A Look At Cava Group (CAVA) Valuation As EPS Weakness Meets Revenue Growth And Premium P/E Concerns

CAVA Group, Inc. CAVA | 79.63 | -0.64% |

CAVA Group (CAVA) is coming into focus as investors weigh an expected 40% year over year earnings per share decline against projected 17.93% revenue growth in its upcoming report, alongside concerns about an above industry P/E ratio.

CAVA Group’s recent share price action reflects this tension, with a 1 day share price return of 2.16%, a 7 day share price return of 2.31%, a 90 day share price return of 20.89%, and a 1 year total shareholder return of a 57.20% loss. This suggests that recent momentum contrasts with a much weaker longer term experience as investors weigh fast casual spending pressures against premium valuation concerns.

If CAVA’s swings have you rethinking concentration in a single name, it could be worth broadening your watchlist with fast growing stocks with high insider ownership.

With earnings expected to fall even as revenue grows, and with CAVA trading on a premium P/E, are you looking at an undervalued fast casual name under pressure, or is the market already pricing in every bit of future growth?

Most Popular Narrative: 14.5% Undervalued

Against CAVA Group’s last close at $60.89, the most followed narrative places fair value at $71.20, which frames the current premium P/E debate in a very different light.

Rapid geographic expansion into new and underserved markets, supported by strong new unit performance and a robust target of at least 1,000 restaurants by 2032, is likely to accelerate systemwide sales and drive higher topline revenue growth.

Growing consumer demand among younger demographics for healthy, flavorful, and customizable dining, especially Mediterranean cuisine, positions CAVA to benefit from increased customer traffic and enhanced brand equity, supporting both revenue and long term pricing power.

Want to see what kind of revenue path and margin profile this assumes, how rich a future earnings multiple needs to be to make $71.20 stack up, how that compares with typical restaurant names, and what it implies for today’s premium price tag?

Result: Fair Value of $71.20 (UNDERVALUED)

However, this story can unravel if aggressive expansion toward 1,000 restaurants strains returns, or if softer fast casual demand and rising competition squeeze margins and traffic.

Another Take: Multiples Paint A Tougher Picture

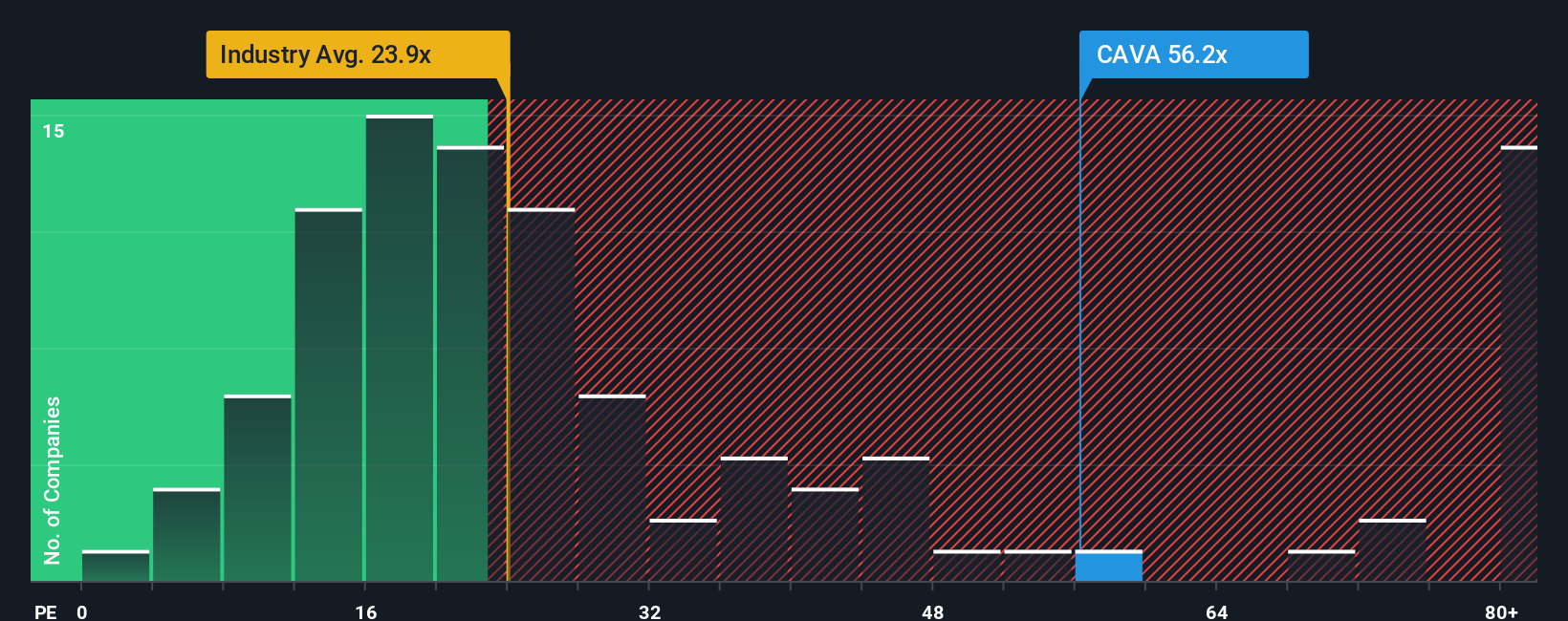

That 14.5% undervaluation narrative runs into a very different signal when you look at plain P/E. CAVA trades at 51.4x earnings, compared with 20.7x for the US Hospitality industry, 47.2x for peers, and a fair ratio of 19.3x. That is a wide gap for you to be comfortable with, or not?

Build Your Own CAVA Group Narrative

If you see the numbers differently or simply prefer to test your own assumptions, you can build a custom CAVA Group view in minutes with Do it your way.

A great starting point for your CAVA Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If CAVA has you thinking differently about risk and reward, do not stop here; broaden your research now so you are not late to the next opportunity.

- Spot potential value opportunities early by scanning these 867 undervalued stocks based on cash flows that align with your return expectations and risk tolerance.

- Capture growth themes in digital assets by reviewing these 19 cryptocurrency and blockchain stocks tied to blockchain, payments, and related infrastructure.

- Target future focused sectors by checking these 23 quantum computing stocks at the intersection of computing power, security, and advanced research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.