A Look At Capital One (COF) Valuation After Earnings Miss And Regulatory Rate Cap Concerns

Capital One Financial Corp COF | 181.92 | -1.40% |

Capital One Financial (COF) is back in focus after its fourth quarter 2025 results missed profit expectations, with a weaker efficiency ratio and regulatory concerns around proposed credit card interest rate caps weighing on investor sentiment.

At a share price of $217.11, Capital One Financial has seen a 12.92% 1 month share price decline and a 12.43% year to date share price decline. Its 1 year total shareholder return of 8.25% and 5 year total shareholder return of 123.97% point to stronger longer term momentum, with recent earnings disappointment, higher net charge offs and regulatory questions around potential credit card rate caps all weighing on sentiment in the near term.

If this mix of earnings pressure and regulatory risk has your attention, it could be a good moment to see how other banks and lenders stack up by screening for solid balance sheet and fundamentals stocks screener (None results).

With Capital One trading below some valuation estimates and carrying a 5 year total return above 100%, the key question now is whether recent regulatory and earnings worries create an opportunity, or if the market is already pricing in future growth.

Most Popular Narrative: 19.5% Undervalued

Compared with the last close of $217.11, the most widely followed narrative implies a fair value of $269.67, using an 8.66% discount rate to weigh Capital One Financial's future cash generation.

The combination with Discover positions Capital One to leverage proprietary payments network infrastructure, enabling it to migrate Capital One debit and some credit card volume to the unregulated Discover network; this transition is expected to generate substantial incremental fee income and interchange revenue over time as scale, acceptance, and brand investments are realized.

Curious what revenue run rate, margin lift, and earnings power are baked into that fair value? The narrative leans on aggressive top line expansion, sharply higher profitability, and a very specific future earnings multiple. The numbers behind those assumptions tell a much more detailed story than the current share price alone.

Result: Fair Value of $269.67 (UNDERVALUED)

However, heavy technology and Discover integration spending, together with execution risk around the payments network, could strain margins and leave those revenue and earnings assumptions looking optimistic.

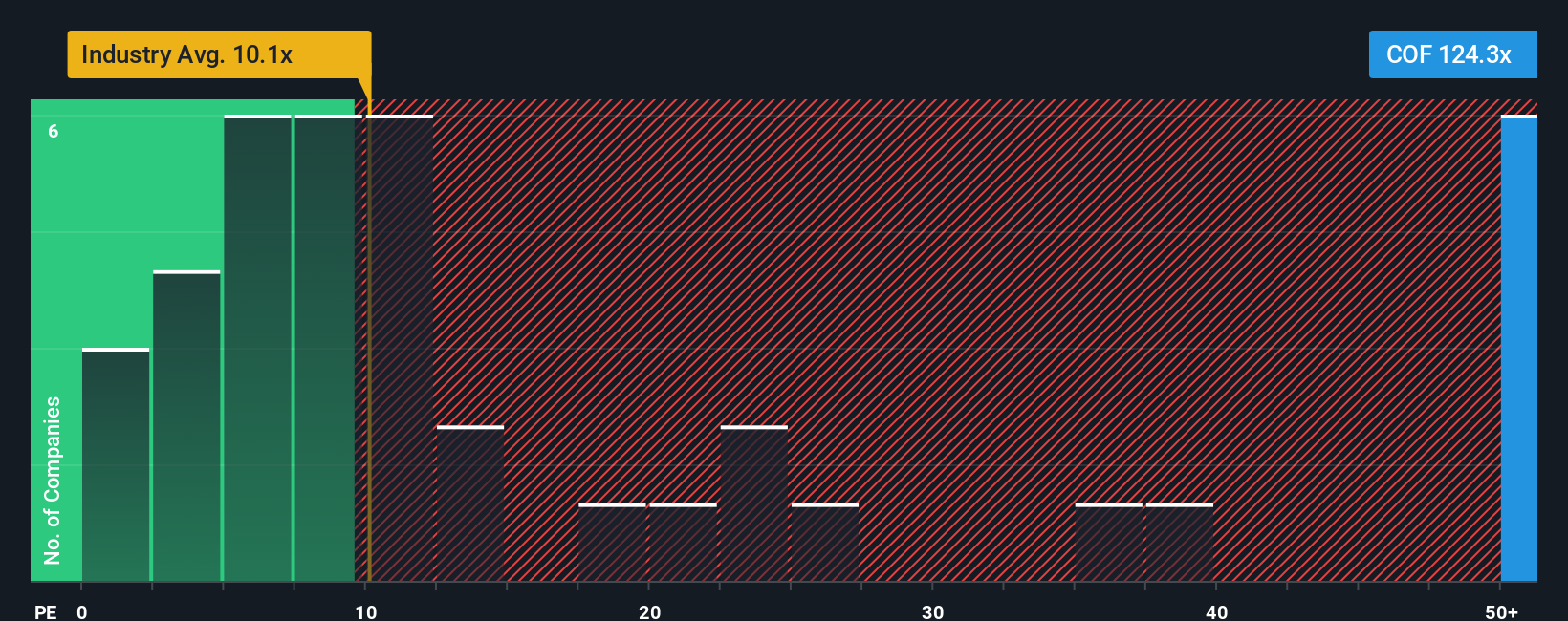

Another View: Earnings Multiple Sends A Very Different Signal

While our cash flow based fair value suggests Capital One Financial is 30.6% below that estimate, the current P/E of 74.7x tells a different story. It sits well above the Consumer Finance industry at 8.7x, the peer average at 24.8x, and even our fair ratio of 26.3x.

That kind of gap can mean the market is paying a high price for expected earnings growth, which leaves less room for error if those forecasts do not play out as assumed. So which signal do you trust more: the cash flows or the earnings multiple?

Build Your Own Capital One Financial Narrative

If you see the story differently or want to stress test these assumptions with your own inputs, you can build a custom view in minutes with Do it your way.

A great starting point for your Capital One Financial research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Capital One has sharpened your focus on risk, return, and valuation, do not stop here. Widen your search with targeted ideas built from hard numbers.

- Spot potential value gaps by scanning these 876 undervalued stocks based on cash flows where prices and cash flows tell a different story.

- Ride powerful technology trends by zeroing in on these 24 AI penny stocks that link real businesses to AI adoption.

- Target income opportunities by filtering for these 13 dividend stocks with yields > 3% to keep yields above 3% on your radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.