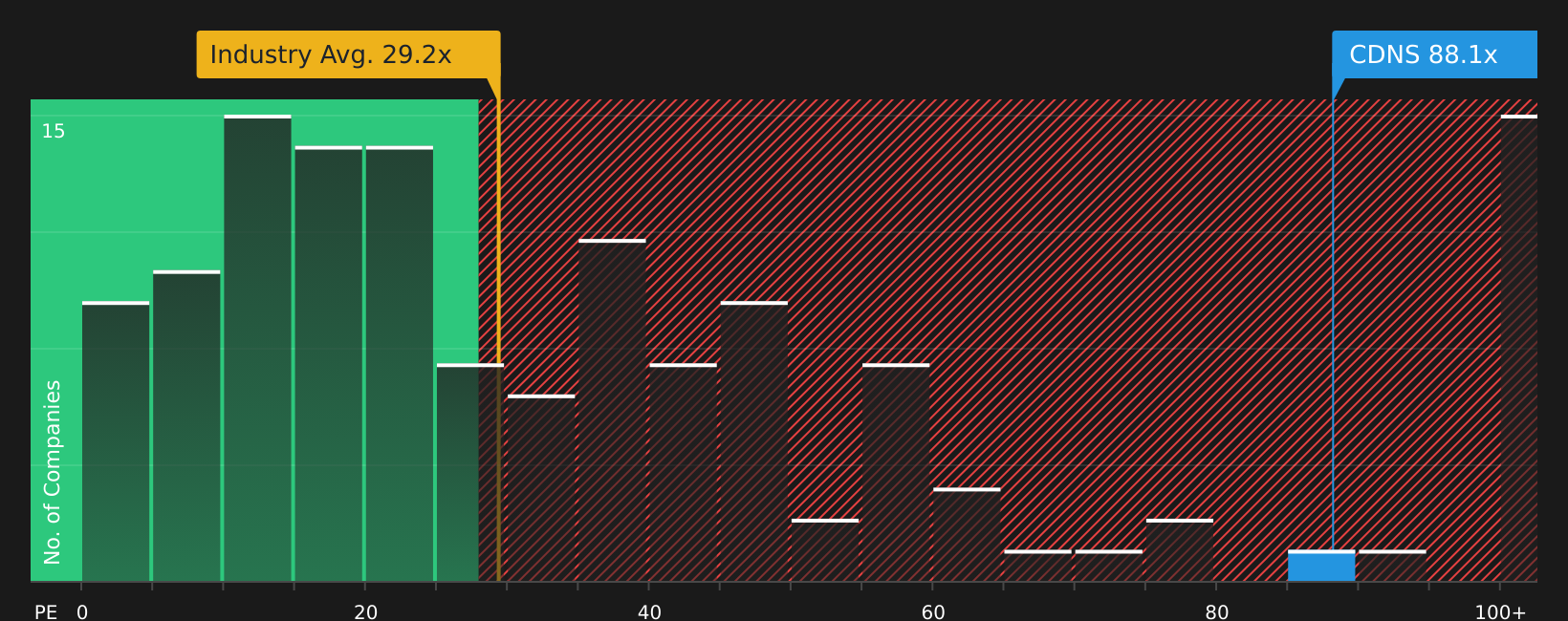

The fair value narrative suggests Cadence is only 1.1% undervalued, but the P/E ratio tells a tougher story. At 80.3x earnings, the stock trades at more than double the Software industry average of 30.3x and well above the 33.6x fair ratio our model points to. This raises the question of how much optimism is already in the price.

Next Steps

With sentiment this optimistic, it helps to move quickly, look through the numbers yourself, and decide what really matters for your portfolio. To see which positives are standing out right now, review the 2 key rewards

Looking for more investment ideas?

If Cadence is already on your radar, do not stop there. Broadening your watchlist with focused stock ideas can help you spot opportunities before the crowd.

- Target steadier growth potential by reviewing companies filtered through the 69 resilient stocks with low risk scores that aims to prioritise resilience over excitement.

- Hunt for quality at a sensible price by checking the 50 high quality undervalued stocks that highlights companies with solid fundamentals trading below their estimated worth.

- Build a cash flow focused watchlist by scanning the 13 dividend fortresses that focuses on businesses offering higher yields with income in mind.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.