A Look At Chipotle Mexican Grill (CMG) Valuation As Earnings Beat Meets Flat 2026 Comparable Sales Outlook

Chipotle Mexican Grill, Inc. CMG | 34.92 | +0.95% |

Chipotle Mexican Grill (CMG) just delivered quarterly earnings that topped revenue and profit expectations, but the stock sold off after management guided to flat comparable sales for 2026 and ongoing pressure on guest traffic.

The weak 1 day share price return of 3.71% and softer 7 day move come after guidance for flat 2026 comparable sales and several updates on promotions, menu items, and record restaurant openings. At the same time, a 25.69% 90 day share price return contrasts with a 32.92% 1 year total shareholder return decline, suggesting shorter term momentum has picked up after a tougher year.

If earnings volatility around Chipotle has you looking for other themes, this could be a good moment to check out 22 top founder-led companies and see what else stands out.

So with Chipotle guiding to flat 2026 comps, a 1 year total shareholder return decline of 32.92% and shares trading about 15% below the average analyst target, is this reset creating an entry point, or is the market already baking in future growth?

Most Popular Narrative: 15% Undervalued

Chipotle’s most followed narrative pegs fair value at about $45 per share versus the last close at $38.45, framing today’s pullback as a valuation gap that hinges on how the long term story plays out.

Chipotle is expanding its international presence with plans to open restaurants in Mexico by 2026 and exploring further expansion in Latin America and Europe. This international expansion is expected to drive future revenue growth.

Want to see what kind of revenue ramp and margin profile would need to sit behind that expansion story? The narrative relies on a specific set of growth and profitability assumptions that have to align for $45 to make sense. The details are where this call becomes more interesting.

Result: Fair Value of $45.03 (UNDERVALUED)

However, this story can still break if traffic and same store sales stay weak into 2026, or if tariffs and input costs pressure margins more than expected.

Another Way To Look At Valuation

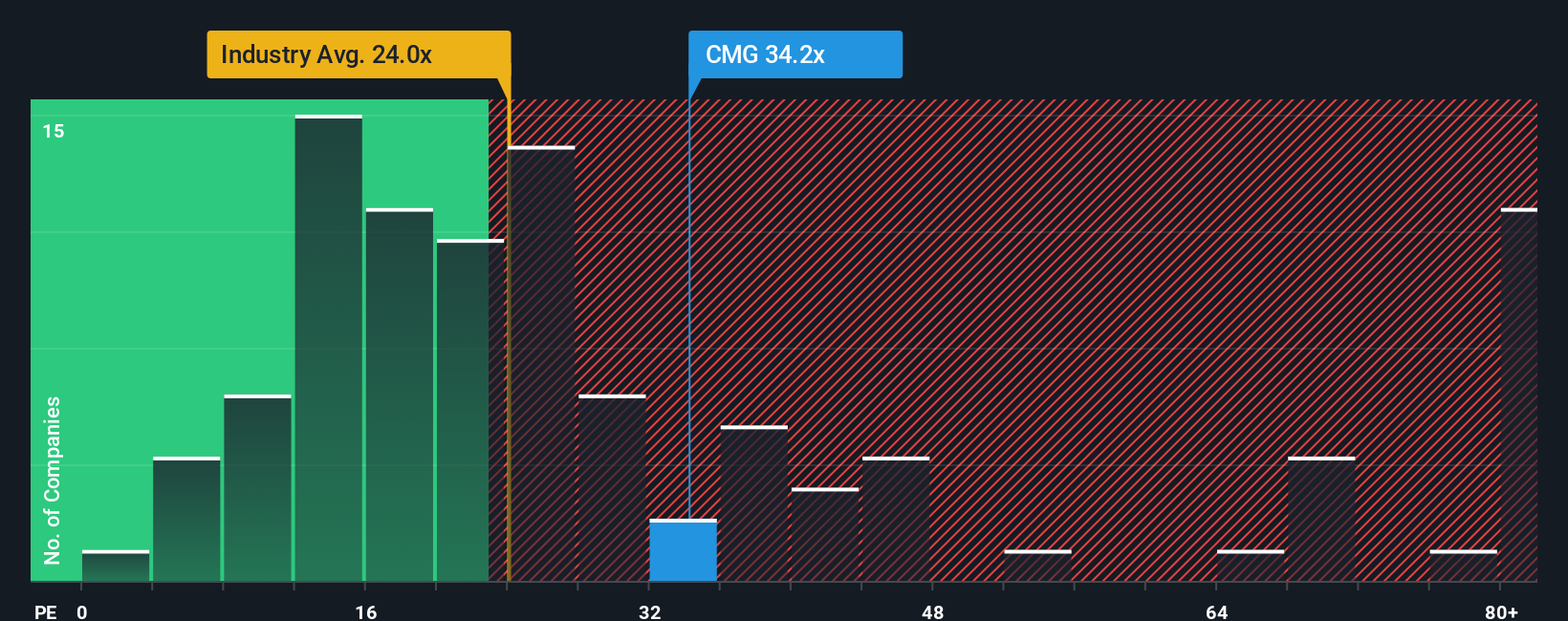

That $45 fair value hinges on long term growth assumptions, but the current P/E of 32.6x tells a tougher story. It sits well above the US Hospitality average of 21x and above a fair ratio of 26.9x, even though it is below a peer average of 56.3x.

In practice, that means the market is still asking you to pay a premium multiple, even after a 1 year total shareholder return decline of 32.92%. The question is whether you see that premium as justified by Chipotle’s quality and brand, or as extra valuation risk if growth stumbles again.

Build Your Own Chipotle Mexican Grill Narrative

If you see Chipotle’s setup differently, or prefer to work through the numbers yourself, you can create your own view in minutes: Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Chipotle Mexican Grill.

Looking for more investment ideas?

If Chipotle has you rethinking your next move, do not stop here. Use this moment to widen your watchlist with a few focused stock ideas.

- Target higher quality value by scanning our list of 55 high quality undervalued stocks that pair solid fundamentals with prices that may be out of sync with their underlying businesses.

- Prioritise staying power by checking out solid balance sheet and fundamentals stocks screener (46 results), where you can filter for companies with stronger financial footing and less stretched balance sheets.

- Hunt for under the radar potential through our screener containing 25 high quality undiscovered gems, highlighting stocks that have strong fundamentals but are not yet widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.