A Look At Carvana (CVNA) Valuation After Record Quarterly Results And Operational Expansion

Carvana CVNA | 0.00 |

Carvana (CVNA) is back in focus after reporting first quarter 2026 results, with revenue of US$6.43b, net income of US$250 million, and diluted EPS from continuing operations of US$1.69.

Carvana's share price has been volatile, with a 22.89% 1 month share price return and a 2.72% year to date decline, alongside a very large 3 year total shareholder return that signals strong long term momentum.

If Carvana’s moves have you thinking about what else is out there in high growth areas, this is a good moment to scan 19 top founder-led companies

With Carvana now posting US$6.43b in quarterly revenue, US$250 million in net income and a 52% revenue jump year on year, plus a share price near US$389, the key question is simple: is there still value left here, or is the stock already pricing in future growth?

Most Popular Narrative: Fairly Valued

Carvana’s most followed narrative pegs fair value roughly in line with the recent $389.38 close, which puts the focus squarely on how that view is built.

There are growing concerns among some market observers that Carvana's business model may be masking deeper financial instability. The company has a long history of operating with negative cash flow followed with rapid debit expansion , and unusually aggressive revenue recognition practices that raise questions about the sustainability of its margins.

Curious what supports a fair value call alongside this kind of scrutiny? The narrative leans heavily on projected profitability, improving margins and a rich earnings multiple. The exact mix of those inputs is where the story gets interesting.

Result: Fair Value of $0 (ABOUT RIGHT)

However, sustained regulatory scrutiny or any renewed questions around accounting practices could quickly challenge the idea that today’s price already reflects fair value.

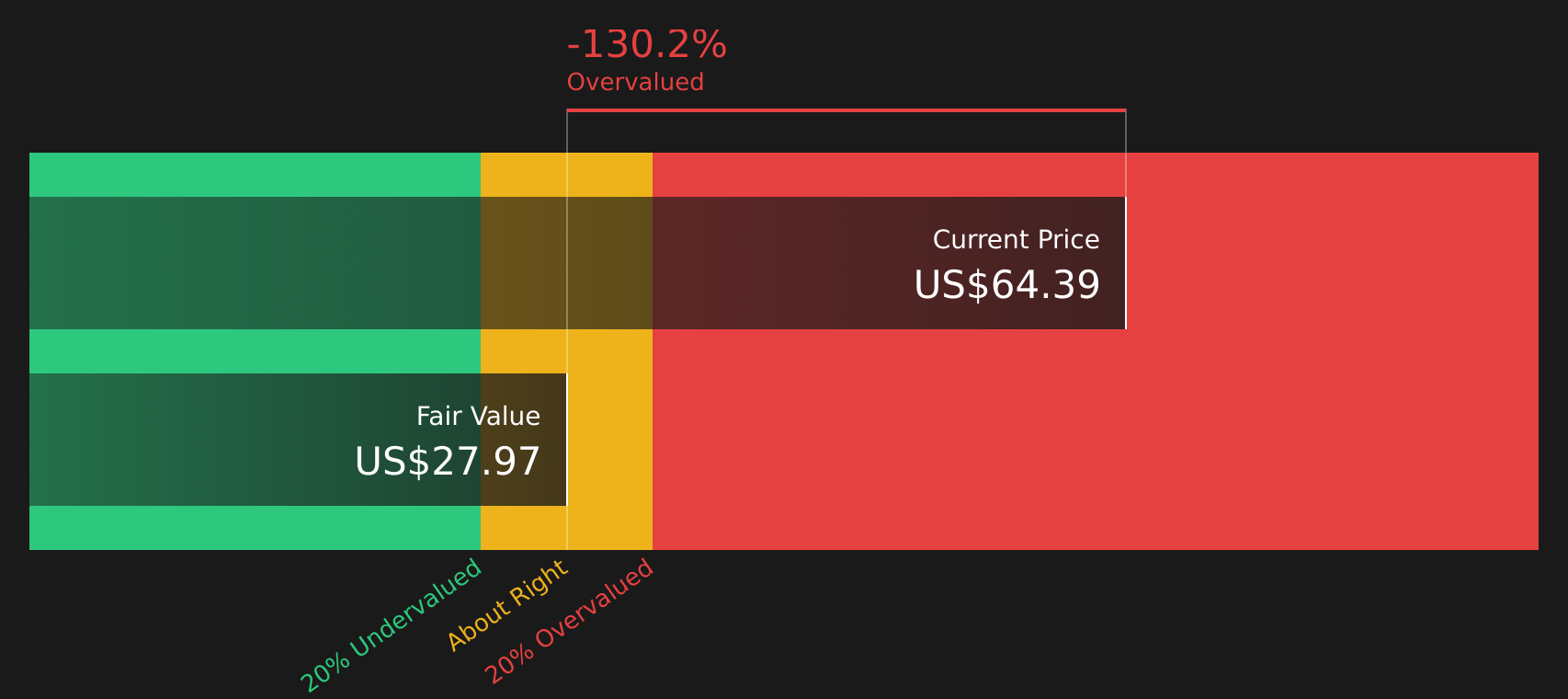

Another View: Cash Flows Paint a Harsher Picture

While the popular narrative sits close to Carvana’s recent $389.38 share price, the SWS DCF model tells a different story. On that view, the stock trades around $389 against an estimated future cash flow value of $137.84, which points to a heavily overvalued setup. So which lens do you trust more when real cash has to back the equity story?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Carvana for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment split between opportunity and concern, this is the moment to look through the numbers yourself and decide where you stand. To weigh both sides of the story, start by checking the 2 key rewards and 1 important warning sign.

Ready to hunt for your next idea?

If Carvana has sharpened your appetite for opportunities, do not stop here. Use this moment to compare other stocks and see where the risk reward tradeoff looks more compelling.

- Zero in on quality at a discount by checking stocks filtered through the 44 high quality undervalued stocks.

- Prioritize resilience by scanning companies highlighted in the 74 resilient stocks with low risk scores.

- Spot potential future standouts early by reviewing the screener containing 23 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.