A Look At Carrier Global (CARR) Valuation After Earnings, Buyback Completion And New AI Feature Launch

Carrier Global Corp. CARR | 61.63 | -4.69% |

Carrier Global (CARR) is back in focus after a packed early February, combining its fourth quarter and full year 2025 earnings release with a completed share repurchase tranche, a fresh AI feature launch, and a supportive analyst update.

The recent cluster of events, including the latest earnings release, completion of a multi year buyback and the launch of Carrier Abound’s AI powered “Tell Me More” feature, has coincided with a strong upswing, with a 30 day share price return of 17.01% and a 5 year total shareholder return of 88.51%. This suggests momentum has been building around the story despite a more modest 1 year total shareholder return of 2.47%.

If this mix of AI, building technology and shareholder returns has your attention, it could be a good moment to scan other opportunities using our 24 power grid technology and infrastructure stocks as a starting point for further ideas.

With the shares up strongly over the past month and trading at $65.82 with a modest discount to both analyst targets and intrinsic value estimates, you have to ask: is there still a buying window here, or is the market already pricing in the next leg of growth?

Most Popular Narrative: 8.8% Undervalued

The most followed narrative puts Carrier Global’s fair value around $72 per share, slightly above the last close at $65.82, and frames that gap around long term earnings power.

Carrier's introduction of differentiated products, such as air-cooled commercial heat pumps and the integration of HEMS technology with Google Cloud's AI, positions them to capture the growing demand for sustainable and smart energy solutions, potentially driving future revenue growth.

The company's strong performance in the aftermarket space, with double digit growth and increased attachment rates on chillers, is expected to bolster net margins through high margin service offerings and customer retention.

Curious what sits behind that $72 fair value mark? The narrative leans on steady revenue expansion, thicker margins and a future earnings multiple that assumes real staying power. Want to see which exact growth and profit assumptions have to line up for that discount to close?

The fair value estimate in this narrative is built using a discount rate just under 9%, alongside projected gains in revenue, profitability and earnings per share over the coming years, all filtered through what analysts see as a reasonable future P/E range for Carrier’s position in climate and energy solutions.

Result: Fair Value of $72.18 (UNDERVALUED)

However, there are still real pressure points, including weaker demand in parts of climate solutions and light commercial HVAC, as well as tariff and currency headwinds that could weigh on profitability.

Another Angle On Valuation

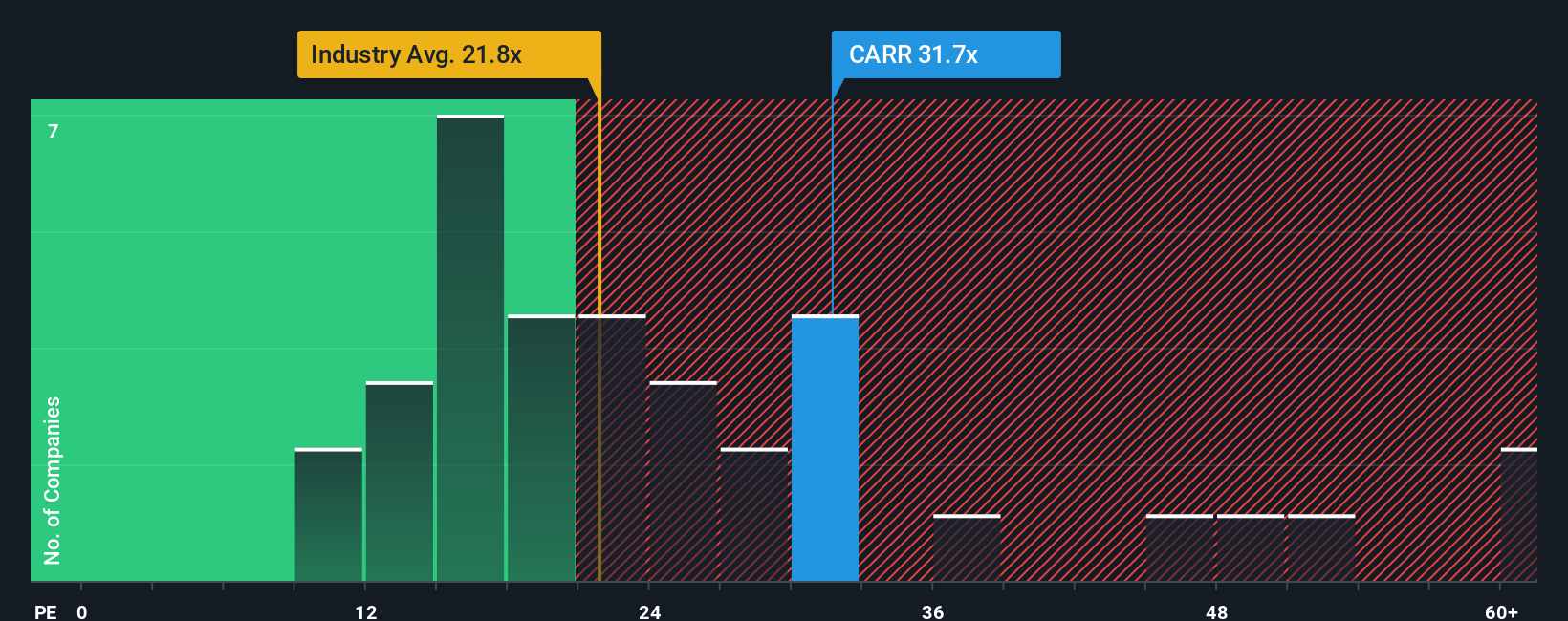

That 8.8% discount to fair value sounds appealing, but the earnings multiple tells a different story. At a P/E of 37.8x, Carrier trades higher than the US Building industry at 23.8x, above peers at 31.7x, and even above its own 37.1x fair ratio. That gap points to less room for error, so investors may consider whether the growth narrative is strong enough to justify paying a higher multiple.

Build Your Own Carrier Global Narrative

If that story does not quite fit your view, or you would rather test the numbers yourself, you can build a custom thesis in just a few minutes: Do it your way

A great starting point for your Carrier Global research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Carrier has sharpened your thinking, do not stop here. Your next strong move could come from comparing a few focused stock ideas side by side in minutes.

- Target strong value potential by scanning our 51 high quality undervalued stocks that highlights companies combining quality fundamentals with prices that may sit below their estimated worth.

- Prioritize resilience and peace of mind with the 83 resilient stocks with low risk scores, which surfaces companies that score well on stability and risk metrics.

- Spot underfollowed opportunities using the screener containing 24 high quality undiscovered gems, a list built to reveal quality businesses that may not yet be widely on the market’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.