A Look At Centessa Pharmaceuticals (CNTA) Valuation After New Orexin Pipeline And Pre Commercial Plans

Centessa Pharmaceuticals CNTA | 39.61 39.41 | +0.05% -0.50% Pre |

Centessa Pharmaceuticals (CNTA) has drawn fresh attention after outlining 2026 plans for its orexin pipeline, including moving lead asset ORX750 toward registrational studies and advancing ORX142 into clinical trials, while also preparing for a pre-commercial shift.

The recent orexin updates come after a mixed price pattern, with a 1 month share price return of 11.86% and a 3 month share price return decline of 10.5%. However, the 3 year total shareholder return of about 7x suggests that sentiment has shifted meaningfully over a longer horizon as investors react to clinical milestones and 2026 guidance.

If Centessa’s orexin story has caught your eye, you might also want to see what else is happening across sleep and neurology related drug research through our screener of 25 healthcare AI stocks.

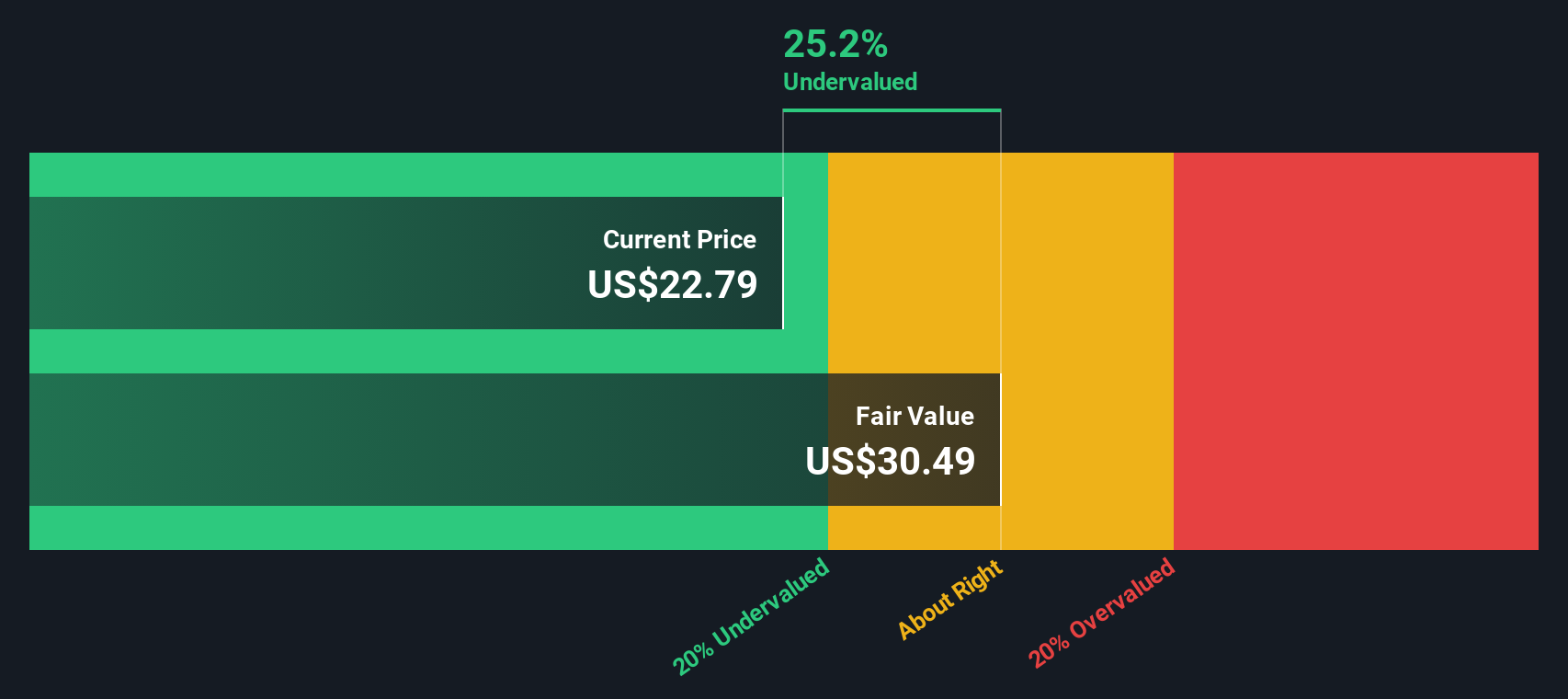

With shares up 44.76% over the past year and trading at a reported 82.33% intrinsic discount, along with a sizeable gap to the average analyst target, the key question is whether Centessa is still mispriced or if the market is already recognizing its future potential.

Preferred Price to Book of 11.7x: Is It Justified?

Centessa trades on a P/B of 11.7x, which sits well above both its closest biotech peers at 9.2x and the broader US Biotechs industry at 2.7x.

The P/B ratio compares the company’s market value to its book value, so a higher figure often reflects strong expectations for future value creation relative to the assets on the balance sheet. For an early stage, clinical focused pharma group that is still loss making, a rich P/B usually signals that investors are putting significant weight on the potential of the pipeline rather than current financials.

Here, the statements flag a clear tension. On one side, Centessa is currently unprofitable, is forecast to remain unprofitable over the next 3 years, and has a negative return on equity of 80.48%. On the other side, it is trading at 82.5% below an internal estimate of fair value based on the SWS DCF model, which puts future cash flow value at $138.50 per share compared to the last close of $24.71.

Relative to the US Biotechs industry average P/B of 2.7x and a peer group at 9.2x, Centessa’s 11.7x multiple stands out as materially higher. That suggests the market is assigning a premium price tag compared to asset value benchmarks, even as the SWS DCF model signals a very large gap between the share price and its estimate of future cash flow value.

Result: Price to book ratio of 11.7x (OVERVALUED)

However, you still have to weigh clinical and regulatory setbacks for ORX750 or ORX142, as well as the impact of ongoing losses with net income at a $242.698 million loss.

Another View: DCF Points in the Opposite Direction

While the 11.7x P/B suggests a rich price tag, the SWS DCF model tells a very different story. It puts future cash flow value at $138.50 per share versus the recent $24.71 price, implying Centessa is deeply undervalued rather than stretched. Which signal do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Centessa Pharmaceuticals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 56 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Centessa Pharmaceuticals Narrative

If you look at the numbers and come to a different conclusion, or simply prefer to test your own assumptions, you can build a personalized view on Centessa in just a few minutes, starting with Do it your way.

A great starting point for your Centessa Pharmaceuticals research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop with a single stock. The right shortlist of ideas can make a big difference.

- Target potential bargains by scanning companies that screen as 56 high quality undervalued stocks, so you can quickly focus on names where quality and price may line up better.

- Prioritize staying power by reviewing our solid balance sheet and fundamentals stocks screener (44 results), helping you concentrate on businesses with financial cushions that may handle tough periods more comfortably.

- Hunt for off the radar opportunities with the screener containing 23 high quality undiscovered gems, so you do not miss companies that have strong fundamentals but limited attention so far.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.