A Look At Centuri Holdings (CTRI) Valuation After Record Revenue And 2026 Outlook Update

Centuri Holdings, Inc. CTRI | 0.00 |

Record revenue, new contracts and board changes set the stage

Centuri Holdings (CTRI) recently reported record annual revenue above US$3b, outlined its outlook for 2026, secured over US$870m in new North American awards, and added new independent directors to its board.

The strong operating update sits alongside a 30 day share price return of 29.24% and a year to date share price return of 52.01%, while a 1 year total shareholder return of 111.25% points to momentum that has been building rather than fading.

If this kind of move has your attention, it could be a good moment to see what else is gaining traction in utility and infrastructure related names through 34 power grid technology and infrastructure stocks

With the share price already up sharply and record revenue above US$3b on the table, the key question now is whether Centuri is still trading below its intrinsic value or if the market is already pricing in future growth.

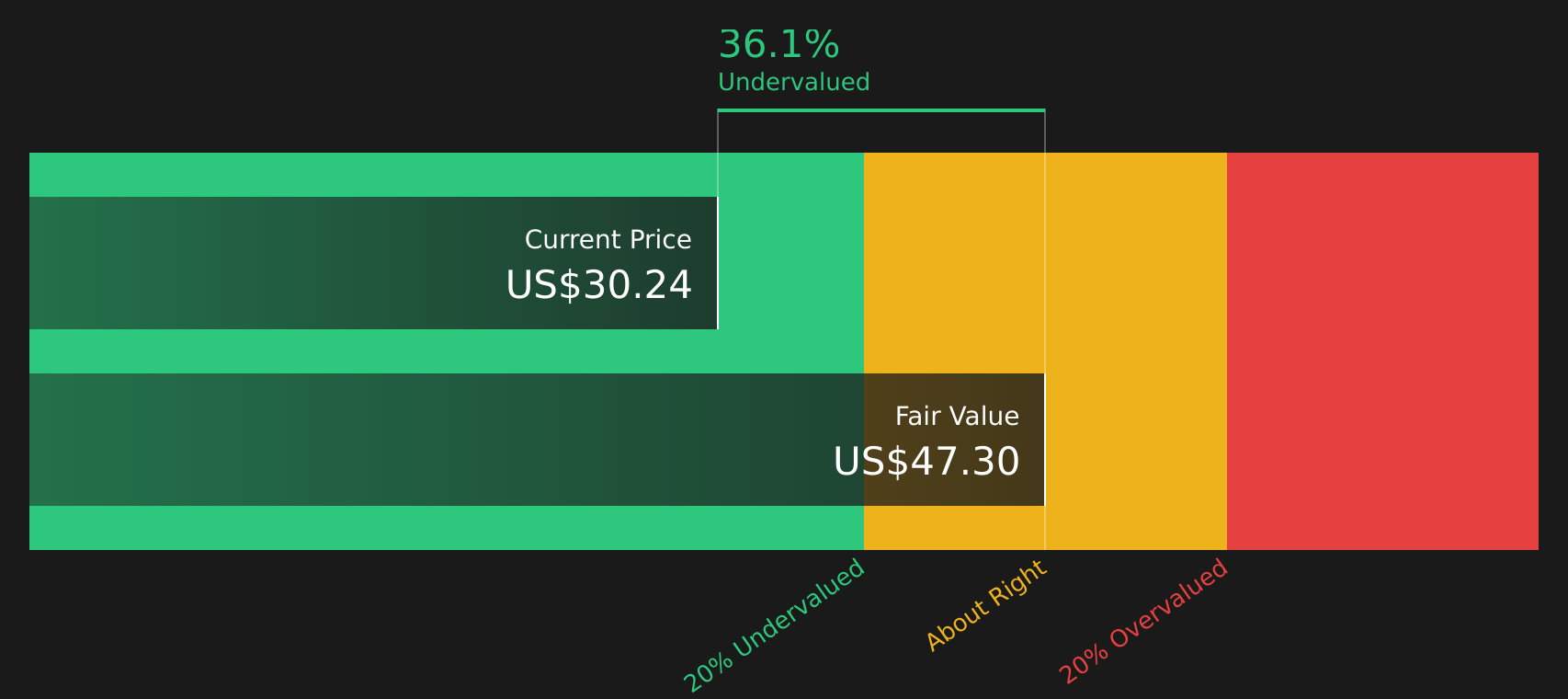

Most Popular Narrative: 61.3% Overvalued

Centuri's most followed narrative assigns a fair value of $24.33, which sits well below the latest close at $39.25, so expectations baked into the model matter a lot here.

Record backlog of approximately $5.9 billion and a robust $13 billion opportunity pipeline, including over 600 strategic bids, supports sustained revenue growth by converting awarded work into a higher, more stable top line.

Want to see what kind of revenue curve and margin profile that backlog implies? The narrative leans on tight assumptions about contract conversion, profitability and how long growth can be held.

Result: Fair Value of $24.33 (OVERVALUED)

However, if Centuri delivers on its double digit 2026 revenue target and margin initiatives take hold, the current fair value narrative could be tested quickly.

Another View: Cash Flows Point in the Other Direction

While the most popular narrative sees Centuri as 61.3% overvalued at $39.25 versus a $24.33 fair value, the Simply Wall St DCF model points the other way, with an estimated future cash flow value of $42.56. That implies the shares trade about 7.8% below this estimate. Which story do you trust more: earnings multiples or cash flows?

Next Steps

With mixed signals on value and sentiment running high, this is a good moment to move quickly, review the numbers yourself, and weigh up the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Centuri has you thinking about what else could fit your portfolio, this is the moment to widen the net and scan for other opportunities before they move.

- Target higher quality at sensible prices by reviewing companies flagged in our 51 high quality undervalued stocks that balance fundamentals with market expectations.

- Strengthen your income stream by checking out businesses highlighted in the 13 dividend fortresses that focus on returns through regular cash payouts.

- Reduce portfolio stress by focusing on companies in the 67 resilient stocks with low risk scores that are assessed to have more resilient financial and risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.