A Look At Carvana (CVNA) Valuation After Recent Share Price Volatility

Carvana CVNA | 0.00 |

Carvana (CVNA) has drawn fresh attention after recent trading left the stock down about 12% over the past month but ahead roughly 15% over the past 3 months, inviting a closer look at its drivers.

At a share price of US$67.25, Carvana’s recent swings, including a 1 day share price decline of 3.39% and a 7 day share price return of 5.66%, sit alongside a year to date share price return that is down 15.99% and a 3 year total shareholder return that is very large. This combination suggests that momentum has cooled recently after an earlier surge in investor optimism.

If you are weighing what to watch next in high growth stories, it could be worth widening your search to the 20 top founder-led companies

So with Carvana’s share price pulling back this year, yet still carrying a very large 3 year return, is the recent weakness giving you a fresh entry point, or is the stock already pricing in future growth?

Most Popular Narrative: 28% Undervalued

Carvana’s most followed narrative points to a fair value of about $92.90 per share versus the current $67.25, framing a material valuation gap built on growth, margin and discount rate assumptions that investors can scrutinize.

The analysts have a consensus price target of $92.9 for Carvana based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $44.1 billion, earnings will come to $2.9 billion, and it would be trading on a PE ratio of 32.1x, assuming you use a discount rate of 8.3%.

Want to see what underpins that fair value? The narrative is based on brisk revenue expansion, higher margins and a premium future earnings multiple. Curious how those ingredients combine into $92.90.

Result: Fair Value of $92.90 (UNDERVALUED)

However, that upside story can be challenged if execution wobbles around ADESA integrations and reconditioning costs, or if heavier marketing spend fails to translate into durable growth.

Another View: High Multiple, Higher Expectations

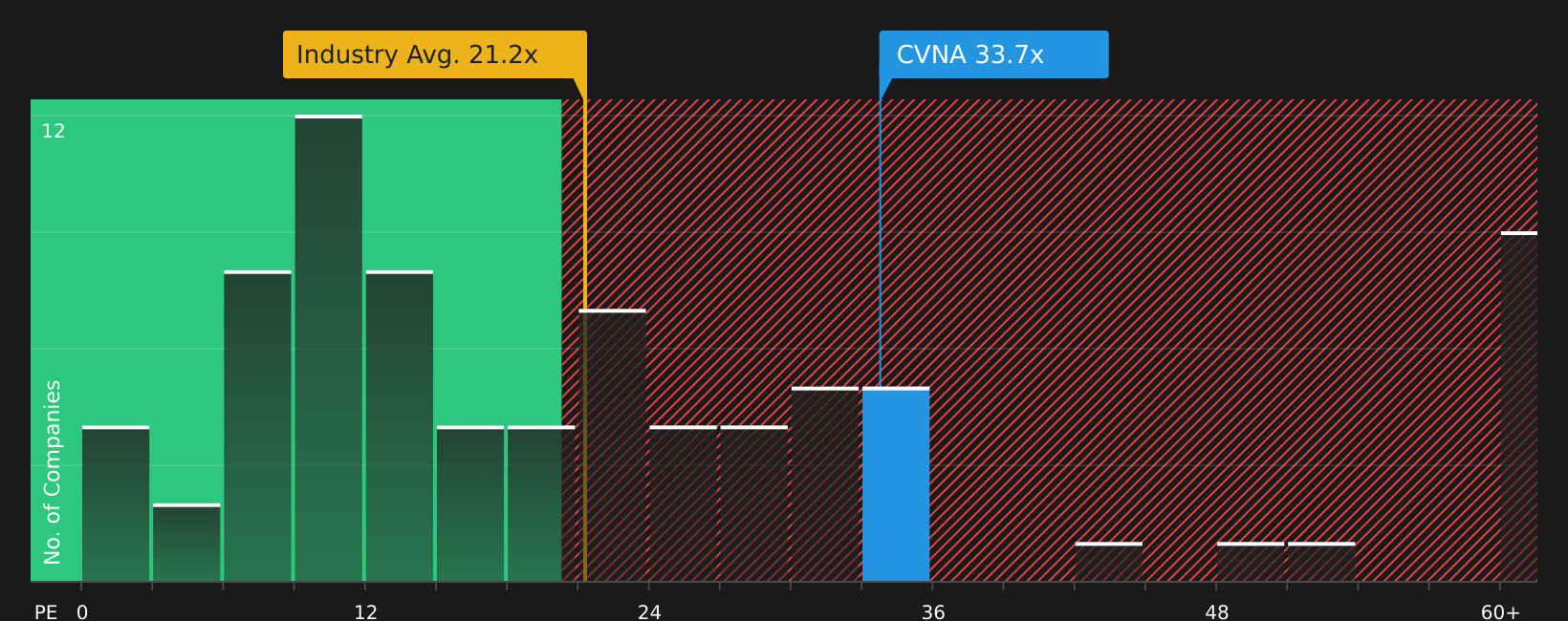

The most popular narrative leans on analyst fair value of about US$92.90. However, current pricing already embeds a rich P/E of 33.4x compared with 20.1x for the US Specialty Retail industry, 20.6x for peers and a fair ratio of 32.8x. That leaves less room for error if the story slips at all.

Next Steps

With mixed signals across returns, valuation and sentiment, it makes sense to move quickly, check the underlying data for yourself, and weigh up the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If Carvana has sharpened your focus on valuation and risk, do not stop here. Widen your search now and compare it with other focused stock ideas.

- Target dependable cash generators by scanning companies with stronger margins and sensible pricing through the 48 high quality undervalued stocks

- Prioritise resilience by checking out stocks that pass tougher balance sheet and fundamentals checks using the solid balance sheet and fundamentals stocks screener (46 results)

- Hunt for off-the-radar opportunities before they gain broader attention with the screener containing 20 high quality undiscovered gems

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.