A Look At Carvana (CVNA) Valuation After Recent Share Price Pullback

Carvana Co. Class A CVNA | 302.04 | +0.22% |

Carvana stock moves after recent performance shift

Carvana (CVNA) has drawn fresh attention after a recent pullback, with the share price down about 16% over the past month and roughly 35% over the past 3 months.

While the share price has given back ground recently, with a 1-day share price return decline of 4.39% and a 30-day share price return decline of 16.44%, the 1-year total shareholder return of 47.31% and very large 3-year total shareholder return suggest longer term momentum has been strong, even as sentiment looks more cautious at the current share price of US$281.28.

If Carvana’s swings have you thinking about where else growth and risk could be priced differently, this is a good moment to scan 20 top founder-led companies

With Carvana generating US$20.3b in revenue and US$1.4b in net income, yet trading at US$281.28 with an indicated intrinsic discount, you have to ask: is this a mispriced growth story, or is the market already factoring in what comes next?

Most Popular Narrative: Fairly Valued

Carvana’s last close at $281.28 sits against a narrative fair value that implies no clear discount or premium, putting the focus firmly on how that value is built.

There are growing concerns among some market observers that Carvana's business model may be masking deeper financial instability. The company has a long history of operating with negative cash flow followed with rapid debit expansion, and unusually aggressive revenue recognition practices that raise questions about the sustainability of its margins. Analysts have also noted that Carvana's reported improvements in profitability often coincide with accounting adjustments rather than genuine operational strength, suggesting the possibility of earnings "smoothing out." Additionally, the firm's reliance on securitizing subprime auto loans creates opacity around the true quality of its assets; rising delinquencies in the used car loan market increase the risk that these securities are overvalued. When a company simultaneously carries heavy debt, thin cash reserves and complex financial structures that are difficult for outside investors to verify, it births skepticism.

Want to see how a fairly valued label still sits on top of this kind of earnings, cash flow and balance sheet tension? The full narrative pulls together profitability assumptions, margin resilience and funding structure into a single fair value story, and the details behind those inputs may challenge how you think about this price.

Result: Fair Value of $0 (ABOUT RIGHT)

However, fresh scrutiny from regulators or renewed focus on debt, cash flow, and loan performance could quickly challenge the idea that today’s valuation is comfortable.

Another View: DCF points to a different story

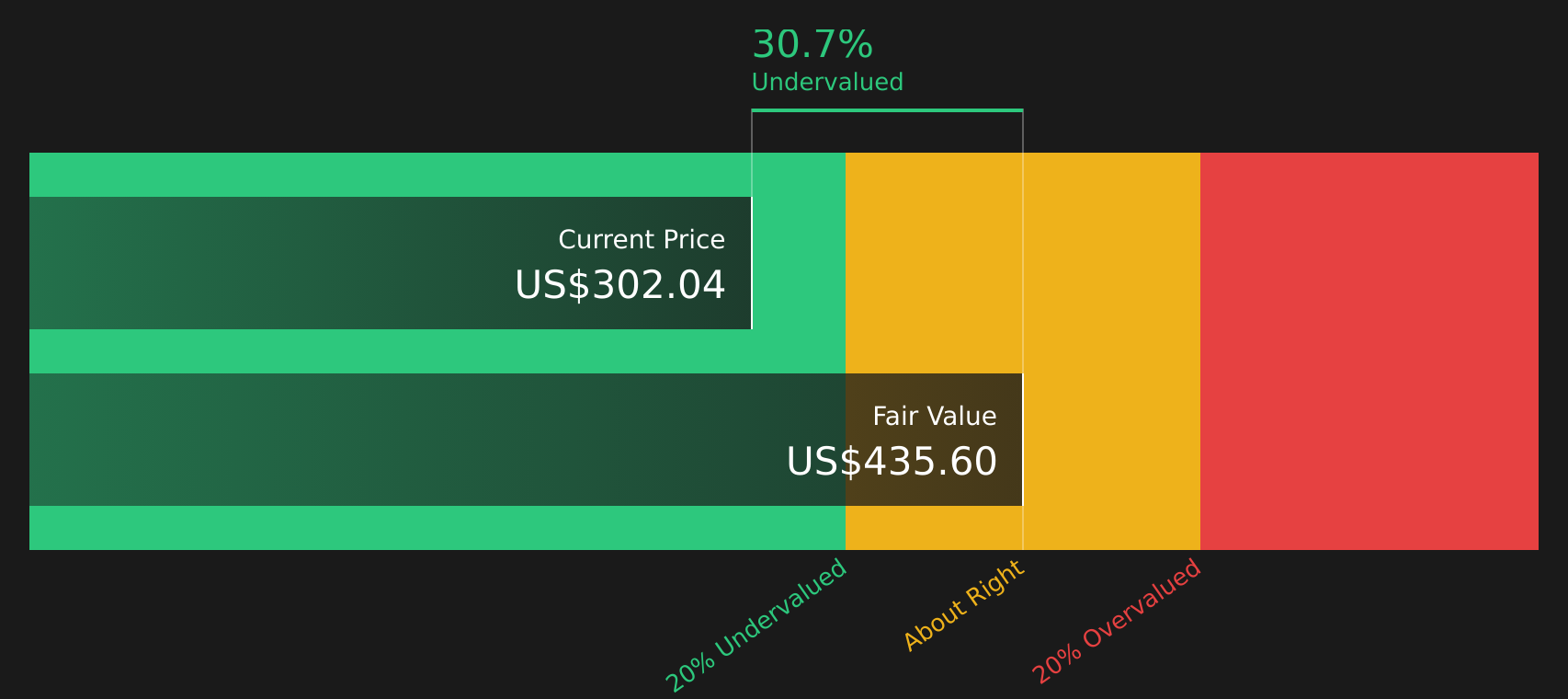

While the fair value narrative suggests Carvana is roughly in line with its current $281.28 price, the SWS DCF model points in another direction, with an estimated value of $437.94. That gap frames Carvana as undervalued on cash flow terms, so which story do you trust more?

For a closer look at how that cash flow view is built, and how sensitive it might be to changes in earnings or funding costs, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Carvana for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of caution and optimism feels hard to balance, do not wait for the crowd to settle it for you. Instead, go straight to the source data and check the 4 key rewards

Looking for more investment ideas?

If Carvana sits on your watchlist, do not stop there; use the same structured approach to scan for other opportunities that might better fit your risk and income goals.

- Target reliable income by reviewing companies with robust payouts and durable cash flows through the 13 dividend fortresses

- Hunt for value by scanning companies that pair quality fundamentals with attractive pricing using the 53 high quality undervalued stocks

- Prioritize peace of mind by focusing on businesses with resilient balance sheets and lower risk profiles via the 67 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.