A Look At Capital One Financial (COF) Valuation After Recent Share Price Swings

Capital One Financial Corp COF | 181.92 | -1.40% |

Capital One Financial (COF) is back in focus after recent share price swings, with the stock showing mixed returns over the past month and over the past three months as investors reassess its value.

At a share price of US$225.46, Capital One Financial has seen a recent 7 day share price return of 3.23% after a 30 day share price return of a 10% decline. Its 1 year total shareholder return of 12.05% and 3 year total shareholder return of about 2x suggest longer term holders have had a very different experience, which may hint that recent weakness reflects shifting views on the balance between growth potential and risk.

If Capital One’s recent swings have you thinking about where else to put cash to work, now could be a good time to broaden your search with fast growing stocks with high insider ownership.

With Capital One trading at US$225.46 and sitting around a 30% discount to an estimated intrinsic value and roughly 23% below analyst targets, investors may question whether this represents a genuine opportunity or whether future growth is already priced in.

Most Popular Narrative: 16.4% Undervalued

Capital One Financial’s most followed narrative pegs fair value at $269.67, comfortably above the recent $225.46 share price, which helps explain why some investors see current weakness as interesting.

The combination with Discover positions Capital One to leverage proprietary payments network infrastructure, enabling it to migrate Capital One debit and some credit card volume to the unregulated Discover network, this transition is expected to generate substantial incremental fee income and interchange revenue over time as scale, acceptance, and brand investments are realized.

Curious how a payments network shift, margin rebuild and higher long term earnings power feed into that fair value line? The full narrative spells out the revenue ramp, profitability assumptions and the earnings multiple that all have to line up to support that price.

Result: Fair Value of $269.67 (UNDERVALUED)

However, heavy spending on technology and Discover integration, along with rising integration costs, could pressure margins if the expected revenue benefits do not materialize.

Another View: Earnings Multiple Flags a Very Different Story

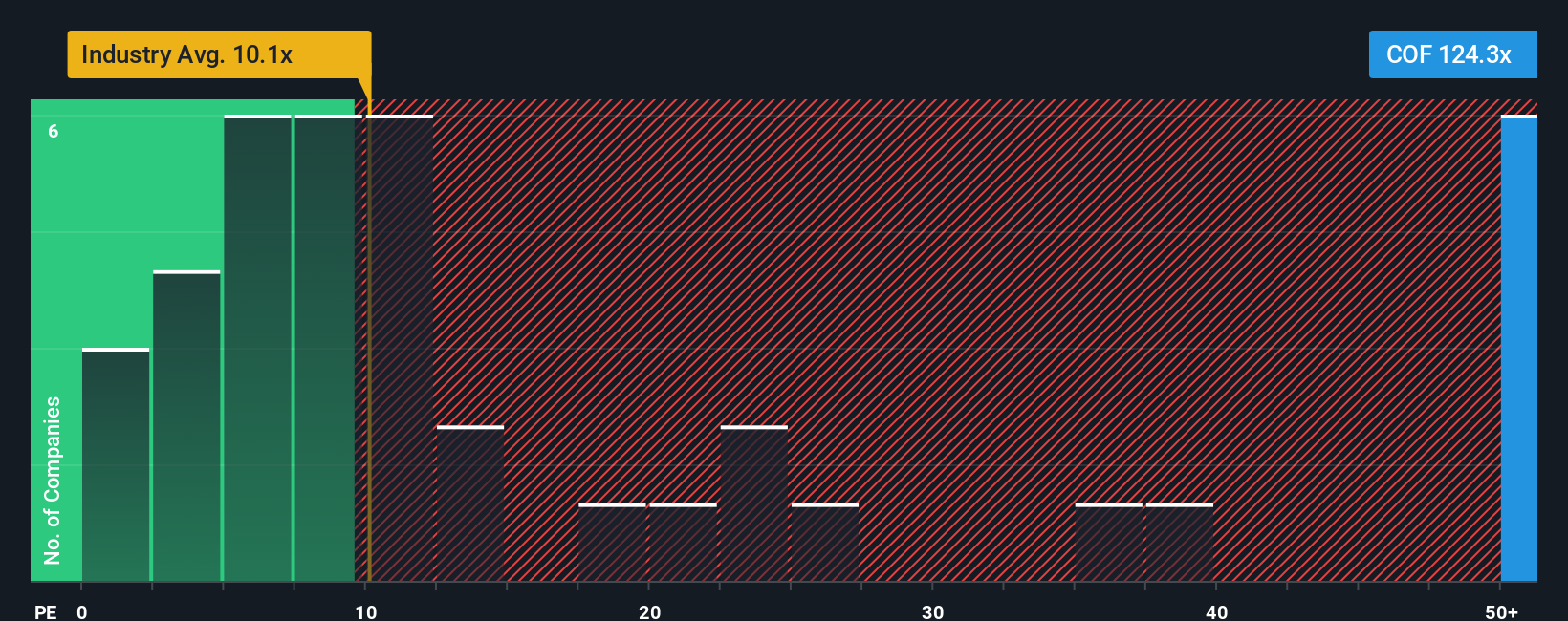

While our cash flow based fair value points to Capital One looking cheap, the earnings multiple paints a tougher picture. At a P/E of 77.6x versus 9.5x for the US Consumer Finance industry, 25.8x for peers, and a fair ratio of 26.7x, the gap suggests meaningful valuation risk if expectations reset.

Build Your Own Capital One Financial Narrative

If you look at the numbers and come to a different conclusion, or prefer to stress test the assumptions yourself, you can build a custom view in minutes with Do it your way.

A great starting point for your Capital One Financial research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are weighing what to do with Capital One, do not stop there. Broaden your watchlist with a few focused idea lists that match your style.

- Target potential mispricings by checking out these 868 undervalued stocks based on cash flows that may offer more attractive entry points based on cash flow fundamentals.

- Ride the AI tailwind by scanning these 30 AI penny stocks where companies are leaning into artificial intelligence themes across different parts of the market.

- Boost your income focus by reviewing these 11 dividend stocks with yields > 3% that pair higher yields with equity exposure instead of holding only cash.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.