A Look At Chipotle Mexican Grill (CMG) Valuation After First Comp Sales Decline And Ackman Exit

Chipotle Mexican Grill, Inc. CMG | 35.42 | +1.43% |

Chipotle Mexican Grill (CMG) is under close watch after reporting its first year over year decline in comparable restaurant sales since going public, paired with guidance for flat comps in 2026 and a high profile investor exit.

The recent guidance for flat comparable sales and the first year over year decline in comps has coincided with fading momentum, with a 1 month share price return of 10.57% decline and a 1 year total shareholder return of 36.41% loss, even though the 3 year total shareholder return of 12.20% and 5 year total shareholder return of 23.21% remain positive.

If Ackman rotating into AI has you thinking beyond restaurants, it could be a good moment to scan our list of 34 AI infrastructure stocks for the next potential opportunity.

So with comps under pressure, mixed earnings revisions, a completed buyback program, and the stock trading around a 23% discount to the average analyst target, is this a reset worth considering, or is the market already pricing in future growth?

Most Popular Narrative: 17.9% Undervalued

With Chipotle Mexican Grill last closing at $36.30 against a most followed fair value estimate of about $44.24, the current setup reflects a clear gap between the narrative and the market price.

Chipotle is expanding its international presence with plans to open restaurants in Mexico by 2026 and exploring further expansion in Latin America and Europe. This international expansion is expected to drive future revenue growth.

Curious what kind of revenue ramp and margin path would need to line up for that $44 fair value to hold? The narrative leans heavily on sustained growth in absolute earnings and a rich future earnings multiple that currently sits above many restaurant peers. Want to see which specific assumptions carry the most weight in that story?

Result: Fair Value of $44.24 (UNDERVALUED)

However, slowing transaction trends and pressure on lower income and younger diners, as well as potential tariff or input cost shocks, could quickly weaken the earnings multiple this story relies on.

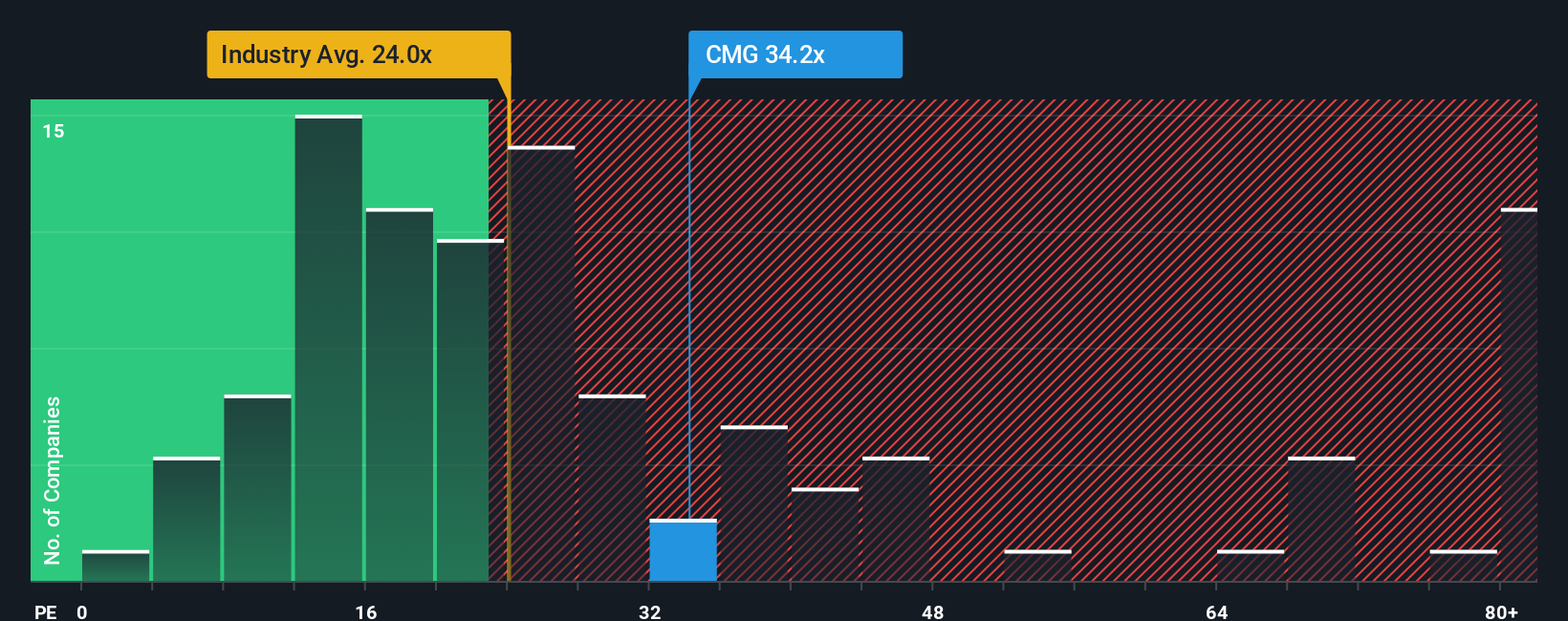

Another View: What The P/E Ratio Is Saying

While the fair value narrative points to Chipotle Mexican Grill as 17.9% undervalued at $44.24, the market’s current P/E of 30.8x tells a different story. That is lower than the peer average at 38.9x, yet higher than the US Hospitality group at 21.4x and above a fair ratio of 26.5x. This suggests some valuation stretch if sentiment turns.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Chipotle Mexican Grill for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Chipotle Mexican Grill Narrative

If you see the setup differently or just want to test your own assumptions against the numbers, you can build a full story yourself in minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Chipotle Mexican Grill.

Looking for more investment ideas?

If this Chipotle story has you rethinking your watchlist, do not stop here. The screener can surface opportunities you might regret missing later.

- Target quality at a discount by scanning our list of 53 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect them yet.

- Prioritise staying power by checking out solid balance sheet and fundamentals stocks screener (44 results) that focus on companies with stronger financial foundations.

- Get ahead of the crowd by reviewing our screener containing 23 high quality undiscovered gems that spotlight companies many investors may not be watching closely yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.