A Look At Centuri Holdings (CTRI) Valuation After $300 Million In New Awards And Reiterated Guidance

Centuri Holdings, Inc. CTRI | 0.00 |

Why the latest $300 million in awards matters for Centuri Holdings

Centuri Holdings (CTRI) has drawn fresh attention after announcing more than $300 million in new commercial awards across gas, electric, and broader energy infrastructure services in the U.S. and Canada.

These bookings, alongside recent quarterly results and reiterated guidance, give investors more concrete data on the company’s current demand trends, contracted work, and the way its utility-focused business is positioning within a large stated addressable market.

Centuri’s latest awards arrive after a sharp 21.9% decline in the 30 day share price return, yet the stock still carries an 18.8% year to date share price return and a 43.3% 1 year total shareholder return. This suggests that longer term momentum has remained positive even as near term expectations reset around valuation and risk.

If this kind of utility and energy infrastructure story interests you, it can be useful to compare it with other grid focused opportunities by scanning 33 power grid technology and infrastructure stocks

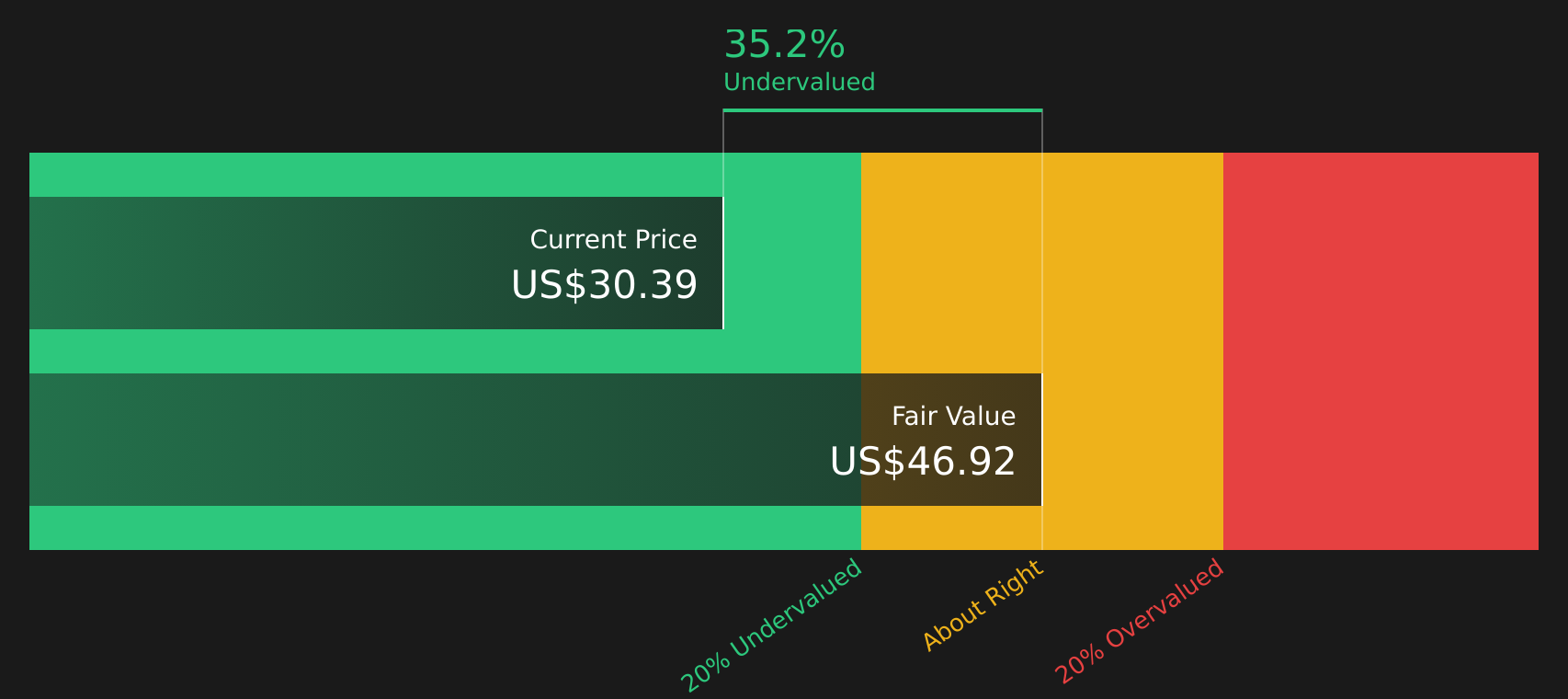

With Centuri trading at US$30.67, an indicated 21% discount to the average analyst price target and a 35% gap to one intrinsic value estimate, you have to ask: is there still upside here, or is the market already pricing in future growth?

Most Popular Narrative: 26% Overvalued

At a last close of $30.67 versus a narrative fair value of $24.33, Centuri is framed as pricing in a richer future than that model suggests.

Record backlog of approximately $5.9 billion and a robust $13 billion opportunity pipeline, including over 600 strategic bids, supports sustained revenue growth by converting awarded work into a higher, more stable top line.

Want to see what sits behind that backlog story? The narrative leans heavily on future revenue, margin expansion and a very specific earnings trajectory. Curious which assumptions really carry the fair value.

Result: Fair Value of $24.33 (OVERVALUED)

However, there is still a risk that contract wins, pricing actions and operational tweaks deliver stronger earnings than assumed, which could challenge the view that the stock is 26% overvalued.

Another Take: Cash Flow Points the Other Way

While the consensus narrative sees Centuri as 26% overvalued versus a $24.33 fair value, the SWS DCF model points in the opposite direction, with a future cash flow value of $47.01 per share, about 53% above the current $30.67 price. Which yardstick do you trust more for a long term view?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Centuri Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed messages in the data so far? If you think Centuri might sit somewhere between risk and reward, move quickly, review the details and weigh up the 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If Centuri has caught your eye, do not stop here; broaden your watchlist now so you are not relying on a single stock story or sector trend.

- Target resilient upside by scanning 63 resilient stocks with low risk scores that combine measured risk profiles with clear financial characteristics.

- Hunt for quality at a potential discount through 46 high quality undervalued stocks built around fundamentals, not hype.

- Spot potential early movers with 24 elite penny stocks with strong financials where strong balance sheets and business quality help filter out weaker ideas.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.